AmeriVet Weekly Muni Snapshot

|

Municipal New Issuance: Last week’s negotiated calendar totaled to just over $6 billion with the largest deals being the $735 billion Massachusetts Development Finance agency, followed by the Commonwealth of Kentucky which issued about $684 million, and the third largest deal of the week was the $600 million New York State Dormitory Authority issuance for Cornell University. AmeriVet was in one issue this past week as a Selling-Group-Member for the Minnesota Housing Finance Agency’s Residential Housing Finance Bonds issuance. |

|

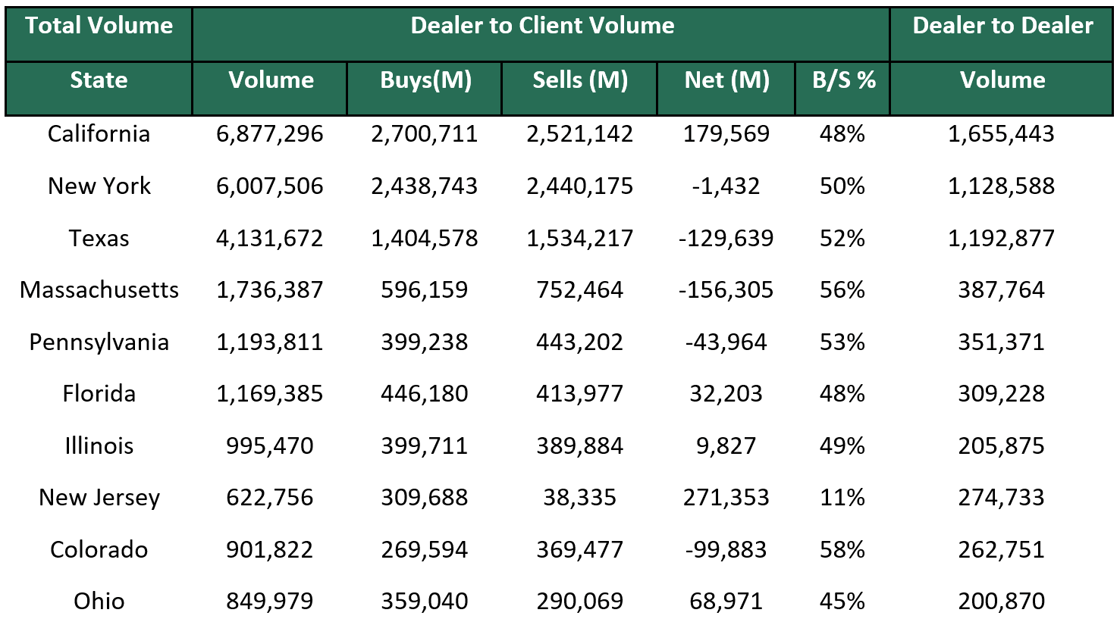

Municipal Secondary Trading: Last week, secondary trading totaled to roughly $37.99 billion with 51% of all trades being dealer sells to clients. According to Bloomberg, clients put up approximately $6.17 billion up for the bid last week, compared to $4.46 billion from the prior week. |

