AmeriVet Weekly Muni Snapshot

|

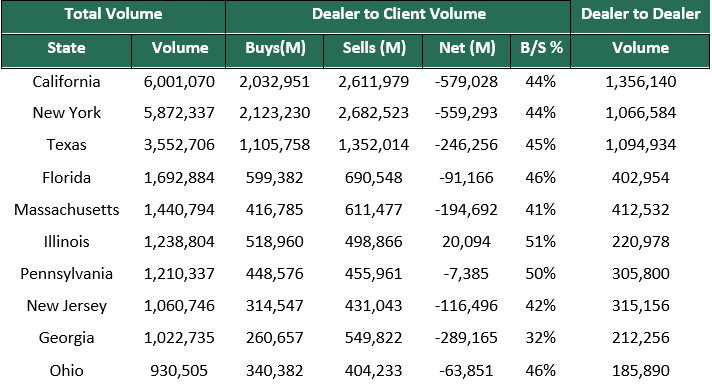

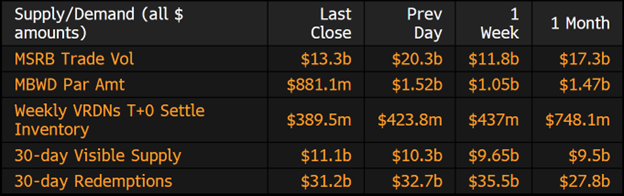

Municipal New Issuance: With a holiday shortened week, the negotiated calendar for the week totaled to just over $4 billion issued. Los Angeles Department of Water issued the largest deal of the week which totaled to $399 million. The New Hampshire Business Finance Authority issued $313 million in social bond Certificates through the National Finance Authority of New Hampshire. With yields continuing to rise, it has been a topic of discussion with many issuers as to whether to price their bonds now or wait to see if rates settle down. If they choose to continue sitting on the sidelines, they possibly miss out on pricing at a lower yield if rates rise even more. Municipal Secondary Trading: Secondary trading for the week totaled to just about $37.6 billion. The reason for the low volume was the Juneteenth holiday on Monday and the markets were closed. We continue to see volatile markets as clients are selling as investors are pulling money out of funds in record numbers. Clients bids-wanted totaled to just around $5.2 billion for the week with three of the days having over a billion in bids-wanted according to Bloomberg. |

|

|

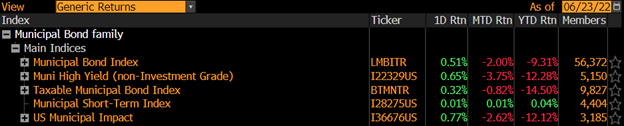

Municipal Spread: After having three weeks of rising yields, munis were able to show some positive news with yields on 10-year notes falling by 10.4 basis points to 2.80% for the week. This equates to a 0.8% gain, the second-best week of performance of the year. Yields have been steadily climbing this year as inflation has climbed to its 40- year high as well as the mounting fears of a recession has sent investors to the sidelines. With the rally in munis last week, munis were able to outperform Treasuries as 10-year ratios is now yielding 89.56% compared to the prior week where those same ratios were at 90.15%. Just a month ago, the 10-year ratio was 101.34%. The muni curve did flatten slightly last week with the gap between short-term and long-term securities flattened by 3.6 basis points to 133 basis points. Although we had a small rally, we should still should understand the fact that we are still not at the bottom but we are almost there. With mounting concerns of a recession and the rally in Treasuries in the last two weeks, we could see munis follow suit as investors are starting to see buying opportunities. |

|

|

Investors continue to pull funds out of municipal bond mutual funds, with investors pulling about $1.6 billion out of those funds last week, this follows the prior weeks outflow of $5.6 billion, and the 18th outflow of the past 19 weeks. One bright spot this year in the muni market has been muni ETF’s due to their short-term exposure. They have been able to reduce investors exposure during periods of uncertainty. But as it stands, muni ETF’s are on pace to have a monthly outflow which will be the first since January. So far this month, muni ETF’s have seen roughly $1.7 billion of outflows, the largest since March 2020. With the Fed being more aggressive with rate increases to combat inflation, its going to be difficult to find a safe haven to park their money. |

|

As we head into the end of the month and reach the halfway mark of 2022, munis, just like every other fixed income product, has struggled. The Bloomberg index (LMBITR) is down about 2% for the month and down roughly 9.3% year-to-date. With yields on 10-year notes rising by 35 basis points this month, mainly due to inflation coming in at its highest in 40 years, the word recession has been creeping back into everyone’s minds as the Fed has been forced to combat inflation with aggressive rate hikes. |

|

|

Municipal Supply: We will finally get some good news on the supply front as the negotiated calendar will have an expected volume of $6.7 billion, with two issues being over $700 million. The largest deal for the week will be the $950 million New York City Transitional Finance Authority deal in which AmeriVet will be a Selling-Group-Member. The second largest deal of the week will be $725 million Alabama Corrections Institution Finance Authority Revenue Bonds issuance. |

|