AmeriVet Weekly Muni Snapshot

|

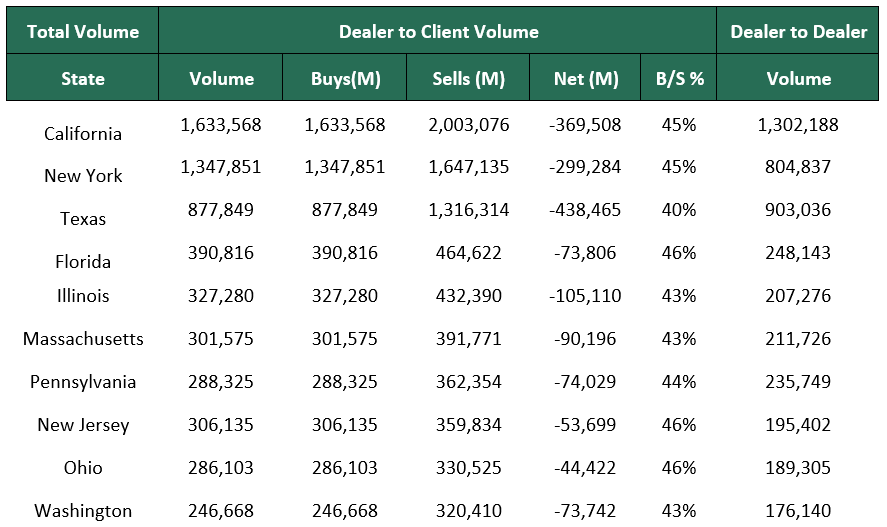

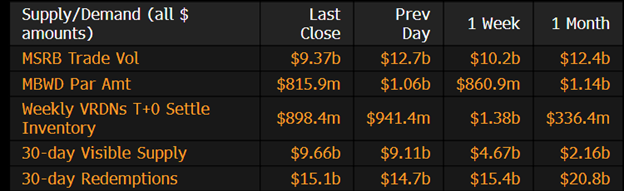

Municipal New Issuance: With the Presidents Day holiday on Monday, the negotiated calendar totaled to just $2.2 billion for the week with the largest deal being the New York City GO issuance totaling to $688.32 million which AmeriVet was in the Selling-Group. AmeriVet was also part of two other issues for the week which were the Massachusetts Housing issuance which issued $95 million in tax-exempt bonds and $61 million in taxable bonds as a Co-manager, and the $17 million Community Development Administration Maryland Department of Housing as a Selling-Group-Member. Municipal Secondary Trading: With only four trading days last week due to the President’s Day holiday, secondary trading for the week was only $29.1 billion with 56% of the trades being client buys. With the limited supply, investors continue to go to the secondary markets to purchase bonds. According to Bloomberg, clients bids-wanted was small as well with just $4.69 billion put up for the bid. |

|

|

Municipal Spreads: Muni yields continue to rise this past week as yields on 10-year notes rose by 7.7 basis points to 2.61% marking three straight weeks of rising rates. Although we did see yields rise considerably this past week, the tone of the market has improved from the prior week where we saw an almost 50 basis point rise in the front end of the curve. Muni bonds outperformed Treasuries slightly with the 10-year Muni-Treasury ratio now at 66.68% compared to 66.93%. Although muni yields continue to rise, they continue to be rich compared to Treasuries and demand continues to outpace supply. With the rise in yields, we did see the muni curve flatten again this past week with the curve flattening by 10 basis points to 71 basis points. |

|

|

For the second straight week municipal-bond funds saw investors pull money from their funds. According to Refinitiv Lipper US Fund Flows data, investors pulled about $1.77 billion from municipal-bond funds, the largest we have seen so far this year. |

|

As we enter the final week of February, munis continue to struggle with yields rising an average of 45 basis points this month. To put things in perspective, of the 17 trading days we’ve had this month, 8 of them saw a rise in yields, and on the 9 trading days we had only 1 day in which we saw yields fall. This has pushed rates back to the levels that we started the year with. Currently munis are down 2.29% for the month and have a year-to-date return of just .51%. With March on the horizon, we should note that the month of March has a historical performance that has not been positive. Based on Bloomberg municipal bond index (LMBITR), in the past 28 years munis have been down 13 years and positive in 15 years, and of the 15 years of positive returns, only four have had returns of 100 basis points. |

|

|

Municipal Supply: The negotiated calendar continues to be very light with an expected volume of just $4.8 billion for the week with four issues taking up half of the issuance size. The largest deals of the week will be the Port of Portland-Oregon Airports issuance which plans to sell $583.2 million, followed by the $529 million Chicago Board of Education issuance, and the $392 Washington Metropolitan Area Transit Authority issuance. |

|