AmeriVet Weekly Muni Snapshot

|

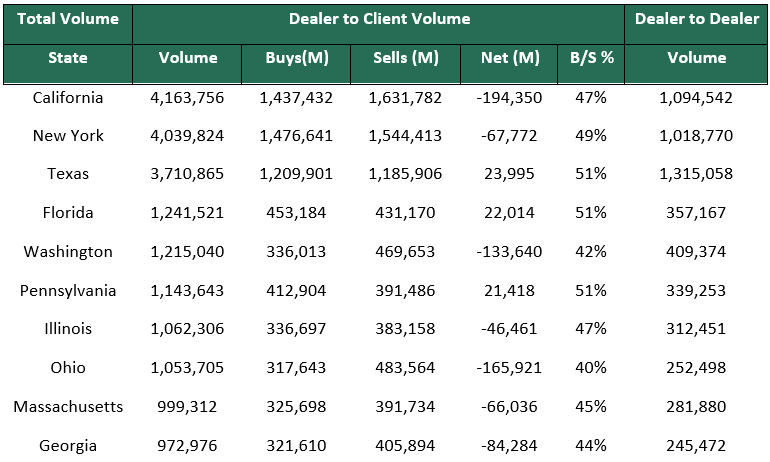

Municipal New Issuance: Last week’s negotiated calendar totaled to roughly $7.4 billion for the week as this was one of the more sizable issuance weeks for the year. The largest deal of the week was the $790 million California Community Choice Finance Authority for the Clean Energy Project issue. Dallas Independent School District issued $551 million in tax-exempt bonds last week. Chicago issued $735 million from the Sales Tax Securitization Corporation in taxable and tax-exempt bonds which AmeriVet participated as a Selling-Group-Member. This was the first time the city would be selling social bonds that are backed by sales taxes. Municipal Secondary Trading: With only four trading days last week, secondary trading totaled to roughly $31.69 billion with 52% of trades being clients buying, With supply continuing to be very limited, we should continue to see a high volume of secondary trading. According to Bloomberg, client’s bids-wanted totaled to $4.24 billion last week. |

|

|

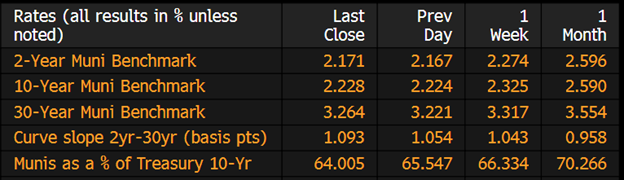

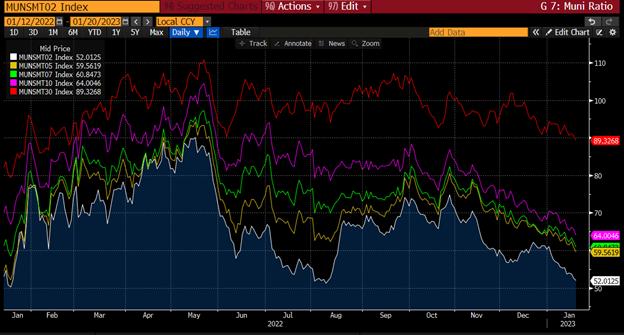

Municipal Spreads: We continue to see yields fall this year as yields on 10-year notes falling by 9.7 basis points to end the week at 2.12%. Yields on AAA munis have fallen an average of 38 basis points across the curve this year. With yields falling, we have also seen muni ratios fall as well as currently 10-year ratios to Treasuries is now yielding 64% compared to 66.33% a week ago, and 70.26% a month prior. With yields falling for three weeks in a row this year, we have seen the muni curve steepen by 5 basis points to 109 basis points. |

|

|

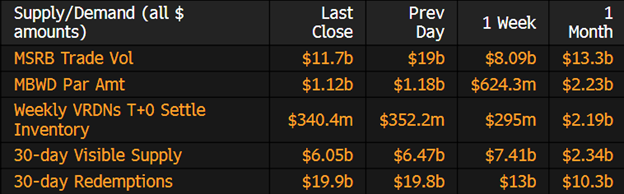

January continues to have positive inflows going into to the week of the month. According to Refinitiv Lipper US fund flows data, investors added about $2 billion to municipal-bond funds last week following last weeks inflow of $2.5 billion. This is positive news for munis as it is showing that investors are coming back to munis following a dismal year in 2022 in which we saw record outflows as yields rose due to inflation concerns as well as the possibility of a pending recession. |

|

With over half of the month over, munis have started the year off on a high note with returns of about 2.8% so far. This rally in munis has many factors to it as supply has been low to start the year coupled with high demand for bonds has led to yields falling to levels we have not seen since the second quarter of last year. Muni yields have fallen by about 40-55 basis points so far this year which has caused ratios to fall to levels near historic lows. If demand continues to outpace supply, we could see 10-year ratios head to its historic low of 54% back in 2021. With the 10-year ratio at 64%, it’s not too far out of the realm of possibility of us hitting 54% as the 30-day supply is at $6.47 billion and supply isn’t expected to pick up until March. |

|

|

Municipal Supply: Supply for the week will be down from last week with the negotiated calendars expected volume of about $4.5 billion. The $1 billion Triborough Bridge and Tunnel refunding issue will take up a quarter of this week’s calendar and the second largest deal of the week will be the $383 million State of Wisconsin taxable issue. |

|