AmeriVet Weekly Muni Snapshot

|

Municipal New Issuance: Last week’s negotiated calendar totaled to just over $9.2 billion with the largest deals of the week being the $3 billion CommonSpirit Health issue followed by the $2.8 billion New York State Dormitory Authority issuance. The third largest deal of the week was the $718 million Colorado Health Facilities Authority issue. The Los Angeles Department of Water and Power issued roughly $372 million. CommonSpirit saw large demand for both its taxable and tax-exempt debt as the taxable bonds tightened by 10 basis points and the tax-exempt portion tightened by as much as 2 basis points. Overall, CommonSpirit saw about $2.2 billion in orders for the taxable bonds and $6.5 billion for the tax-exempt bonds. State and local governments have sold roughly $82 billion so far this year which is approximately 30% higher than 2023. |

|

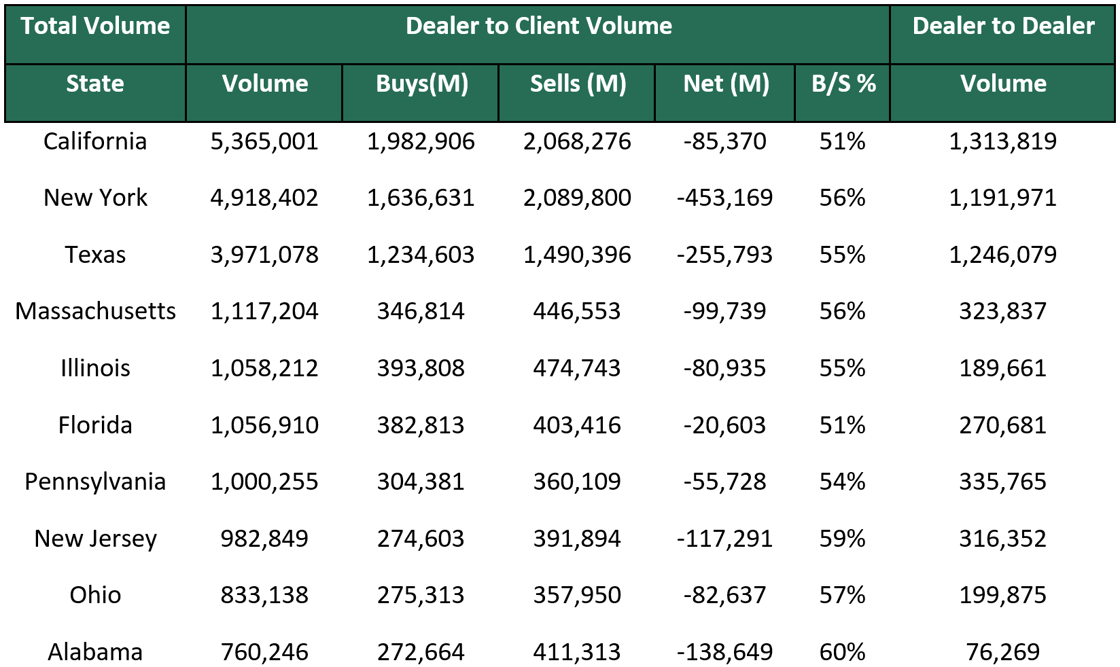

Municipal Secondary Trading: Secondary trading for the week totaled to just over $32.47 billion with 54% of the trades being dealer sells. According to Bloomberg, clients put up roughly $5.48 billion up for the bid with last Wednesday having the largest amount of bids-wanted totaling to approximately $1.25 billion up for the bid. |

