Weekly Muni Snapshot | September 7, 2021

|

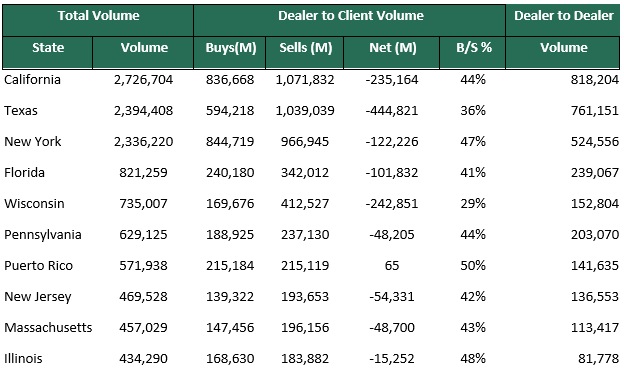

Municipal New Issuance: The negotiated calendar volume for this past week totaled $4.6 billion as many issuers waited to come to market until after the Labor Day holiday weekend. The largest deal for the week covered calendar was the $950 New York City Transitional Finance Authority issue, AmeriVet was a syndicate member on that deal. The State of Wisconsin issued this week with $326 million in taxable bonds and both financings saw solid investor demand. Municipal Secondary Trading: Secondary trading for the week continued the recent trend of lower overall volume with $18.6 billion in trades for the week due as many investors and traders took the last week of summer off. With trading volume down, so were customer bids-wanted lists, according to Bloomberg customers put up roughly $1.7 billion out for the bid which Is down from the prior week’s total of $2.71 billion. We expect to see secondary trading activity pick up in the coming week as supply and investor participation should be more robust. With overall market conditions remaining positive for issuers the level municipal bond issuance is anticipated especially in advance of the potential for the being to taper their level of asset purchases. |

|

|

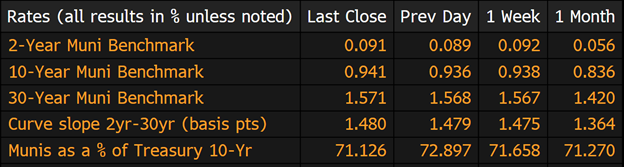

Municipal Spread: For the fourth straight week municipal bond yields rose slightly with the 10-year benchmark yield increasing by 0.3 basis points to 0.941%. The last few weeks of August have been pretty uneventful as investors have remained cautious, but with the expected pickup in activity in both primary and secondary markets and with the potential for slightly higher yields we anticipate a solid increase in overall market volume of deals. With light trading in the municipal market, it comes as no surprise that yields remained fairly stagnant but it is interesting to note that the municipal market outperformed Treasuries ever so slightly for the week as the 10-year ratios is now 71.26% compared to 71.65% a week ago. Although, yields fell for the week the municipal bond curve did steepen slightly by 0.5 basis points to 148 basis points. |

|

|

The month of August posted a small loss with the Bloomberg Municipal Bond Index (LMBITR) showing a negative -0.37% return. This reduces 2021 returns to 1.53% down from the end of July where returns were 1.90%. The month of August is usually one of the slowest months of the year for municipal bonds but 2021 was the third worst August of the past decade. August losses could be coupled by many market participants being out on vacations, the delta variant increasing in the U.S., and ratios reducing the level of overall activity. Lower-rated bonds did fair better than higher-rated bonds as Aaa bonds lost 0.40% and Baa bonds lost only 0.36% for the month which shifted returns to 0.45% and 4.84% respectively. Taxable bonds also posted a loss with 0.19% for the month lowering their year-to-date returns of 1.76%. |

|

|

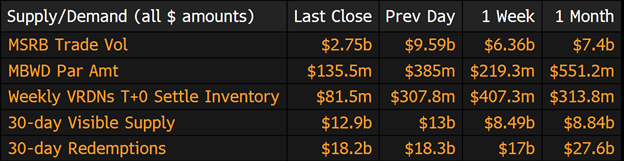

Municipal Supply: With the holiday shortened week the negotiated calendar will be very light with an expected volume of $3.04 billion. The largest deal for the week will be the $1 billion Piedmont Healthcare Taxable bond issue. The next largest deal for the week is the $817 million Hampton Roads Transportation Accountability Commission notes deal. |

|

|