AmeriVet Weekly Muni Snapshot

|

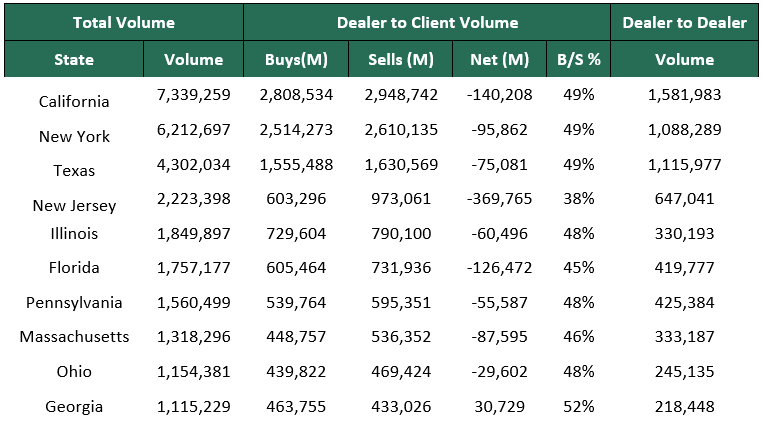

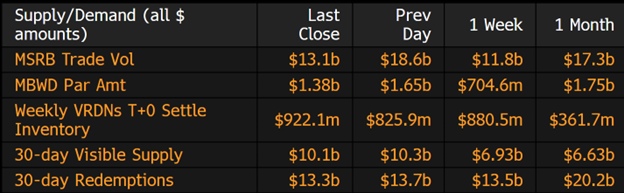

Municipal New Issuance: Last week’s negotiated calendar was very light due to the Columbus Day holiday on Monday as well as the CPI number coming out on Thursday to which many issuers decided to take break on issuing for the week. The negotiated calendar for the week totaled to just $1.4 billion with New Jersey Turnpike Authority taking up half of the issue by issuing $700 million in revenue bonds which saw overwhelming demand and were tightened as well as upsized due the demand. Municipal Secondary Trading: Although there was just four days of trading last week, we saw about $43 billion in secondary trading as volatility continues to hit the markets as accounts are still worried about high inflation, a possible recession, and the potential of more rate hikes. Clients’ bids wanted continue to be at elevated levels with about $7.33 billion in total par amounts according to Bloomberg. |

|

|

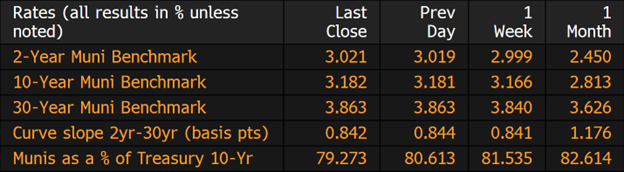

Municipal Spreads: Muni yields for the week rose slightly with the 10-year notes rising by just 1.6 basis points to 3.16% as munis sold off due the higher-than-expected inflation numbers on Thursday. Even though munis finished the week weaker, they were still able to outperform Treasuries as Treasury yields increased dramatically because of the CPI number. Ratios for bonds maturing in 10-years is now yielding 79.27% of Treasuries compared to 81.53% a week ago. The Muni curve steepened slightly by just 1 basis point to 84 basis points for the week. |

|

|

With inflation numbers remaining high, investors continue to take a step back to wait and see as municipal-bond mutual funds continue to see investors pull money out of their funds as Refinitiv Lipper US fund flows reported that investors withdrew $2.3 billion from those funds. This follows the prior weeks $2.05 billion of outflows and the 4th consecutive week of over $ 2 billion of weekly outflows. |

|

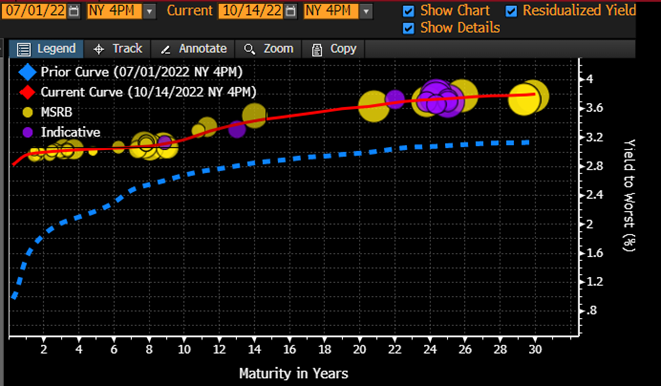

With the release of the CPI figures on Thursday, inflation continues to be at elevated levels. As a result of this, the MMD scale was cut by 3-5 basis points with the deeper cuts being on the short end while Treasuries saw a sharp rise in rates with 9-18 basis point increases 5 years and in. Although we did not see the sharp increases in yields as we saw in Treasuries, keep in mind that munis usually lag Treasuries as we are seeing the muni curve continue to flatten even more. Since the beginning of the third quarter, we have seen the short end yield rise by about 150 basis points, while the 10-year portion only increasing by roughly 70 basis points, and the long by just 65 basis points. |

|

|

Municipal Supply: The negotiated calendar for the week will pick up for the week with an expected volume of $7.3 billion. Although, it is a larger than average expected weekly volume for 2022, three of the issues cover over half of the issuance. The three largest deals of the week will be the $1.5 billion Colorado Health Facilities revenue bonds, the $1.1 billion State of Connecticut Special Tax Obligation bonds which AmeriVet will serve as a Co-Manager, and the $1.1 billon Commonwealth of Massachusetts deal which AmeriVet will also serve as a Co-Manager on. AmeriVet will also be in 4 other deals for the week as a Co-Manager which will be the $195 million Massachusetts Housing, $125 million Wisconsin Housing, $105 million Indiana Finance Authority, and the $88 million Department of Veterans Affairs of the State of California which AmeriVet will serve as a Co-Senior Manager on. |

|