AmeriVet Weekly Muni Snapshot

|

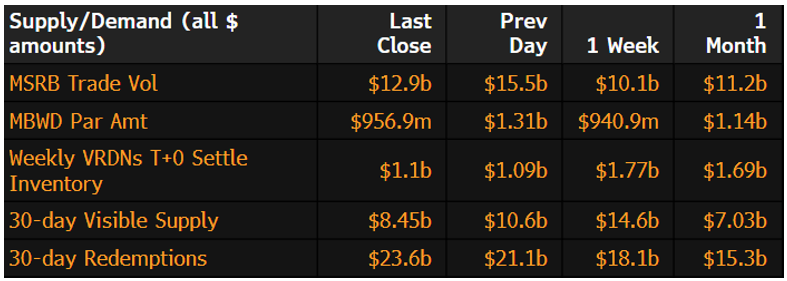

Municipal New Issuance: Last week’s negotiated calendar totaled to just over $13.3 billion with the largest deal of the week being the $3.1 billion Brightline Florida Passenger Rail project which saw high demand due to the high yield it provided. The second largest deal of the week was the $2.9 billion Los Angeles Unified School District issuance followed by the Florida Development Finance Corporation which sold $314 million. AmeriVet participated in two deals this past week, the first as a Co-Manager for the Massachusetts Housing Finance Agency which issued $76 million in tax-exempt bonds and $47 million in taxable bonds. AmeriVet also participated in the Selling-Group for Maryland Department of Housing and Community Development which sold $40 million in tax-exempt bonds and $210 million in taxable bonds. |

|

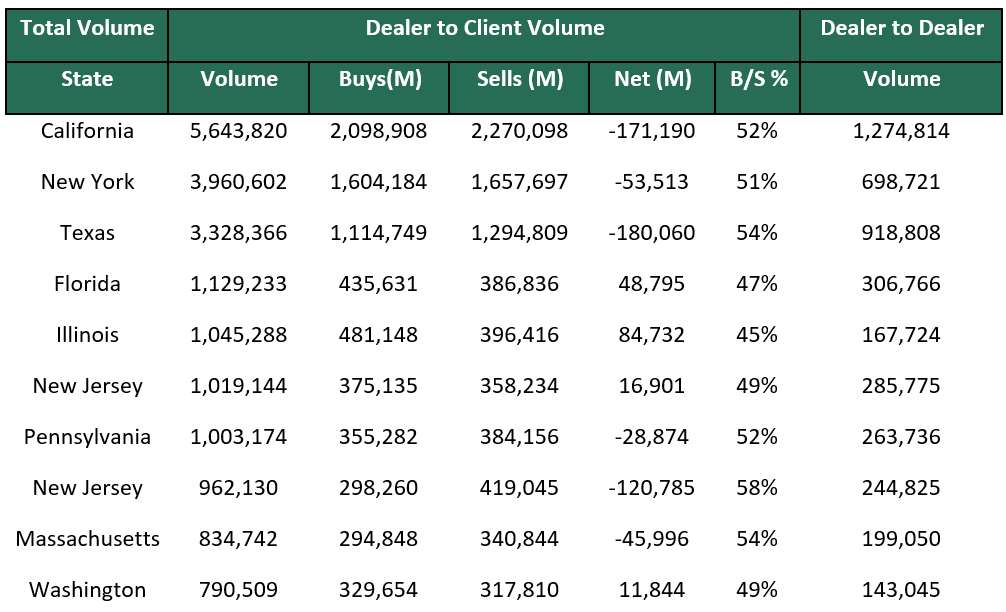

Municipal Secondary Trading: Last week, secondary trading totaled to roughly $30.37 billion with 51% of all trades being dealer sells to clients. According to Bloomberg, clients put up approximately $6.494 billion up for the bid which is above the total amount of bids from the prior week’s total of $6.172 billion. |

