Weekly Muni Snapshot | July 12, 2021

|

Municipal New Issuance: The July 4th holiday shortened week saw a very small, negotiated calendar totaling only $3.7 billion in issuance. The largest deal of the week which made up roughly half of the issuance was the $1.8 billion California University Revenue bonds which included taxable bonds as well as tax-exempt bonds. This deal was some great significance to AmeriVet because this was the first time the firm was able to participate in the issuance as a Co-Manager.

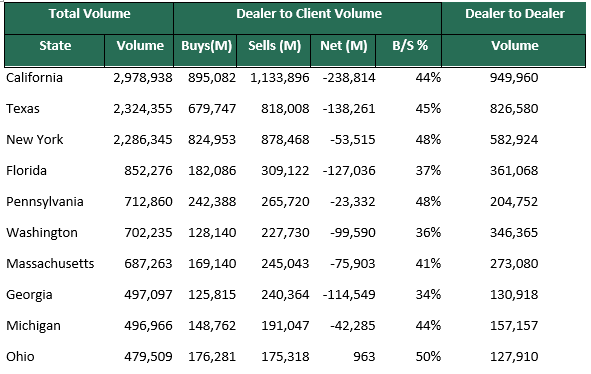

Municipal Secondary Trading: With the markets closed on Monday secondary trading for the week was very light with $18.68 billion in secondary trading. Dealers selling to customers totaled roughly 56% of all trades, continuing the trend of clients wanting tax-exempt bonds. According to Bloomberg client’s bids-wanted were also down for the week with clients putting out only $1.3 billion of bonds out for bid. With a full week a head we do expect to see trading volume as well as bids-wanted to come back to their 2021 levels with trading volume around $25 billion and bids-wanted to total approximately $2.9 billion. |

|

|

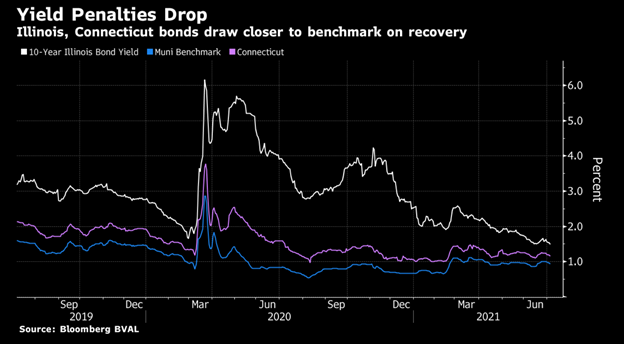

Municipal Spread: With the shortened holiday week municipal bonds had some significant movement as yields on the Bloomberg 10-year benchmark fell by 11.6 basis points to 0.865% which has been one of the largest moves we have seen this year. With this rally in municipals, municipals did outperform Treasuries as they are now yielding 63.74% of Treasuries compared to 68.79% a week ago. We are slowly moving closer to our lowest historical ratios levels which was 53.87% on February 16th of this year. The municipal bond curve did flatten for the week as the gap between short-term bonds and long-term bonds moved by 11.3 basis points to 127 basis points. |

|

|

According to Refinitiv Lipper US Fund Flows Data municipal bond mutual funds added $2.29 billion, marking the 18th straight week of inflows. This follows the prior weeks inflow of $832 billion. Even as municipal bonds become even more expensive this continues to show investors find value in owning tax-exempt bonds. States and local governments have experienced tremendous credit and market volatility from March 2020 to today as the rating agencies lowered their outlook rating outlook as they projected that state and local governments would have some significant revenue short falls back in 2020 due to the economic stress from the pandemic. Fast forward to today the rating agencies such as S&P Global and Fitch Ratings have changed their views as they have both upgraded their outlooks on about $400 billion of municipal bonds this year. This positive change to their credit views is due to the influx of federal aid as well as the surge in tax revenues that was not expected which has lessened much of credit stress that was triggered from the pandemic. The improvement in the national economy has kept defaults to a minimum and has allowed municipal bonds to show a net positive return of 1.3% this year as Treasuries have shown a negative total return of 2% year-to-date according to Bloomberg Barclays Indexes. High yield municipal has even showed better gains with 6.5% year to date as investors sought more yield and were willing to take on the additional credit risks higher yielding bonds have. |

|

|

Municipal Supply: Supply for the week will be an increase from the prior week’s of $3.4 billion to roughly of $7.9 billion on the negotiated issuance. The largest deal of the week will be the $832 million Chicago Metropolitan Pier and Exposition Authority refunding bonds. AmeriVet will be part of the second largest deal of the week which will be the $589 million New York City Transitional Finance Authority Refunding bonds. In addition, the Water Works Board of the City of Birmingham is scheduled to sell $469 million in taxable revenue refunding bonds this week and The Dormitory of New York will be selling $250 million in taxable and tax-exempt bonds. |

|

|