AmeriVet Weekly Muni Snapshot

|

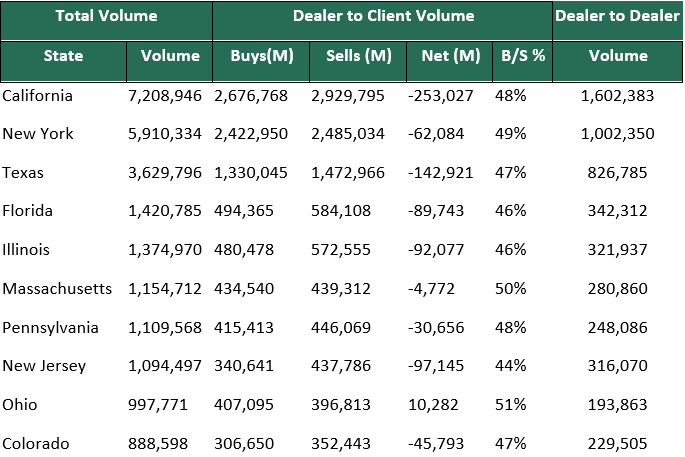

Municipal New Issuance: The third week of March negotiated calendar had a total volume of $5.3 billion, which is 17% less than the weekly average for 2022, and with half of the issuance coming from a single issuer, the New York State Dormitory Authority $3 billion issuance. University of Massachusetts Building Authority also issued this week to the sum of $607 million. AmeriVet was also in one issuance this week which was the $84 million South Carolina Finance and Development Authority. Many Issuers decided to take a pause in issuance this week and it was expected that investors will sit on the sidelines until after the Fed meeting. Municipal Secondary Trading: Secondary trading continues to be very active this week with roughly $38.65 billion up from the prior week of $36.9 billion, with 52% of the traded being clients buying. Buyers have been very active once the Fed hiked rates on Wednesday with many taking advantage on wider spreads. Secondary trading has been somewhat more active in recent weeks due to a lighter new issue calendar. Client’s put up for the bids worth roughly $5.2 billion with 3 of the days having over a billion in bids according to Bloomberg. |

|

|

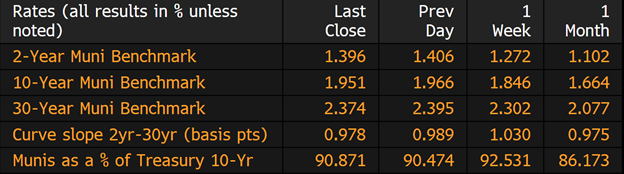

Municipal Spread: Municipal bonds continue to struggle this year along with other fixed income products as rates continue to rise this past week with 10-year notes rising about 10 basis points to 1.95%, with majority of the movement coming from the beginning of the week as investors were able to finally digest the much-anticipated rate hike that happened on Tuesday. After the rate hike, municipal bonds fared relatively well as they only adjusted by 5 basis points and could point to some positive sentiment going into this week. This positive sentiment in municipal bonds played well into their favor as 10-year municipal and the 10-year ratio is now at 90.87%, the week prior those same ratios were at 92.53%. We did see the municipal curve flatten last week with the gap between yields on short-term and long-term municipal flattening by 5.2 basis points to 98 basis points. |

|

|

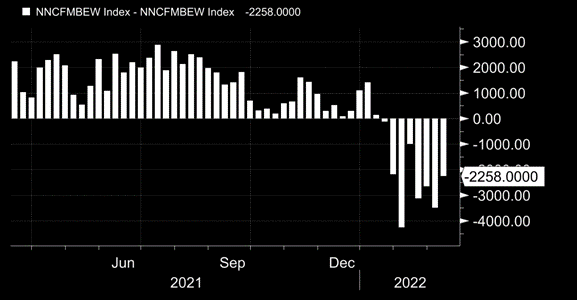

Municipal bond mutual funds continued to see investors pull money out of those to the sum of $2.1 billion. This follows the prior weeks loss of $662 million and marks the fifth straight week of outflows and a total of $17.5 billion of withdrawals year-to-date. This is a complete 180 of what we saw back in 2021 where we saw inflows almost every week with 2021 seeing 43 straight weeks of Inflows. |

|

|

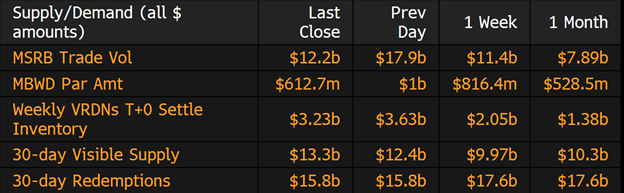

With the first of many Fed hikes finally behind us, we are starting to see municipals turn positive as investors have been finally able to digest the fed hike and have been slowly buying bonds particularly in the belly of the curve. Prior to the fed hike, municipal bonds have lost an average of 5.15% year-to-date, but after the hike they have recovered slightly only down 4.88% year-to-date. With low supply expected in the next 30 days ($13.3 billion), we should start to see some buying frenzy. |

|

|

|

Municipal Supply: This week’s negotiated calendar will have a projected volume of roughly $5.6 billion as we continue to see continue to many issuers hold on issuing or continue to place their bond issue on a day-to-day basis. Municipal bond sales are down roughly 8% from the same period last year. AmeriVet will be a Selling-Group-Member in the largest deal of the week which will be the $890 million New York City General Obligation. The second largest deal of the week will be the $594 million Illinois Finance Authority Revenue bonds for the Northshore Edward Elmhurst Group. |

|