AmeriVet Weekly Muni Snapshot

|

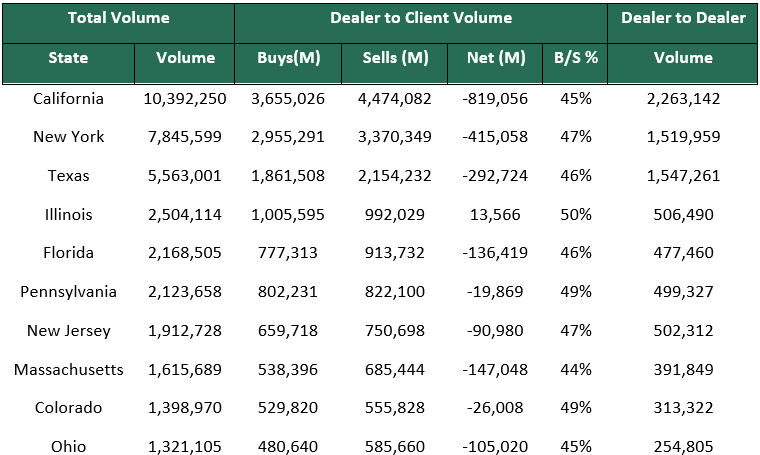

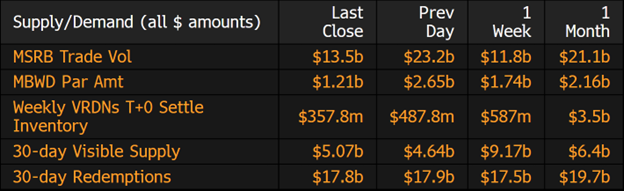

Municipal New Issuance: The negotiated calendar for the week totaled to about $5.8 billion with the largest deal being the $1 billion New York City Transitional Finance Authority issuance which AmeriVet participated as part of the Selling Group. The second largest deal of the week was the $700 million New York City Triborough Bridge and Tunnel issue. AmeriVet also participated in the $52 million University of Connecticut and $30 million New Hampshire Housing Finance Authority issuances as a Co-Manager. Municipal Secondary Trading: Secondary trading for the week totaled to roughly $55.58 billion as the selloff continues as investors continue to expect a few more rate hikes from the Fed. With the sell off in munis, we continue to see large amounts of customer bids-wanted again last week with a total of just over $10.5 billion with 4 days of having over $2 billion according to Bloomberg. The high number of bids wanted has caused increased amount of selling pressure in the markets causing more volatility as well. |

|

|

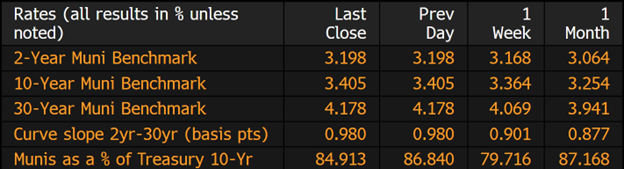

Municipal Spreads: Muni yields rose again for the week with 10-year notes rising by 4.1 basis points to 3.4%, the highest the 10-year has been since January 2011. With the rise in muni yields, muni ratios rose sharply with ratios on 10-year notes now yielding 84.91% of Treasuries compared to the prior week when the ratios were at 79.71%. With yields rising for the week, we did see the muni curve steepen by 7.9 basis points to 98 basis points. |

|

|

With yields still on the rise, we continue to see investors pull their investments out of muni mutual funds. According to Refinitiv Lipper US Fund Flows data, investors pulled $1.8 billion from municipal-bond mutual funds last week. This follows the prior week’s outflow of $2.6 billion as well as the 12th consecutive week of outflows. |

|

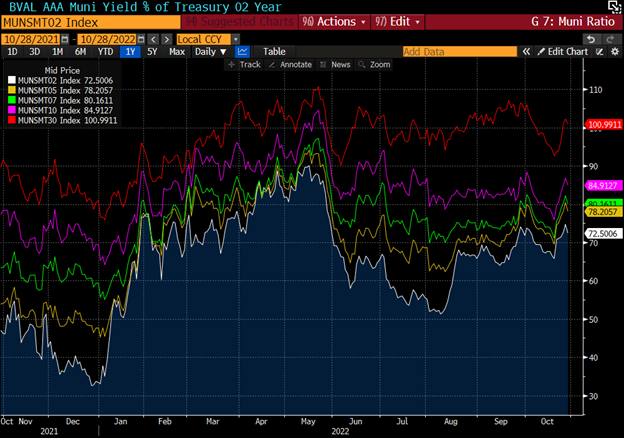

For the past few weeks, we have been talking about how much muni ratios have risen in the past few months and how investors are still focusing on the longer end of the curve, particularly 10-years and out as that continues to be the best part of the curve when compared to Treasuries. Currently, 10-year ratios are at 84.9% and when you go further down the curve, 5 year ratios are at 78.20%, and the 2-year ratio is at 72.5% which are both higher than the average for the last 10 years. The 2-year muni ratios average for the past 10 years has been 96.39% while the 5-year munis 10-year average has been 84.63%. When you look at 10-year munis, the 10-year average is at 92.3%, only 5 percentage points richer than the average which is still attractive compared to the shorter end. When you look at 30-year munis, those ratios are at 100.99% while the 10-year average is at 100.84%. |

|

|

Municipal Supply: The negotiated calendar for the week will be exceptionally light with just an expected volume of about $2.53 billion with the bulk of the calendar coming from just 3 issues. The largest deals of the week will be the $850 million City and County of Denver Colorado for its department of Aviation Airport Systems. The New York State Environmental Facilities Corporation is planning to issue $323 million in green bonds. Johns Hopkins University will be issuing $300 million in taxable bonds. |

|