AmeriVet Weekly Muni Snapshot

|

Municipal New Issuance: Last week’s negotiated calendar totaled to just over $6.8 billion with the largest deal being the $1 billion Florida State Board of Administration issuance. The second largest deal of the week was the $941 million Energy Southeast Alabama issue. The Texas University Board of Regents issued $801 million and was the third largest deal of the week. AmeriVet participated in two issues this past week as a Selling-Group-Member which were the $788 million New York City Municipal Water Finance Authority which upsized their deal from $447 million during the pre-marketing to $788 million. AmeriVet was also in the $49 million New Mexico Finance Authority Revolving Fund Revenue Bonds, Series 2024A issuance. |

|

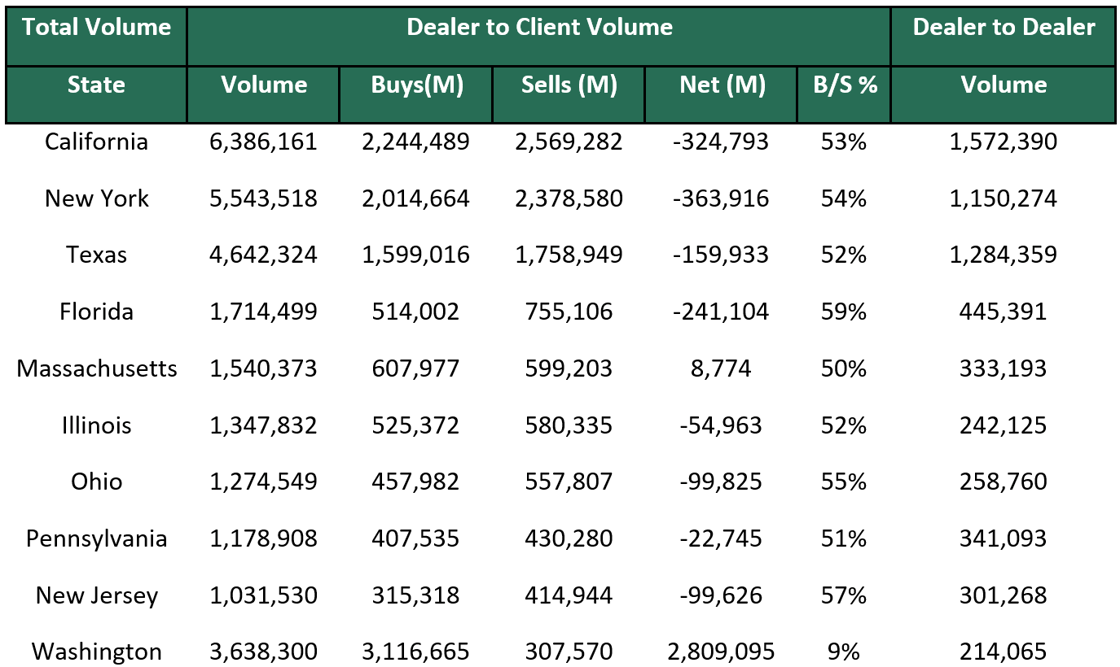

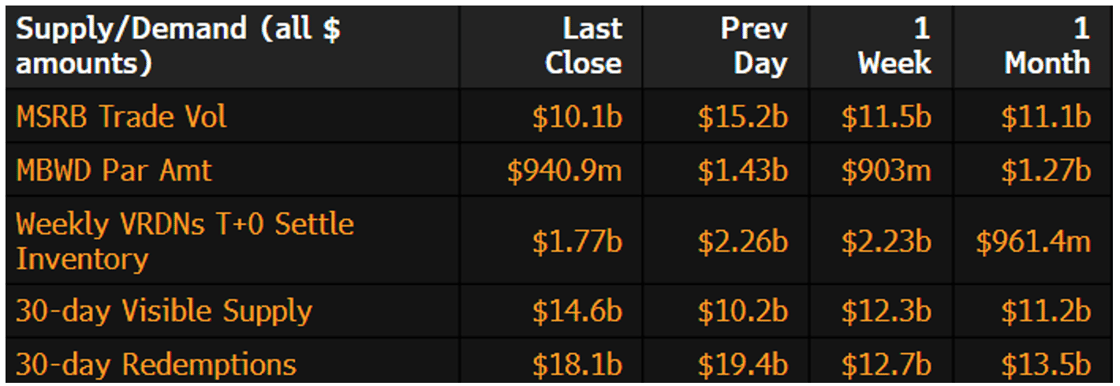

Municipal Secondary Trading: Last week, secondary trading totaled to roughly $39.49 billion with 54% of all trades being dealer sells to clients. According to Bloomberg, clients put up roughly $6.172 billion up for the bid which is slightly below the total amount of bids from the prior week’s total of $6.175 billion. |

