Weekly Muni Snapshot | November 15, 2021

|

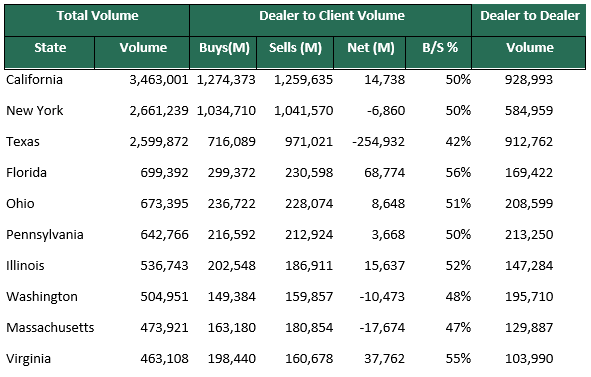

November 15, 2021 Municipal New Issuance: The negotiated calendar for the second week of November totaled to just over $8 billion for the week with only one issuer issuing bonds over $1 billion. Dallas Area Rapid Transit issued $1 billion in bonds with $576.35 million in taxable bonds and $448.96 million in tax-exempt bonds. AmeriVet had a busy week as we were part of two issues on the week, AmeriVet was in the $500 million State of Connecticut special tax obligation bonds as a selling group member as well as the $253 million Pennsylvania Housing Finance Agency revenue bonds as a co-manager. Municipal Secondary Trading: Secondary trading for the week totaled to just about $20.39 billion with 51% of tall secondary trades were clients buying. Secondary trading was very light for the week due to the markets being closed on Thursday for the Veterans Day Holiday. Even with only having four days of trading clients put up $2.51 billion bonds up for the bid down slightly from the prior week of $2.65 billion. |

|

|

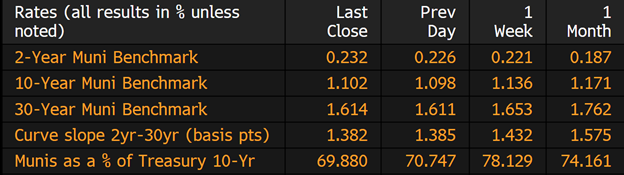

Municipal Spread: Municipal bonds continued their rally this week with the 10-year bonds rallying by 3.4 basis points to fall to 1.10%. With the rally in municipals, they did outperform Treasuries as state and local debt maturing in 10 years is not yielding 69.88% compared to 78.13% a week ago. Ratios one month ago were 74.16%. With yields falling across the bond curve, the gap between short-term and long-term municipal bonds flattened by 5 basis points for the week to 138 basis points. |

|

|

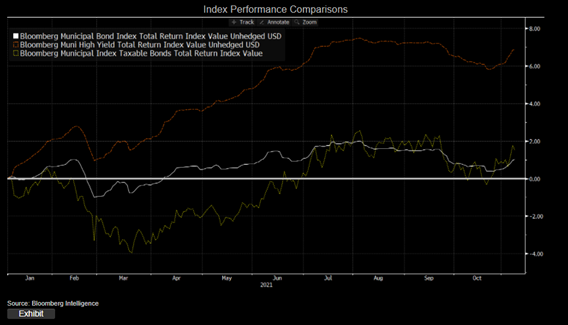

For the 36th straight week investors added to municipal bond mutual bonds to the sum of $1.9 billion for the week ended Wednesday according to Refinitiv Lipper US Fund Flows data. Investors for the week added $1.2 billion to high-yield funds which was the second largest on record as investors continue to pour money into those funds as yields have fallen in the past month and comes after Treasury yields appear to have stabilize below their October peak. The largest inflow into high-yield funds was back in April 2021 to the sum of $1.28 billion. With the end of 2021 in our sights, municipal bonds started off on the right foot but trickled into negative returns but rallied for the most part of the year only to erase those gains in the last two months. Fortunately, the downturn has been short lived, and municipals have rebounded with all three Bloomberg indices showing positive returns. With the economy improving high-yield funds (LMHYTR) benefited the most returns compared to the Bloomberg Municipal (LMBITR), the Bloomberg Taxable Muni (BTMNTR). High yield bonds have earned about 7.2% this year compared to just 1.1% of the overall market for municipals, the widest in performance since 2012. |

|

|

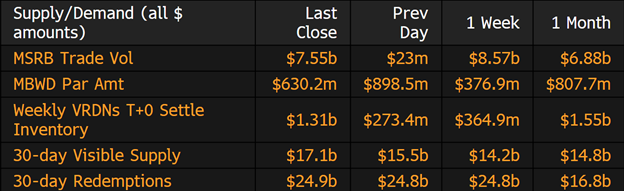

Municipal Supply: The negotiated will have an expected total volume of roughly $8.7 billion for the week with three deals being over $1 billion. Grand Canyon University will be issuing $1.2 billion in taxable bonds using a corporate CUSIP to help refinance outstanding debt including revolving credit facility used to purchase property, plant, and equipment assets. The State of Mississippi will be issuing tax-exempt and taxable bonds to the sum of $1.1 billion. The California Health Facilities Financing Authority will be issuing $1 billion in revenue bonds for the Cedars-Sinai Health Systems. Supply is expected to increase as requests for trading tickers for new municipal securities rose about 5% in October versus the prior month. Overall municipal CUSIP requests have been down about 6.4% through October. |

|