AmeriVet Weekly Muni Snapshot

|

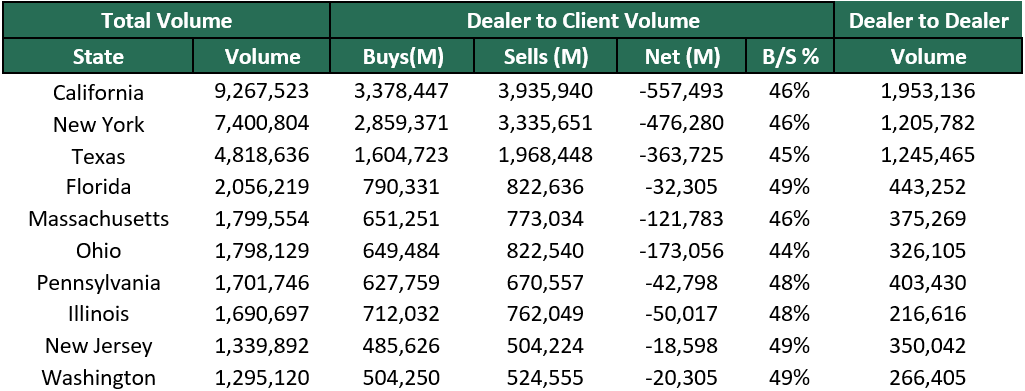

Municipal New Issuance: The first week of May had a very light negotiated calendar with just over $3 billion being issued, with just two issues being $300 million or more. The Triborough Bridge and Tunnel Authority issue of $927 million, which AmeriVet was a Selling-Group-Member. The next largest deal of the week was the $300 million State of North Carolina revenue bonds issuance. Many issuers had their deals on the calendar but chose to hold off on issuing ahead of the Fed rate decision. Although it was almost a guarantee that the Federal reserve would raise rates by 50 basis points, many chose to sit on the sidelines. Municipal Secondary Trading: May started off with a high number of secondary trading as volatility still remains in the fixed income markets. Secondary trading for the week totaled to roughly $ 50.26 billion, with bulk of the trading coming from the back half of the week as many traders were reacting to the fed’s decision to increase rates by 50-basis points. Continuing with the theme of the year, we continued to see clients put up record numbers of bids-wanted as clients put up just over $8 billion in bids-wanted for the week. |

|

|

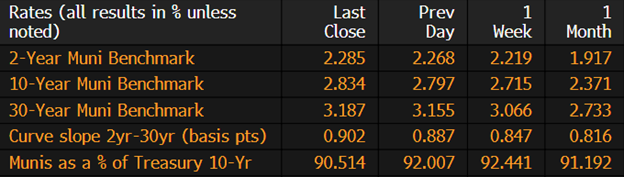

Municipal Spread: After having a quiet end to April, municipals bonds volatility returned last week with 10-year notes rising by 12 basis points to 2.83%. Majority of the movement was due to the Federal Reserve raising interest rates by 50 basis points. With municipal bonds tending to lag movements in Treasuries, it could take a few days until we fully catch up to the change in Treasuries. With that being said, municipal bonds did perform better than Treasuries as State and Local debt maturing in 10-years is now yielding 90.51% compared to the prior week when those ratios was at 92.44%. A month earlier those ratios was at 91.19%. With yields rising last week, we did see the yield curve steepen by 4.1 basis points to 90 basis points. |

|

|

Outflows continue to hit municipal bond mutual funds as investors once again pull money out of those funds to the sum of $2.67 billion according to Refinitiv Lipper Funds Flows Data. This is the 12th straight week of outflows and follows the previous week’s outflow of $2.88 billion. Until rates settle down, we should continue to see outflows from mutual funds as many continue to wait and see if the Fed can help resolve concerns of inflation. Currently, municipal funds have lost a total of $44 billion year-to-date marking the largest outflow streak since 2018. |

|

|

With the second rate of hike the year on Wednesday finally behind us, municipal bonds started its sell off just like the rest of the fixed income market with Treasuries reaching its highest levels since 2018 and municipal bonds hitting their highest March 2020. With yields at its highest in over two years, as well as ratios versus treasuries, this should signal a buying opportunity for investors, but many still continue to pull money out of funds until things settle down. With many predicting that rates will continue to rise, investors have made the decision to pull back and wait until things get better even as muni valuations are at attractive levels compared to the last two years. |

|

Municipal bonds have lost roughly 9.1% year-to-date slightly underperforming Treasuries, which have lost 8.5%, and corporate bonds have lost 12.6% over that same period. Even though municipals have cheapened. its not a from a credit stand point, but from a rates stand point as we have seen some of the larger issuers get upgrades such as the State of Illinois as well as Massachusetts Department of Transportation. |

|

|

Municipal Supply: This week’s negotiated calendar will have an expected volume of $9.6 billion for the week. This large calendar is due to the $3.2 billion Louisiana Local Government Environmental Facilitates and Community Development Authority taxable bonds issue. The Dormitory Authority of State of New York, a $750 million school district revenue bonds issuance, and the $750 million for the Northwell Health Obligated Group, which AmeriVet will be a Co-Manager on are the next two large issues of the week. San Francisco Bay Area Rapid Transit District will be issuing $700 million in green bonds for transit improvements. If you don’t count the Louisiana issuance, the calendar will still be very small as issuers continue to be in a holding pattern, trying to time when to issue as yields continue to rise due to the ongoing concerns with inflation. |

|