AmeriVet Weekly Muni Snapshot

|

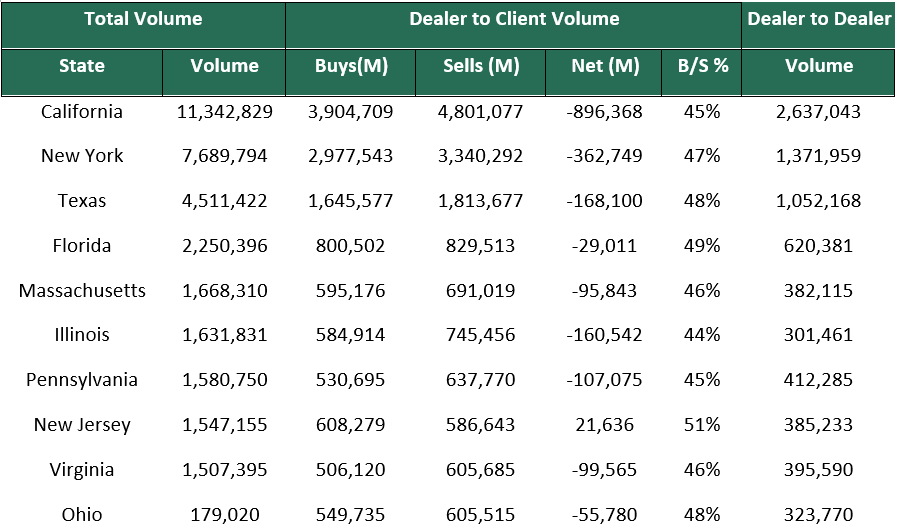

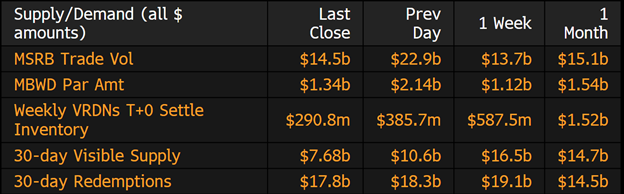

Municipal New Issuance: The final week of April had a total volume of just over $10 billion with the largest deal of the week taking up almost a third of the issuance. University of California Regents issued $3 billion bonds last week with $1.1 billion of it being taxable bonds. Michigan Finance Authority issued $900 million in revenue bonds. Although the calendar looked fairly large for the week, it should also be noted that the bulk of the issuance came from just six issuances. One interesting note regarding University of California deal was that they downsized the taxable portion by $600 million and shuffled those bonds over the tax-exempt portion as investors had more interest in the tax-exempt bonds as well as taxable bonds have underperformed more than tax-exempt bonds. Municipal Secondary Trading: The final week of April was very volatile with secondary trading totaling to over $54 billion for the week. This was one of the largest trading weeks we have seen since the March 2020. With a very active secondary, we continue to see high number of bids-wanted from clients. According to Bloomberg, clients put up $ 9.6 billion in bids-wanted smashing the previous weeks high of $8.24 billion. |

|

|

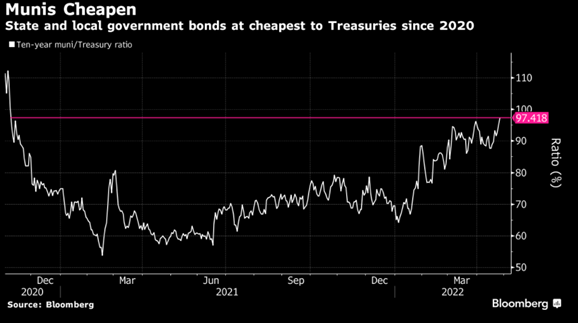

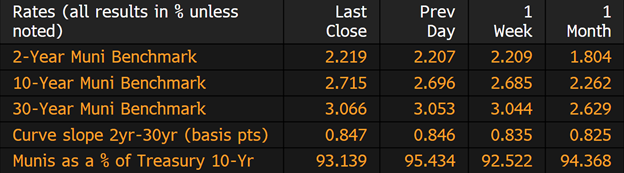

Municipal Spread: Municipal bonds had a quiet week to close out a rough month as yields only rose slightly, with 10-year notes rising by just 3 basis-points to 2.71%. To start the month, 10-year notes were at 2.26% and on January 1st, yields were at 1.06%, a 165 basis-points difference. With the no movement in US Treasuries this week, municipal bonds did lag compared to Treasuries as 10-year ratios are now at 93.14%. Those ratios did hit 98.38% on Tuesday April 26th, the highest since November 2020. We also saw a slight steepening of the curve as the gap between yields on short-term and long-term notes steepened by 0.8 basis points to 85 basis-points for the week. |

|

|

|

For the 11th straight week investors pulled money of municipal-bond mutual funds last week to the sum of about $2.88 billion according to Refinitiv Lipper US Fund Flows data. This outflow follows the prior week’s outflow of $3.5 billion and marks a total streak of losses of $47.4 billion, with investors withdrawing $45.9 billion from municipal funds year-to-date. |

|

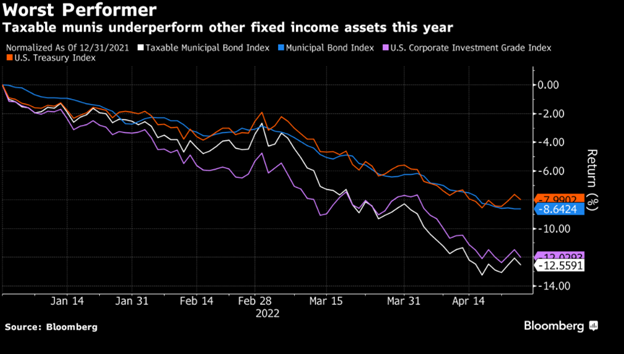

Taxable municipal bonds were one of the bright spots in 2020 and 2021, but for 2022 that is a different story. Even as other fixed income asset classes have struggled mightily this year taxable municipal bonds are among the worst performers so far. Taxable municipals have underperformed and have fallen by 12.6% so far this year, while tax-exempt bonds have fallen by just 8.6%, corporate bonds are down just 12%, and Treasuries have declined by just 8%. With a rising rate environment, taxable municipals have struggled to make any returns as they have an average duration of 9.2 years while investment grade corporates have an average duration of 8 years, and the longer out in the curve, you see the worst returns. With taxable bonds being down, so has issuance this year, with issuers just selling $21.7 billion in long term notes this year, a decrease of 37% from the same period last year. |

|

|

Municipal Supply: The first week of May will have a very light calendar once again as many issuers continue to hold off on issuing until rates stabilize. This week we anticipate a total volume of roughly $2.8 billion for the week with one deal taking up a third of the expected volume. The largest deal for the week will be the $945 million Triborough Bridge and Tunnel Authority refunding bonds, which AmeriVet will be a Selling-Group-Member. The state of North Carolina will be issuing $300 million in revenue bonds for highway improvements. |

|