AmeriVet Weekly Muni Snapshot

|

Municipal New Issuance: Last week’s negotiated calendar totaled to approximately $4.35 billion for the week with the largest deal being the State Public Works Board of the State of California which AmeriVet participated as a Co-Manager on. The State Public Works Board of the State of California issued $639 million in tax-exempt bonds and $230 million in taxable bonds. The second largest deal of the week was the National Finance Authority for the Wheeling Power Co., which issued $450 million in taxable bonds. AmeriVet was also in one other deal this past week as a Selling-Group-Member which was the New Hampshire Housing Finance Authority which issued $50 million in tax-exempt bonds and $25 million in taxable bonds. |

|

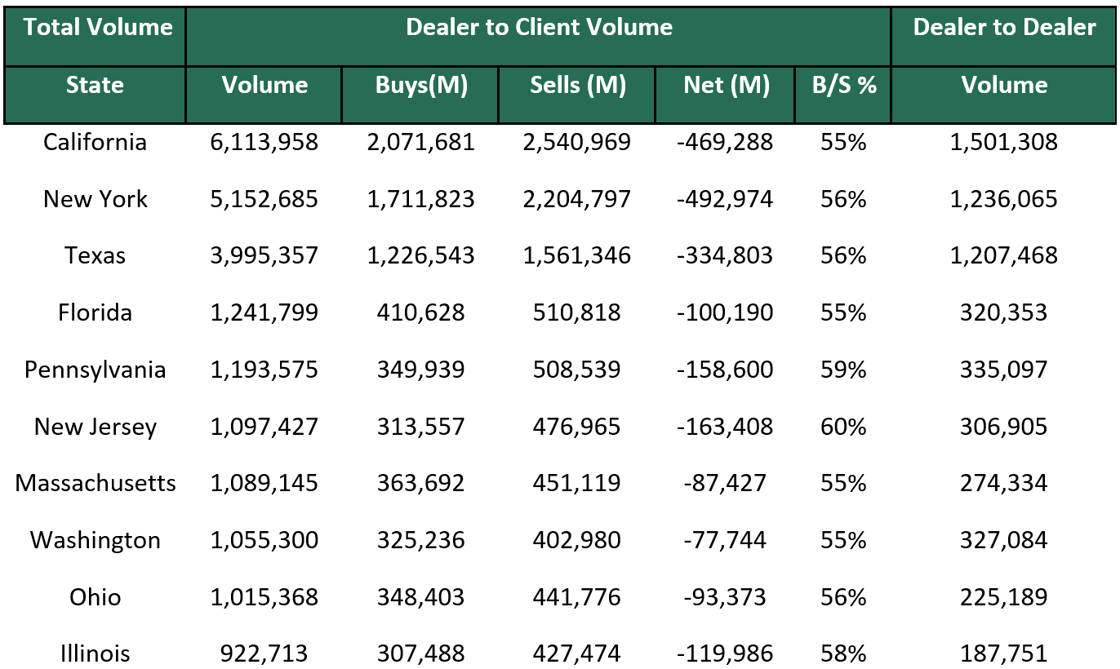

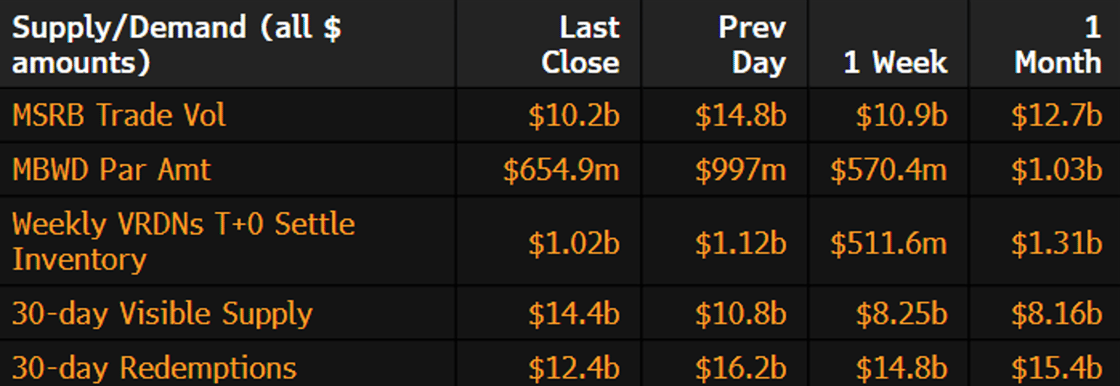

Municipal Secondary Trading: Last week, secondary trading totaled to about $35.89 billion for the week with 56% of all trades being dealer sells to clients. According to Bloomberg, clients put up approximately $4.46 billion with Wednesday have the largest volume of bids wanted which was just over $1 billion. |

