Weekly Muni Snapshot | October 11, 2021

|

October 12, 2021

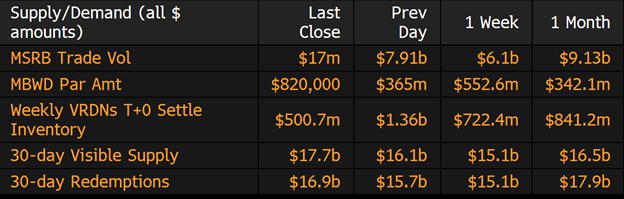

Municipal New Issuance: Negotiated issuance for the week totaled to about $9.9 billion for the week just a touch higher than the previous total negotiated issuance last week. The largest deal of the week which was the only deal above $1 billion was the $1.5 billion Alabama Federal Aid Highway Finance Authority which issued taxable bonds as well as tax-exempt bonds. The second largest deal of the week was the Riverside County California Transportation Commission Toll Revenue which issued $437 million in tax-exempt bonds. AmeriVet was in one issue for the week as a co-manager which was the $216 million School District of Philadelphia. The School District of Philadelphia saw enough demand for their bonds as they tightened from its original pricing.

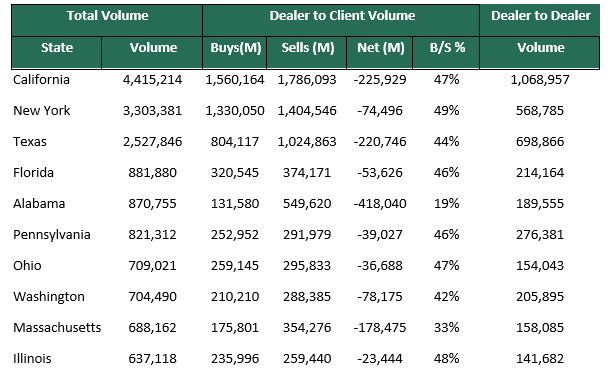

Municipal Secondary Trading: Secondary trading continues to pick up as the weekly total trading totaled to about $25.7 billion with 56% of the total trading was dealers selling to customers. With yields climbing for the third straight week many continue to see value in purchasing bonds that were expensive just a month ago. Customers this week put up less bonds up for the bid with customers only putting up $2.8 billion compared to the previous week of $3.1 billion. |

|

|

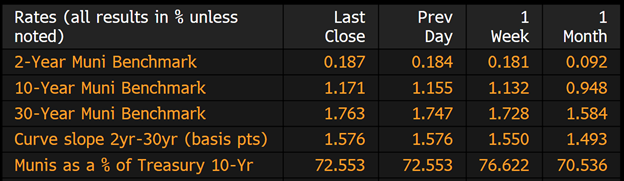

Municipal Spread: Municipal bonds continued there slump this week with yields on the 10-year notes rising by 3.9 basis points to 1.17% in the past week marking a 12.4 basis point rise in 2 weeks. With the rise in yields we did continue to see the municipal bond curve steeped as it rose by 2.6 basis points to 156 basis points for the week. Although, municipal bonds did weaken they still fared better than Treasuries as bonds maturing on 10 years are now yielding 72.5% of Treasuries compared to 76.62% a week ago but still higher a month ago which was 70.53%. Even though, ratios have risen in the past few months they are still considered far from ‘Fair Value’ on ratios. Long-term averages for 10- and 30-year Muni-U.S. Treasuries ratios measure at 95%-102% respectively compared to what we are seeing now which is 74% to 82%. |

|

|

Municipal bond Inflows for the week totaled to just $37 million a drop of 61% from the previous week of $408 million, according to Refinitiv Lipper US Fund Flows Data. This was the weakest weekly inflow we have seen since the first week of March where we saw an outflow. High yield funds which were popular for the better part of the year saw its second week straight of outflows with those funds losing $460 million and long-term funds also losing about $344 million. High yield funds for the year have been averaging about $358 million of inflows and to go to an outflow of $460 million should not go unnoticed.

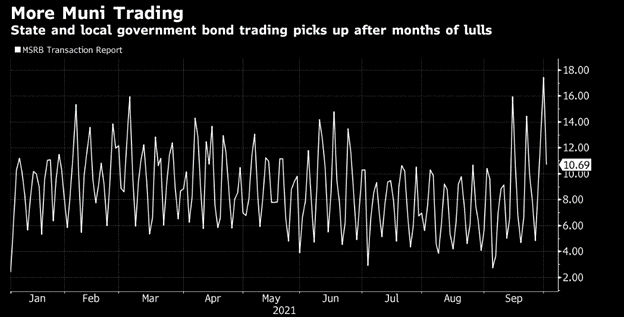

For the past few month’s traders have been scrounging for bonds that were worth buying but with 10-year municipal bond yields now at its highest relative to Treasuries in seven months many are now seeing a chance to purchase or swap out of bonds they bought earlier in the year. With supply expanding over the next 30 days with $14.8 billion expected trade volume should increase as well. |

|

|

Municipal Supply: With a shortened holiday week for Columbus Day on Monday, the negotiated calendar will have an expected volume of just over $4.3 billion. There will only be two issues that will have a total expected size of over $300 million, which will be the $377 million Indiana Finance Authority Revenue bonds for the Deaconess Health Systems, and the $365 million Texas Water Development Board Revolving Fund Revenue Bonds. AmeriVet will be in one issue for the week which will be the $125 million New York City Housing Development Corp. |

|

|