AmeriVet Weekly Muni Snapshot

|

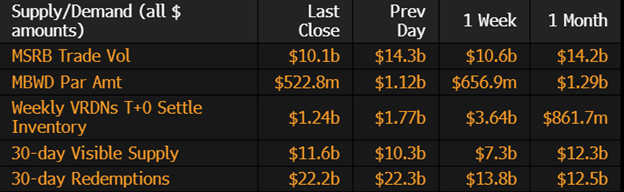

Municipal New Issuance: The negotiated calendar for this past week totaled to just over $4.1 billion with the largest deals being City of Chicago Water revenue bond issuance which sold over $1 billion. The second largest deal of the week was the $506 million Energy Northwest which issued refunding bonds for the Columbia Generating Station. With the FOMC rate decision earlier in the week, many issuers took a pause on issuing as many expected a 25-basis point hike. With the Fed expected to take a pause on any more hikes, we should expect to see an increase in issuance on the muni side. Municipal Secondary Trading: Trading for the final week of April totaled to roughly $36.23 billion with 58% of trades being dealer sells. We are starting to see investors slowly move further out in the curve as the front end continues to be rich compared to Treasuries. According to Bloomberg, clients put up roughly $4.59 billion for the bid which is down from the prior weeks total of $5.56 billion. |

|

|

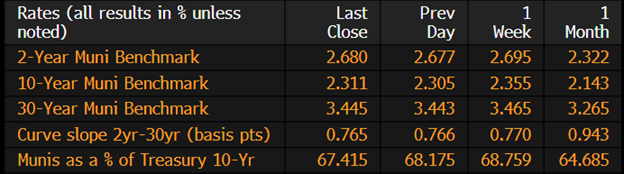

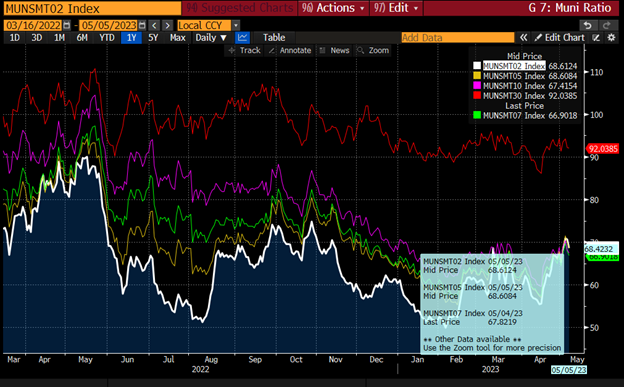

Municipal Spreads: After two straight weeks of yields rising, munis saw their yields fall with 10-year notes falling by 4.4 basis points for the week to finish the week at 2.31%. Although yields fell for the week, munis did perform slightly better when compared to Treasuries as the 10-year notes are now yielding 67.41% compared to the prior week when ratios were at 68.76%. Even as yields rose this past week, the muni curve remained relatively unchanged for the week with the curve flattening by just .5 basis points to 76 basis points. |

|

|

For the 12th consecutive week, muni bond funds saw outflows with investors pulling about $846 million from muni funds this past week according to Refinitiv Lipper US Fund Flows. This loss follows the prior weeks outflow of $92 million. Despite 12 consecutive weeks of outflows, muni fund inflows stand at just $4.1 billion for the year. Even as munis continue to improve from 2022, we are continuing to see investors pull money out of funds. With the potential end of the hiking cycle in our sight, we could start to see money flow back into muni funds. |

|

Over the past few weeks, we have seen muni-to-Treasuries ratios tending to be higher more particularly in the front end. Although this is positive for munis as the front end has become extremely rich over the past year, we are still in rich territory. Ratios on the front end back in mid-April reached an average of 58% and have moved higher to an average of about 70%, which is still rich as the average ratio for the front end is about 90%. Currently, the best part of the curve has been the 12-20 year range as we have started to see larger funds move towards this portion which has driven yields down on the belly of the curve. |

|

|

Municipal Supply: The negotiated supply for the week will be have an expected volume of $6.4 billion with the largest deal being the $1 billion Dormitory Authority of the State of New York issuance which AmeriVet will be participating in the Selling Group. The next largest deals of the week will the Lower Colorado River Authority which plans on selling $481 million in refunding bonds followed by the City of Dallas, which will be offering $445 million. |

|