AmeriVet Weekly Muni Snapshot

|

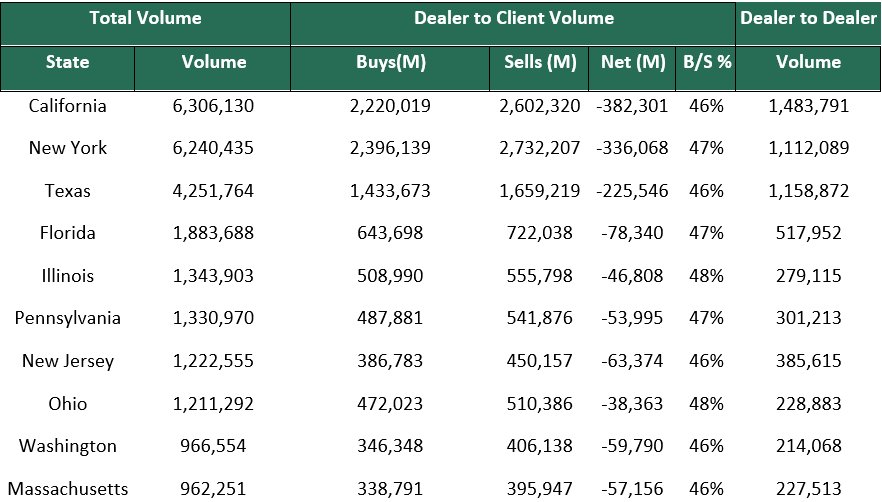

Municipal New Issuance: The Negotiated calendar for the second week of June totaled to just roughly $4.75 billion with many issuing ahead of the all-important CPI number that came on Friday. The largest deal of the week was the $234 million Texas Water Development Board who issued green revenue bonds. AmeriVet was in two deals for the week including the $115 million New York City Housing Development Corporation as a Selling-Group-Member and the $18 million Rhode Island Health and Educational Building Corporation as a Co-Manager. Both issues were downsized from their original expected size. Municipal Secondary Trading: Secondary trading volume totaled to just over $40 billion for the week which has been lower than the average trading volume we are used to seeing in this volatile year. Majority of the trading was done prior to Friday’s CPI number which was unexpectedly higher than many had expected. Customer’s bids-wanted totaled to about $7.1 billion for the week as many are selling due to clients pulling funds out of mutual funds. |

|

|

Municipal Spread: The two-week rally was short lived as yields rose again for the week with yields on 10-year notes rising by 14.3 basis points to 2.59%. With the Fed’s Hawkish efforts to bring inflation down, muni bonds have been hit hard this year with bonds maturing in 10-years have climbed by 147 basis points. Munis were able to outperform Treasuries last week even as munis yields rose for the week, as ratios for state and local debt maturing debt is now yielding 82.36% of Treasuries compared to 83.55% from the prior week. The yield curve did steepen for the week as the gap between short-term and long-term notes steepened by 27.7 basis points to 132 basis points as many investors continue to favor the short end. |

|

|

|

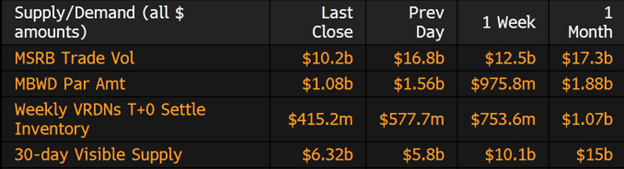

Investors offloaded about $2.1 billion from municipal-bond mutual funds last week according to Refinitiv Lipper US Fund Flows data, this follows the prior weeks inflow of $1.2 billion which snapped 15 straight weeks of outflows. Many investors decided to get ahead of the CPI data as well as the FOMC rate decision who are expected to raise rates by 50-basis points. However, a 75-basis point rate hike is still not off the table, especially since CPI came higher than expected (8.6%). |

|

With inflation hitting a 40-year high, tax-exempt munis yields have inched higher for the year causing a year-to-date loss of 7.83%. Although, tax-exempt bond returns are near record lows they are still fairing better than their taxable muni bond counterparts who have dropped roughly 14% year-to-date. Tax-exempts have also outperformed other fixed income markets as US Treasuries have lost roughly 9.26% for year, and US Corporates losing 13% for the year. With these volatile markets, investors should focus on relative value in the municipal markets. 30-year ratios for tax-exempt bonds are now averaging roughly 95% while taxable municipal bonds ratios stand at 109%. With only $28 billion of taxable issuance ($ 8 billion refunding) this year, taxable bonds should garner much more attention as they have cheapened to a point where buyers should dive back in. |

|

|

|

Municipal Supply: With the FOMC rate decision coming on Wednesday, many issuers are taking a pause on issuance. The negotiated calendar will only have an expected volume of just over $2.3 billion with only two issues being over $300 million. The County of Riverside will be issuing $360 million in Tax and Revenue Anticipation Notes and the City of Salt Lake City Public Utilities Water & Sewer Revenue plans on issuing $301 million. |

|