AmeriVet Weekly Muni Snapshot

|

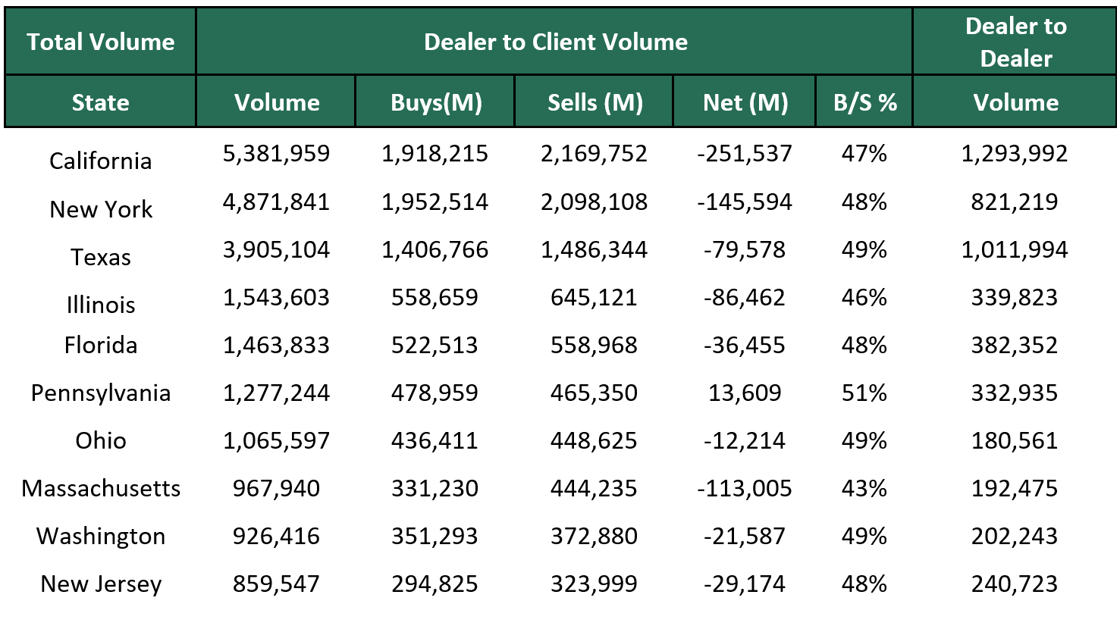

Municipal New Issuance: The negotiated calendar for this past week totaled to just over $6.3 billion with the largest deal being the $1 billion Dormitory Authority of New York which AmeriVet was a Selling Group Member. The next largest deal of the week was the $472 million Lower Colorado River issuance. With a larger than average calendar, there was not the usual high demand for bonds this week. Municipal Secondary Trading: Trading for the week totaled to roughly $35.4 billion for the week with 52% of the trades being dealer sells. With a larger than average calendar this past week, secondary markets took a back a seat to the primary markets. According to Bloomberg, clients put up roughly $6.7 billion up for the bid, up from the prior week in which clients put up $4.6 billion. |

|

|

Municipal Spreads: Last week muni yields remained relatively unchanged as 10-year notes rose by just 0.8 basis points to close out the week at 3.32%. With yields remaining unchanged for the week, we did see the muni ratio fall slightly with 10-year notes now yielding 66.94% of Treasuries compared to the prior week’s ratio of 67.18%. The muni curve also remains unchanged at 75 basis points. With about $134 billion in redemptions in the next couple of months, we should expect this to boost the muni market. |

|

|

According to Refinitiv Lipper US Fund Flows data, investors pulled about $102 million from muni funds this past week marking the 13th straight week of outflows. This follows the previous week’s outflow of $846 million. With rates volatility seemingly subsiding in the past few weeks, we could start to see outflows decrease and demand flow back into munis. |

|

With redemptions topping over $134 billion in the next few months and with a net negative supply of about $13.2 billion over the next 30-days, we should expect this to drive yields further down. Coupled with higher yields, demand should be high for new bond sales. This weakness in the markets should be offset by reinvestments into munis, but we should still be cautious until we start to see a reversal in flows in muni funds. |

|

|

Municipal Supply: The negotiated supply for the week will be have an expected volume of just under $4.8 billion, with largest deal of the week being the $277 million California Housing Social Certificate issue. The Dormitory Authority of New York for Columbia University will be selling $275 million in revenue bonds. |

|