|

|

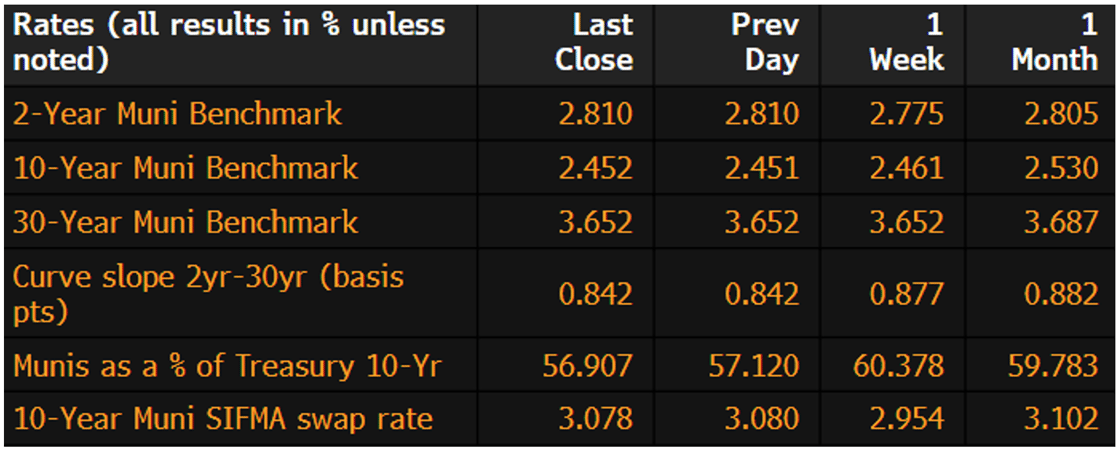

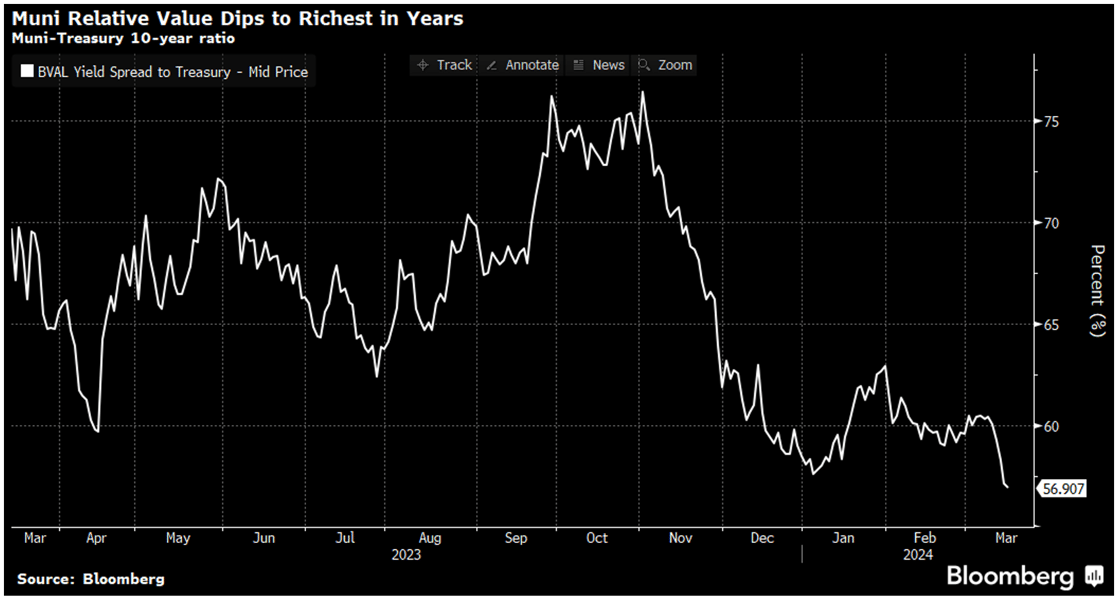

Municipal Spreads: Last week, muni yields fell slightly with yields on 10-year notes falling by .9 basis points to finish the week at 2.45%. With muni yields falling, we did see munis outperform Treasuries as the 10-year ratio is now at 56.90%. Just prior to last week, that ratio was at 60.38%. We also did see the muni curve flatten last week by 3.5 basis points to end the week at 84 basis points. |

|

|

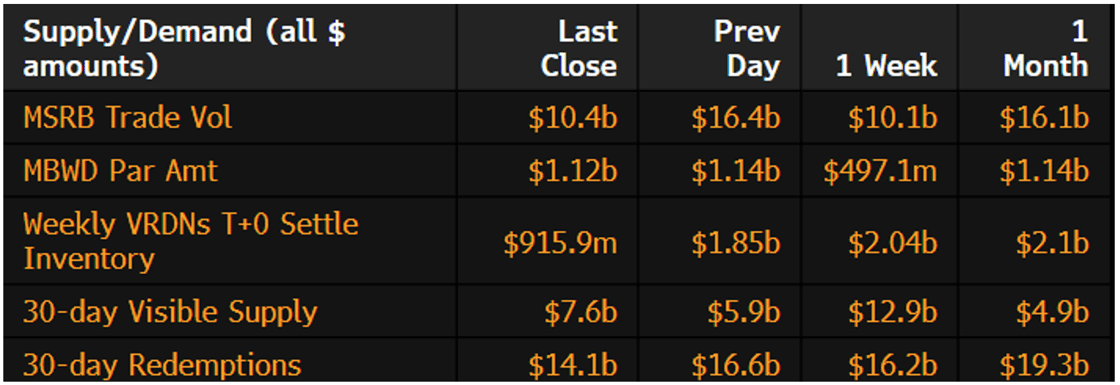

Municipal bond mutual funds continue to see inflows as investors added roughly $295.5 million into the funds last week. This marks the third consecutive week of inflows and follows the prior week’s inflow of $869 million. This is positive news as we are starting more confidence in the markets, yields falling, and an increase in supply as many investors are jumping back in the fixed income markets before any anticipated rate cuts begin. |

|

With just two weeks left in the first quarter of 2024, we have seen a complete turnaround from the start of the year. 2024 had a rough start coming off a huge rally in December that led to a loss of .51% in January to today where we are roughly flat for the year due to the rally in the markets. The downside to this is that we have pushed valuation to a three-year high as the 10-year ratio has fallen to 56.9%. This is the lowest the 10-year ratio has been since June 2021. Investors continue to overlook the richness of munis with new issues coming to market being well oversubscribed to as much as five times as yields are still attractive from five years ago. |

|

|

Municipal Supply: This week, the negotiated calendar will have an expected volume of $5.2 billion with the 3 issuers covering just under half of the issuance for the week. The largest deal of the week will be the $1.2 billion Metropolitan Transportation Authority which AmeriVet will be participating in the Selling-Group. The next largest deal of the week will be the New York State Environmental Facilities Corporation which will sell roughly $722 million. The third largest deal of the week will be the $500 million New Jersey Turnpike Authority issuance. |

|