Fed Preview: After 10 Years, It’s Time

When Jay Powell steps to the podium this week, many of the themes he will speak about regarding the Fed’s decision to lower interest rates for the first time in a decade will sound familiar:

“uncertainty, downside risks to the outlook, inflation shortfalls, insurance and the Fed will continue to take appropriate actions to sustain the recovery”

Over the course of the last 9 months, we have generously shared thoughts and opinions on the Fed, interest rates and a very uneven way forward. We began reading signals of concern from Powell (and were vocal about it) in November of 2018. And when the global markets began to react aggressively toward the end of 2018, coupled with the final and inappropriate hike, we went on record in a methodical way to help navigate one of the biggest U-turns in Fed history.

Some of our thoughts along the way:

December 20, 2018

- Ultimately we believe that base (for the market) will need to come from the Fed as it becomes more apparent their work has gone too far. This is not the same economy we had ten years ago. We are a global market place laden with extreme debt levels, much of it USD denominated and certainly higher in size than 10 years ago

February 2, 2019

- The Fed’s mandate is symmetric. And when pressed about whether the next move in rates was up or down his answer equally clear: that will depend entirely on the data. Without question, although the baseline case for the Fed is constructive for the economy, if the dis-inflationary forces being felt by the market at the moment are real, and more importantly sustained, a shift toward looser policy is plausible

June 5, 2019

- His most recent speech outlines thought on neutral rates moving lower, asustained flattening of the Phillip’s curve and an open mindset to accepting the data while recognizing models can be wrong and require at times more art than science with forward intuition. It supports the case, we believe, for a more proactive v reactive Fed in the context of the current environment.

June 14, 2019

- It is our opinion lower rates are coming from the Fed. We believe that 50-100 basis points (2019-2020) is possible. We don’t expect that all to come this year, although the direction is right and matters.

Why is the Fed easing?

Both the Fed and ECB miscalculated policy in 2018. Heading into the latter part of 2018, normalization was alive and well. Until it wasn’t. The ECB ready to raise rates and the Fed heading to neutral of 3%. The speed and force in which financial conditions came down was lasting.

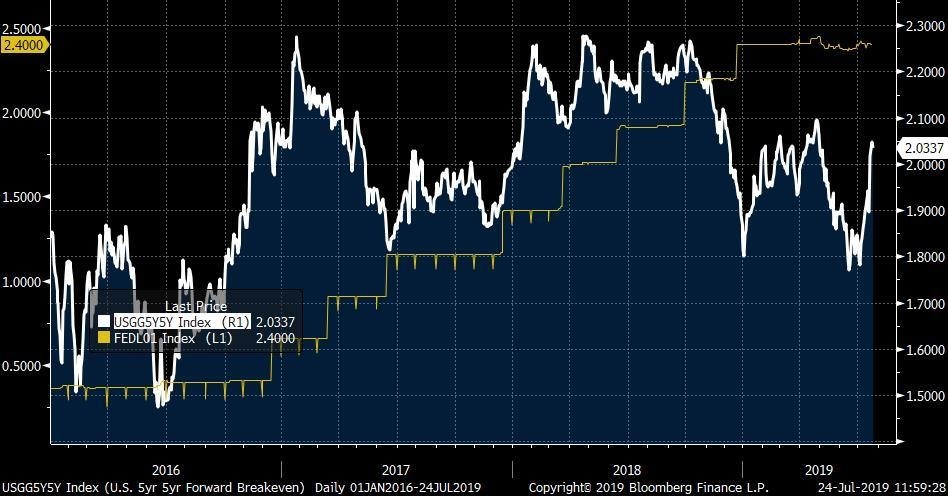

1) The damage to global markets and financial conditions spilled over into 2019. To us, the chart below tells the picture. One in which the EFF (Effective Funds Rate) watched the sharp decline in 5-year forward, 5-year break-even inflation expectations cross over, head lower and never recover since the last quarter of 2018. The overlay of Europe looks very much the same.

EFF (Effective Fed Funds versus 5-year forward, 5-year inflation break-even)

2) The global outlook has changed. We have spoken about GDP-at Risk (GaR) and a more forward looking Fed. This is not a matter of looking at the data NOW. So much of late has been about the rebound in data. Point taken. However, that is not what the Fed is looking at when formulating current policy. Within the context of their models are risk factors. And those factors are adjusted based on risk to the accuracy of the outlook. The global economy is very bifurcated right now. And to simply ignore the manufacturing recession would be a mistake. It is very difficult to compartmentalize manufacturing from other areas within the global economy.

3) The FF rate is too high and funding pressures exist. Not too long ago, the Fed tweaked the IOER. The administrative rates the Fed has been using to manage the target range for the FF rate, for the most part has worked. Yet we continue at times to challenge the upper bound. $ are scarce and our currency is strong. Despite “posture” from the Fed, the USD has been on a tear, more so because of extreme weakness abroad. And that is simply a dynamic which is hard to control from this side of the pond. There is, and will continue to be a dependency on a global rate and central bank structure, which right now is very dovish. Couple this with the US running pro-cyclical deficits, and the Fed simply needs to get absolute and relative rates lower at the moment, and for multiple reasons.

EFF (Effective Fed Funds v US Overall Debt Levels)

The Fed Meeting

We have been advocating lower rates for many months. The debate between 25 v 50 basis points is valid, but we still believe the discussion within the Fed is more about:

“to cut or not to cut. Pricing for 100% and a split mainly skewed toward 25 basis points seems rational heading into the meeting“

1) The committee is divided. Certainly, the inner circle (Powell, Clarida, Williams) has been very consistent of late: a cut is coming. Yet, there are voting members within the committee still undecided. They see the here and now in the data and would prefer to wait. Inner circle wins but not without a vigorous debate. Another reason we believe it leans 25- basis points.

2) We are on the lookout for a twist. Something along the lines of the Fed cutting the official rate by 25-basis points but having it “feel like more” through something unconventional.

The Fed and Powell have been consistent in utilizing verbiage along the lines of “using all of their tools“. Repeatedly. And certainly the ECB laid out a comprehensive plan and not limited to just lowering the official rate. Balance sheet, IOER, Repo facilities and more.

3) Powell will be very transparent in his press conference. Most certainly he will be asked about independence. And with the data recovering lately, the need to ease at all.

We do expect him stay the course:

Insurance cut, risks management, inflation expectations, global uncertainty- door open for more IF warranted.

What next?

1) It would be surprising if the Fed signaled one and done. Theoretically, they could do 50-basis points and signal “that’s it”. Although that scenario almost sounds stupid with the line for easing being “uncertainty”. How could the Fed cut and be certain their done?

2) A 25-basis point move followed with an open mindset is plausible and our baseline call. Yet, if the Fed leans on the inflation side of their mandate (which we expect to happen), then they will be tied to that notion going forward. In other words, the Fed will likely maintain a bias to ease until they see a sustained pickup in expectations: 25, 50, 75

3) The hardest work is ahead: the Fed and ECB. Without additional help (prudent) on the fiscal side, the likelihood of continued loose policies failing, is high. Draghi leaves in a few short months and Powell is struggling to find his footing. We think it’s likely once we move past the Fed, and shift to a very data dependent environment, a pickup in volatility follows.