AmeriVet Weekly Muni Snapshot

|

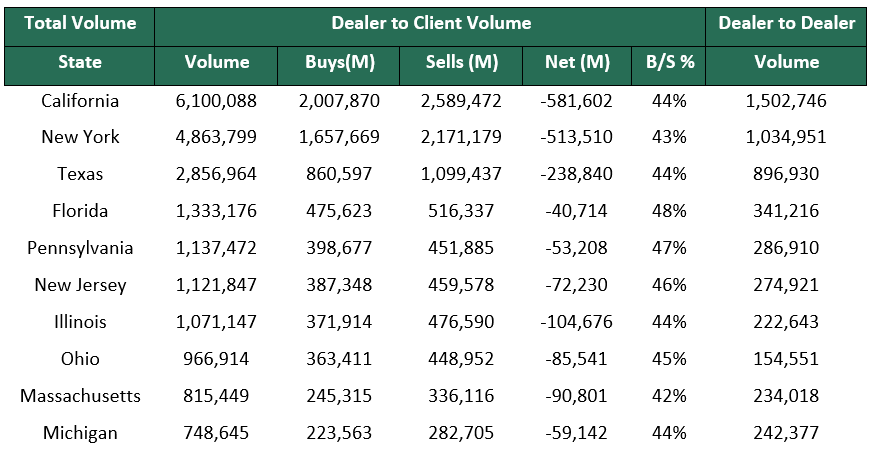

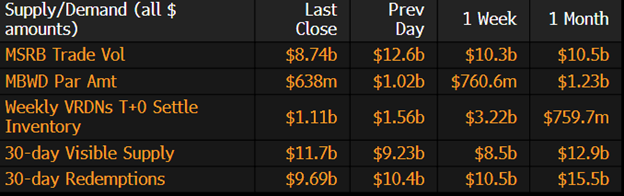

Municipal New Issuance: The negotiated calendar for this past week totaled to just over $3.8 billion with largest deal of the week, the $950 million New York City GO issuance, which AmeriVet participated in the Selling-Group, garnering the most interest. The second largest deal of the week was the $314 million Michigan State Housing Development Authority issuance. AmeriVet was also in one other issue this week which was the $43 million New Hampshire State Housing Finance Authority. Municipal Secondary Trading: Trading for the week totaled to roughly $37.56 billion with about 56% of trades being clients buys. Secondary trading continues to have a strong bid side as the primary market continues to be catch up to demand. According to Bloomberg, customer bids-wanted totaled to about $4.5 billion for the week, compared to $5.01 billion from the week prior. |

|

|

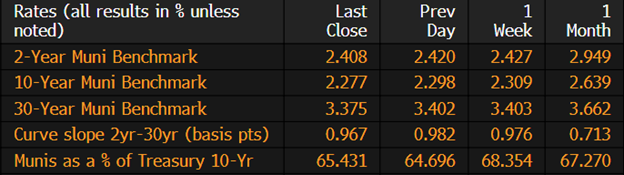

Municipal Spreads: Muni yields fell once again this past week, marking four straight weeks of falling yields as 10-year notes are now yielding 2.27% compared to 2.31%. Yields have fallen roughly an average of 29.9 basis points this month. A reversal of February, a month in which we saw yields rise by an average of 46 basis points. With the continuation of the muni rally, munis were able to outperform Treasuries this past week as 10-year munis are now yielding 65.43% of Treasuries, compared to the prior week when the ratios were at 68.35%. The muni curve did steepen slightly this past week by .9 basis points to end the week at 96 basis points. |

|

|

Investors continue to pull money out of municipal bond funds even as yields are falling. With market volatility continuing to spook investors as the direction in interest rates are still up in the air. This past week, investors pulled about $194 million from those funds, this follows the prior week’s outflow of $427 million. |

|

The month of March started off on a high note and is finishing up the same way it started – in positive territory. Muni have returned over 2.2% for the month, a great reversal from February where munis returned a loss of 2.26%. For the first quarter of 2023, munis have returned about 2.78%, a far cry from 2022 when we had losses of 6.23%. For the first quarter of 2023, yields have had a roller coaster ride as signs pointed to the Fed ending their tightening cycle to only be do a complete 180 when an unexpected jobs data report in February spurned more hikes from the Fed. Then the collapse of Silicon Valley bank and Signature Bank pushed yields lower as once again the Fed appears to be winding down their tightening policy. With limited supply in munis, we could continue to see a strong bid-side market which will drive yields even lower. |

|

|

Municipal Supply: The negotiated calendar for the week will total to roughly $5.2 billion. Although it is sizable compared the prior couple of weeks supply, half of the issuance is from just one issue, the $2.5 billion State of California tax-exempt GO issuance, which AmeriVet is participating in the Selling-Group. The second largest deal of the week will be the San Francisco City & County Public Utilities Commission Wastewater Revenue which plans to sell $998.6 million in bonds. Supply for the first quarter of 2023 is down 24% and until we start to see rates stabilize, supply will continue to be at record low levels. |

|