|

|

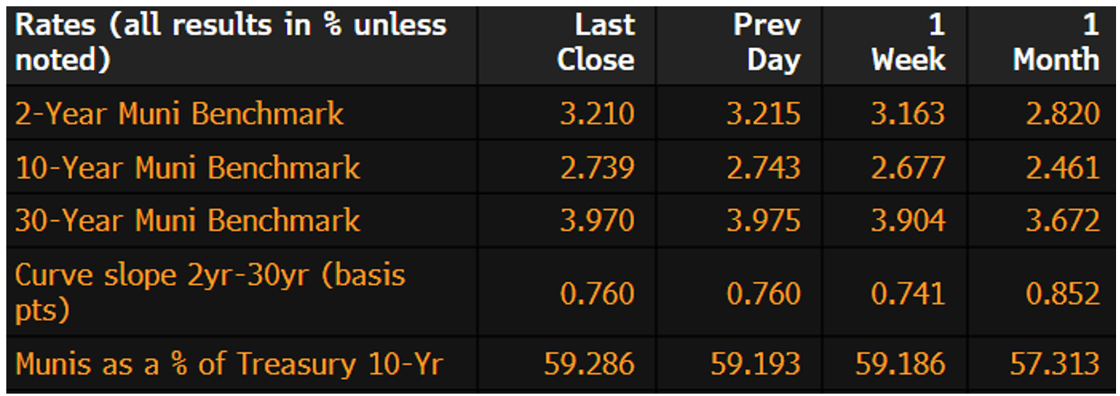

Municipal Spreads: For the fifth straight week, the markets saw muni yields rise as 10-year notes rose this past week by 6.2 basis points to end the week at 2.74%. Since the start of the month, we have seen muni yields rise by an average of about 20.5 basis points across the curve. With yields rising this past week, munis were still able to outperform Treasuries slightly as 10-year notes are yielding 59.28% of Treasuries, compared to the prior week when the ratio was at 59.18%. We did see a slight steeping of the curve this past week with the curve steepening by 1.9 basis points this past week to 76 basis points. |