|

|

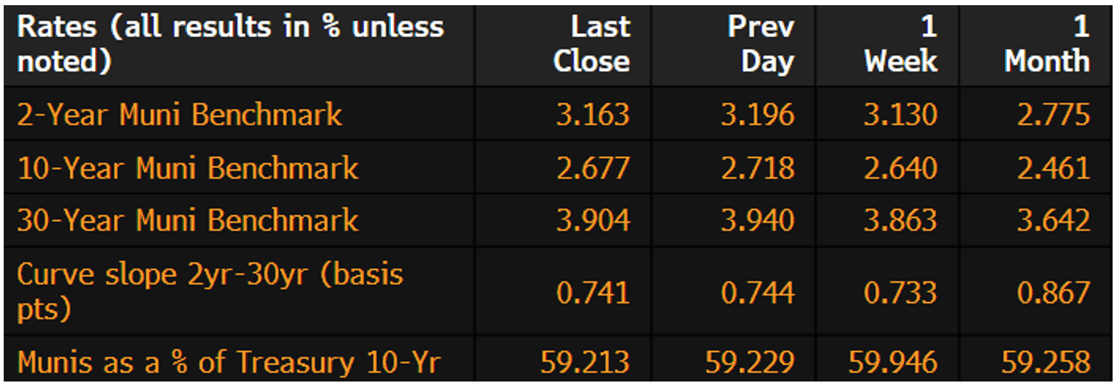

Municipal Spreads: We continue to see yields rise this month as 10-year notes rose this past week by 3.7 basis points to close the week at 2.67%. In the past thirty days, munis have risen by an average of 26 basis points. Although yields rose this past week, munis were able to outperform Treasuries this past week as 10-year munis are now yielding 59.21% of Treasuries compared to the prior week when the ratio was at 59.94%. The muni curve did steepen this past week by .8 basis points to close the week off at 74 basis points. |

|

|

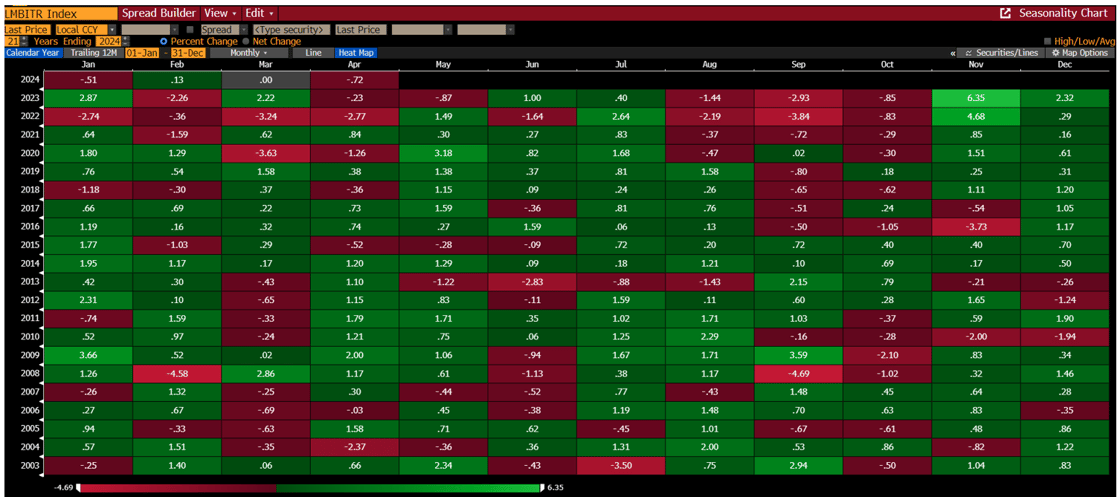

Although we continue to see yields rise, investors are continuing to add to municipal bonds funds. According to LSEG Lipper Global Fund Flows data, investors added about $414 million to those funds and this follows the prior week’s inflow of $79.9 million. This marks the seventh consecutive week of inflows. |

|

April continues to be harsh for munis as munis have given up roughly 96 basis points in the first 2 weeks of April bringing this years, year-to-date loss to 1.11%. Since the start of April, we have seen munis rise by an average of 14.5 basis points across the curve. If this trend continues, this will be the third successive loss for April. With the hotter than expected inflation number earlier in the week which sparked a sell off in Treasuries and munis, many are beginning to accept the possibility of rate cuts being pushed into Q4 2024 or even 2025. |

|

|

Municipal Supply: This week, the negotiated calendar will have an expected volume of $5.5 billion with the largest deals being the $1.5 billion State of Florida taxable issue for the Brightline Trains Florida LLC, followed by the $527 million Board of Regents of the University of Texas System. The next largest deal of the week will the $450 million New York City Municipal Water which AmeriVet will be participating in the Selling-Group. AmeriVet will also be in one other issue for the week as a Selling-Group-Member for the Maryland Department of Housing and Community Development which will be issuing $210 million in taxable bonds and $40 million social bonds. |

|