|

|

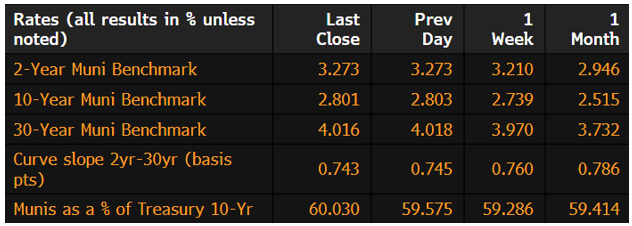

Municipal Spreads: For the sixth straight week, markets saw muni yields rise as 10-year notes rose this past week by 6.2 basis points to end the week at 2.80%, hitting a year-to-date high this past week. With the muni curve hitting new year-to-date highs, munis underperformed Treasuries as 10-year munis are now yielding 60.03% of Treasuries. Compared to the previous week, that same ratio was at 59.28%. We continue to see the muni curve flatten this past week, as the curve flattened by 1.7 basis points to close the week at 74 basis points. |

|

|

According to LSEG Lipper Global Fund Flows data, inflows returned to municipal bond funds as investors added about $200 million to the funds following a week of outflows. This follows to prior week’s outflow, the largest since Dec 2022, of $1.47 billion. |

|

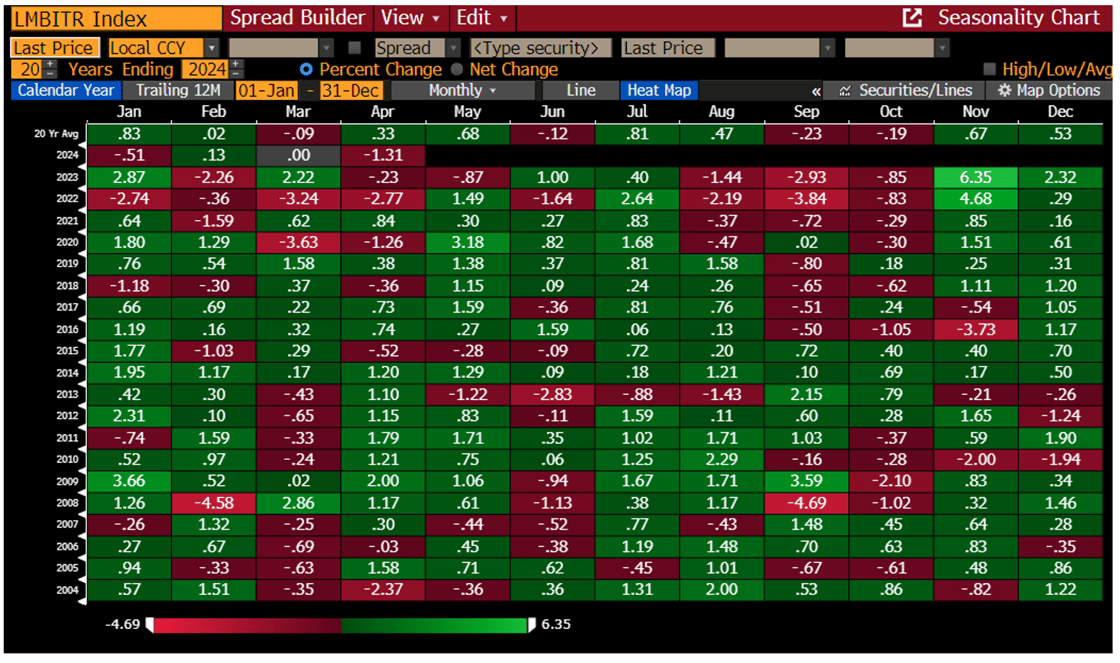

Munis are continuing to be on track to have the second worst April returns in almost 20 years as yields continue to trend higher as the likelihood of a Fed Reserve interest rate cut looks more and more unlikely. Although munis are down roughly 1.31% for the month, we are still far from our worst returns for April which was reached in 2022. We should still be cautious as we anticipate volatility in the markets as well as rising yields until we get a concrete time table of when the Fed may cut rates. |

|

|

Municipal Supply: This week, the negotiated calendar will have an expected volume of $5.28 billion. The largest deals of the week will be the $1.9 billion South Carolina Jobs & Economic Development Authority issue, followed by the Port Authority of New York and New Jersey which plans on selling $649 million, and the Board of Regents of Texas A&M University will issue approximately $425 million. |

|