Weekly Muni Snapshot | May 10, 2021

|

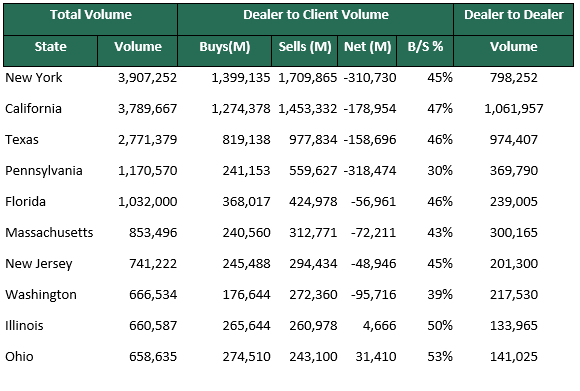

Municipal New Issuance: The first week of May negotiated calendar was comprised of roughly $6.7 billion in volume, with a third of the issuance coming from just 4 issuers. The largest deals for the week were the $1.1 billion Washington State Housing Finance Commission revenue bonds which had the social certificate certification for the two series they issued. The next largest deal was the North Texas Tollway Authority $868 million revenue bonds which consisted of taxable and tax-exempt bonds, this issue was slightly upsized to meet aggressive investor demand. The last notable deal for the week was the $533 million California State Department of Water Resources financing which AmeriVet was co-manager on. The deal was repriced, and yields were lowered as demand for dual exempt bonds in California allowed underwriters to price more aggressively. The lack of general market supply as well as the potential for increases in Federal taxes and increased demand from investors helped to support market levels. Municipal Secondary Trading: Secondary trading for the week totaled approximately $25.7 billion, down from the prior week’s volume of $32 billion. Investors continue to purchase tax-exempt and taxable bonds as 56% of the secondary trading was investors buying from broker-dealers. With the lack of new issue supply, investors are continuing to look for value in the secondary markets as they hope the volume of the new issue calendar increases. According to Bloomberg, customers bids-wanted totaled $2.82 billion for the week slightly down from the weekly average we have had this year. |

|

|

Municipal Spread: After we saw yields rise in the last week of April, the first week of May saw yields decline, with the Bloomberg 10-year benchmark falling by 3.1 basis points to 0.945%. Although we did see a dip in yields, municipal bonds underperformed versus Treasuries as tax-exempt debt maturing in 10 years are now yielding 60.07% compared to 59.95% a week ago. Even with the small drop in yields, we did see the municipal bond curve flatten by 4.5 basis points to 153 basis points for the week, as yields on the long end of the curve fell due to strong investor interest while the short end remained virtually unchanged. |

|

|

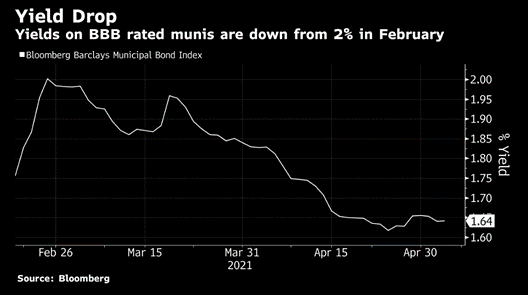

For the ninth straight week municipal bond mutual funds saw positive a weekly inflow in new investor cash. According to Refinitive Lipper US Fund Flow Data investors added roughly $585 million to those funds, this follows last week’s inflow of $1.64 billion and now total $36.28 billion year to date. For the past year, we have seen yields fall to their lowest levels despite state and local governments dealing with decreased tax revenues and other budgetary issues. The saving grace for many states and local governments was the Federal government giving them a lifeline of $350 billion stimulus program to help fill their funding needs. This was a huge boost to issuers as they have been able to lower their borrowing costs as well as help improve the credit quality. We have seen that some lower-rated issuers such as the State of Illinois and New Jersey’s Transportation Trust Fund Authority did which both are BBB rated utilized this opportunity. Last month New Jersey’s Transportation Trust fund issued $1.47 billion to refund outstanding debt. The issue which was well oversubscribed had some maturities being 10-times oversubscribed which allowed underwriters to lower yields and reduce debt service costs. Bonds from the issue are trading higher prices with bonds maturing in 2032 trading with an average yield of 1.76% which is a spread of 73 basis points compared to top-rated bonds down from 78 basis points when those bonds were issued. As yields have been falling many investors continue to seek more yield so many have been moving further down the curve. The area that has been standing out the most in the investment grade spectrum has been the BBB rated municipals. Currently, yields on BBB rated bonds were 1.64% which is down from its highs of the year of 2% which has returned roughly 2.7% for the year and has been beating top rated municipals which have shown a loss of 0.09% for the year. |

|

|

Municipal Supply: This week we are expected to have a negotiated calendar with the size of about $6.2 billion, with two issues being over $500 million in size. The largest issue of the week is the $771 million Georgia, Main St. Gas issue while the second-largest deal for the week is the $709 million Energy Northwest taxable issue consisting of multiple project electric revenue refunding bonds. Another issue of note is the $336 million Dormitory Authority of New York refunding bond issue. With a relatively light calendar, we expect to see very high demand for these bonds as well as some very aggressive pricing. |

|

|