|

|

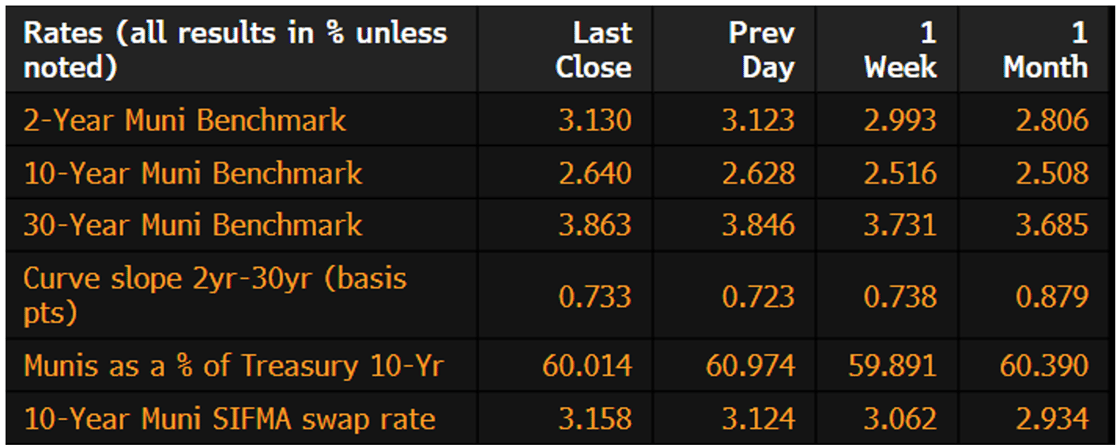

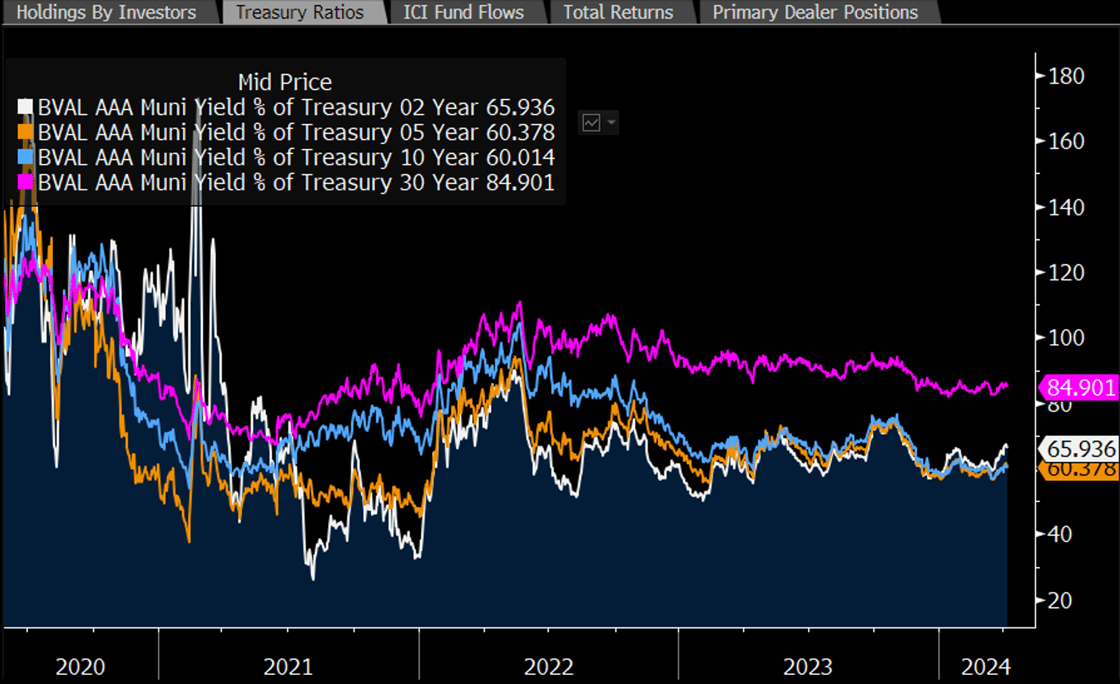

Municipal Spreads: For the first week of the second quarter of 2024, muni yields rose, marking the third week in a row of rising yields. Last week, yields on 10-year notes rose by 12.4 basis points to 2.64% bringing the 10-year above 2.60% for the first time since December 2023. With muni yields rising, we did see munis cheapen compared to Treasuries as the 10-year ratio is now yielding 60.01% compared to the prior week when the 10-year ratio was yielding 59.89%. The muni curve did flatten this past week by 0.5 basis points to end the week at 73 basis points. |

