AmeriVet Weekly Muni Snapshot

|

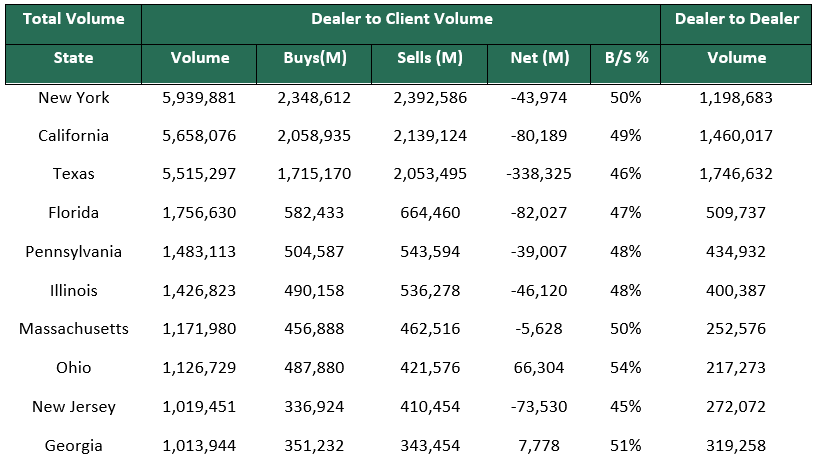

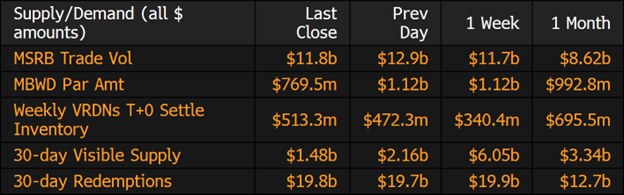

Municipal New Issuance: Last week’s negotiated calendar totaled to roughly $4.58 billion as many issuers decided to issue last week in anticipation of the FOMC rate decision coming later this week. The largest deal of the week was the $828 million Triborough Bridge and Tunnel issue which AmeriVet was part of the Selling-Group. The second largest deal of the week was the $383 million State of Wisconsin deal. The Triborough issue garnered a lot of interest as it was well over-subscribed during the retail order period with some of the longer maturities being 3-4 times over-subscribed. Municipal Secondary Trading: Secondary trading picked up this week with roughly $41.10 billion in secondary trading with 52% of trades being clients buying. With the continued low supply, clients continue to purchase bonds in the secondary market causing yields to fall which has resulted in munis becoming even more expensive when compared to Treasuries. According to Bloomberg, last week clients put up roughly $5.4 billion up for the bid with four of those days having bids-wanted of over $1 billion. |

|

|

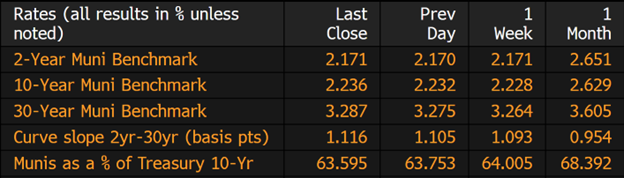

Municipal Spreads: Muni yields remained relatively unchanged for the week with the exception of yields on 10-year notes rising by just .8 basis points to 2.22% to end the week. Munis are off to a great start this year with yields falling an average of 40 basis points so far this year. Although muni yields did rise slightly last week, we are continuing to see muni ratios fall with 10-year notes now yielding 63.59% of Treasuries, compared to 64% a week ago and 68.39% a month prior. These are the lowest levels to US Treasuries since July 2021 as many investors are returning to the market and as supply continues to come at a snail’s pace. We did see the muni curve steepen last week by 2.3 basis points to 111 basis points. |

|

|

For the third straight week in a row, muni-bond funds saw investors add to their funds with last week seeing investors add roughly $1.3 billion according to Refinitiv Lipper US Funds Flows data. Investors have added about $4.8 billion in the first 3 weeks of the year. This is positive news as it’s a sign that investors are coming back into the market. |

|

Muni bonds continue start the year off on a good note as they are up by about 2.86% and with with the rally in Treasuries, coupled with inflows into muni funds, as well as the lack of supply has fueled this rally to its best start since 2009. Even with the Fed expecting to raise rates again later this week and most likely at their next meeting as well, many investors are optimistic that the worst is behind us and they see the light at the end of the tunnel as the Fed is nearing the end of their tightening policy. This has caused some adverse effects on the markets as munis have been outpacing Treasuries by about 25 basis points which has caused munis to become increasingly rich especially in the short end of the curve. The 2-year stands at 51.8% with the 5-year average being 87% while the 10-year is at 62% with the 5-year average at 87.60%. This has caused many to go further out on the curve and is something we at AmeriVet observed in the Triborough deal last week with the longer maturities being well oversubscribed. |

|

|

Municipal Supply: This week’s calendar will be very limited as many issuers are taking a pause until after the Fed announcement of how much they will be raising the Fed Funds Rate. The negotiated calendar will only have roughly $664 million in expected volume. The largest deal being the $277 million Fort Worth Independent School District. The next largest deal will the be $86.9 million Alaska Municipal Bond Bank issue which will include taxable and AMT bonds. |

|