AmeriVet Weekly Muni Snapshot

|

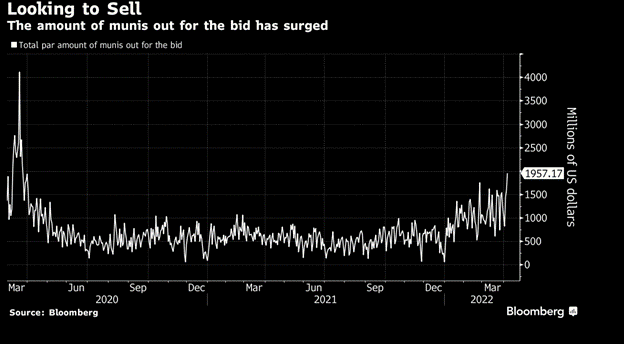

Municipal New Issuance: The first week of April saw a negotiated calendar size of just over $9.3 billion as many issuers chose to enter the market prior to the holiday shortened week. The largest deal of the week was the $1.3 billion New York Transportation Development Corporation for the JFK International Airport. Dallas Fort Worth International Airport also issued bonds to the sum of $1.1 billion. AmeriVet was part of two issues this week as a Selling-Group-Member, which was the $608 million Power Authority of the State of New York, as well as the State of Oregon Housing and Community Services Department. Municipal Secondary Trading: Secondary trading for first week of April totaled to roughly $41 billion as we continue to see volatility in the markets. Until we see rates stabilize, secondary trading should continue to be higher than the levels we are use to seeing. Back in 2021, in secondary trading, we were averaging roughly $30 billion. Clients once again put up a record number of bonds up for the bid. According to Bloomberg, clients put up $7.5 billion up for the bid with almost $2 billion on Wednesday. |

|

|

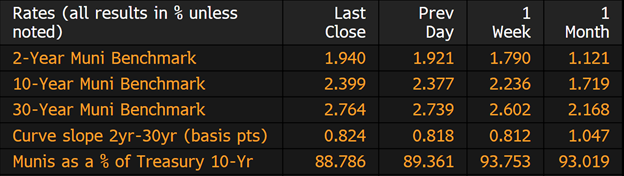

Municipal Spread: Municipals continue to have a rough go around this year as yields continue to rise as 10-year notes rose this past week by 16.3 basis points to 2.4%. With economists boosting their Inflation forecasts, as well as downgrading their economic growth though most of 2023 causing municipal bonds to post a 7% loss for the year. Despite showing a loss for the week, Municipals did outperform Treasuries as the 10-year ratio is now yielding 88.78% of Treasuries, compared to the prior week where the ratio was at 93.75%. We are continuing to see the yield curve flatten, as the curve flattened by 0.1 basis point to 82 basis points. The short end of the curve has risen by 150 basis points, while the long end has only risen by 120 basis points. |

|

|

Municipal Bond mutual funds continue to see investors pull money out of their funds as they pulled $3.2 billion from those funds during the week that ended on Wednesday. This was the fifth largest weekly outflow on record according to Lipper US Fund Flows data. This also marks the eight straight weeks of outflows as the Municipal Bond market continues to recover from a record decline in the first quarter. Once we start seeing rates stabilize then we should start to see outflows subside. |

|

Municipal bonds had a tough week, particularly on Wednesday, when yields on AAA bond rose as much a 11 basis points which caused the worst day of returns in over two years as investors are anticipating a hawkish rate-rise as the Federal Reserve continues to combat inflation. This sell off was in-part due to the $2 billion of bonds that investors put up for the bid which was the most since March 2020, when we were at the start of the pandemic. Municipals have posted a loss of 6.9% so far this year, for an asset class that is known for stability, this is unheard of. For example, municipal bonds have increased roughly 130 basis points since the start of the year. |

|

|

Municipal Supply: The negotiated supply for the week will be very light as we head into Easter weekend with a total expected supply of $3 billion with three deals taking up half of the issuance. The largest deal of the week will be the $500 million Regents of the University of Minnesota taxable deal. The next largest deal of the week which AmeriVet will be a Co-Manager on is the $500 million President and Fellows of Harvard College Taxable deal. |

|