|

|

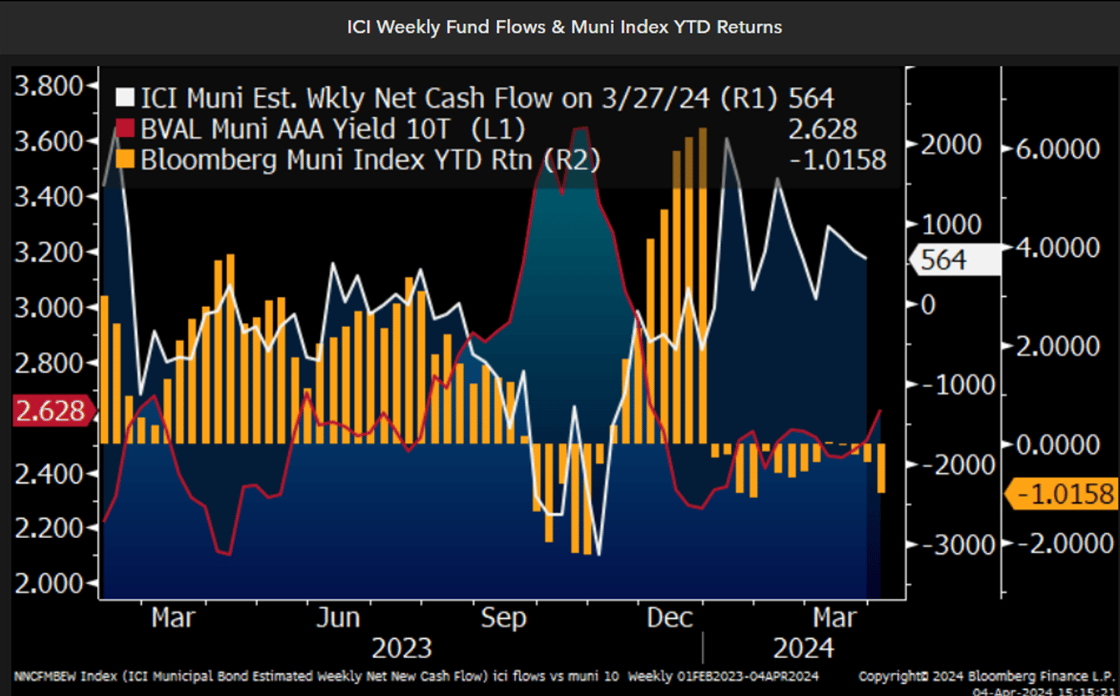

Municipal bond mutual funds continue to see inflows as investors added roughly $80 million to those municipal bond funds according to LSEG Lipper Global Fund Flows data. This follows last week’s inflow of $447 million and marks the seventh consecutive week of inflows. |

|

|

Munis continue to cheapen across the curve as we have seen ratios continue to inch back up to their normal averages. Three weeks ago, we saw the 10-year ratio hit their four year low of 59.90%, and since that four year low, we have seen the 10-year ratio move higher by about five percentage points. With stronger than expected economic numbers in recent weeks, most particularly in the recent March payroll numbers, we should continue this trend of higher yields to continue. Federal Reserve Bank of Dallas President Lorie Logan stated on Friday that it’s too early to consider cutting interest rates. With CPI coming later this week, we could start to see how many cuts we could actually expect for 2024. If inflation continues to trend flat, it will be interesting to see how the Fed reacts and if they change their tune to not cutting rates at all this year. |

|

|

Municipal Supply: This week, the negotiated calendar will have an expected volume of $5.6 billon with the largest deals of the week being the $632 million Commonwealth of Kentucky, followed by the $610 million Dormitory Authority of the State of New York issuance. AmeriVet will be in one issue this week as a Selling-Group-Member which will be the $39 million Minnesota Housing Finance Agency Residential Housing Finance Bonds issuance. |

|