|

|

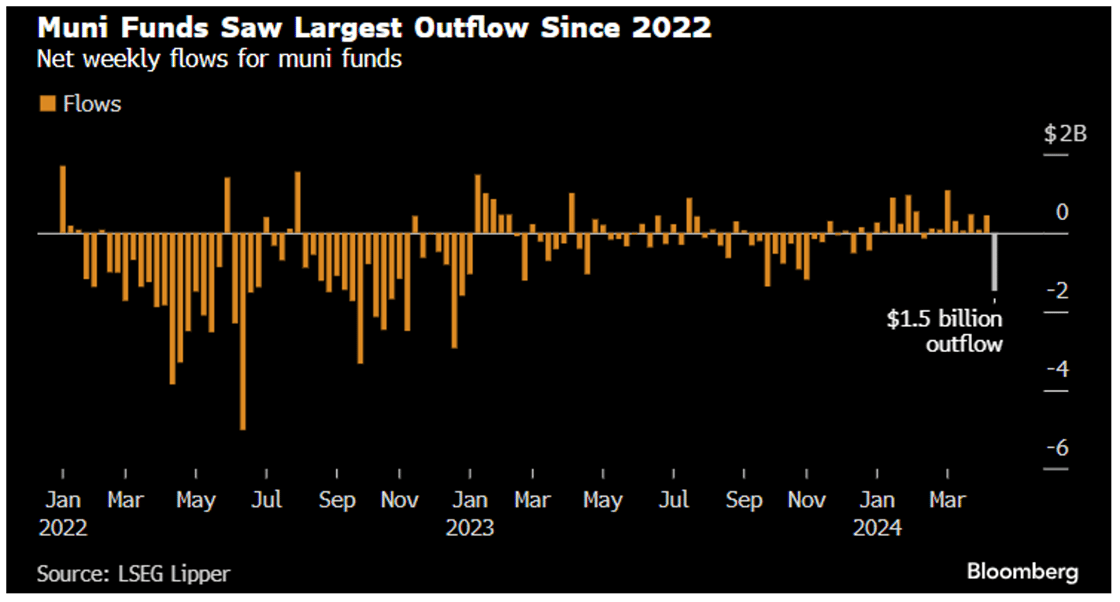

According to LSEG Lipper Global Fund Flows data, for the first time in eight weeks, investors pulled their investments out of municipal bonds funds this past week. This is the largest outflow since December 2022 as investors pulled about $1.5 billion from those funds. This was expected as the market has been experiencing selling pressure due to higher rates, as well as investors selling after the tax-deadline in order to pay off any income taxes, and to protect returns. |

|

|

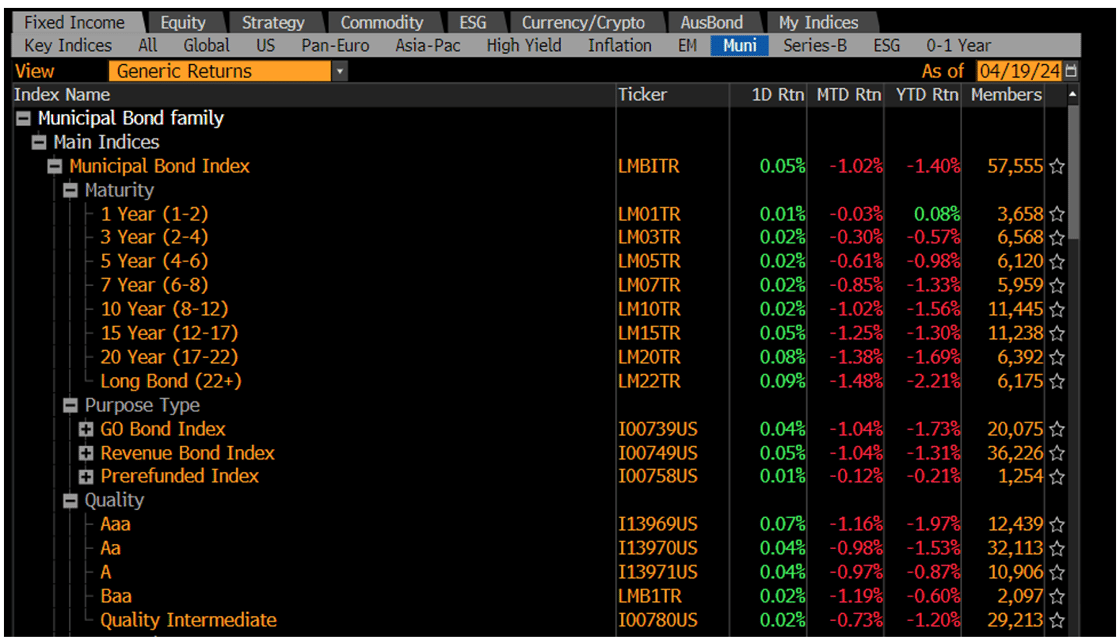

April continues to be a tough month for munis as munis continue to dip into the red with month to date returns of -1.02% which brings the total year-to-date return of -1.40%. Since the start of April, 10-year Treasuries have risen about 40 basis points while 10-year munis have risen 20 basis points. With the potential of any rate cuts in 2024 dwindling, we are seeing munis continue to follow suit with Treasuries. This rate move has pushed us into bearish territory once again as clients continue to grapple with the possibility of no rate cuts in the near future. |

|

|

Municipal Supply: This week, the negotiated calendar will have an expected volume of $12.1 billion with the largest deals of the week being the $2.9 billion Los Angeles Unified School District followed by the $2.2 billion Florida Development Finance Corporation for the Brightline Florida Passenger Rail Project. The net largest deal of the week will be the City of Houston, which plans on selling $841 million in refunding bonds. AmeriVet will be 2 deals this week, which will be the Maryland Department of Housing and Community Development which plans on selling $210 million in taxable bonds and $40 million in tax-exempt bonds. AmeriVet will also be participating as a Co-Manager for the Massachusetts Housing Finance Agency which plans on issuing $124 million with a mix of AMT, Non-AMT, and Taxable bonds. |

|