AmeriVet Weekly Muni Snapshot

|

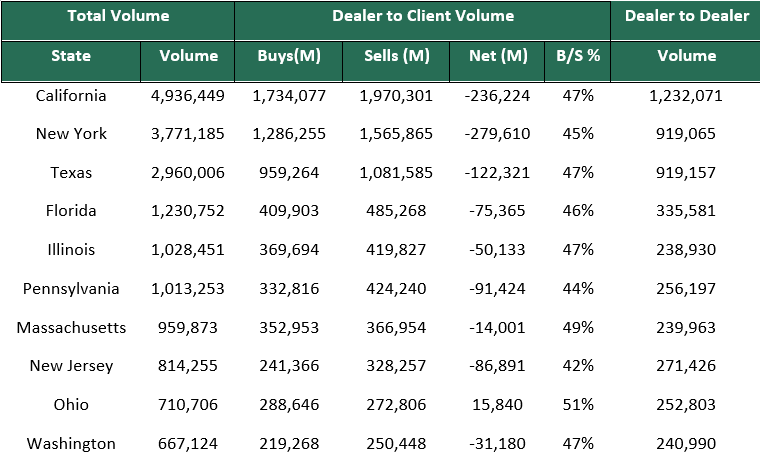

Municipal New Issuance: With the July 4th holiday on Monday, the negotiated calendar only totaled to just over $3.6 billion for the week with three issues covering over half of the issuance. The largest deal of the week was the $1.6 billion Denver City Airport Systems Revenue bonds which were AMT bonds. The second largest deal of the week was the $700 million Triborough Bridge and Tunnel MTA deal which AmeriVet was a Selling-Group-Member. This deal was unique because the bonds were backed by New York City’s sales tax receipts rather than fare and toll receipts. This gave the deal a higher credit rating which gave it more interest from investors. This is the second time the MTA has used a separate revenue source outside of farebox and toll collection. Municipal Secondary Trading: Trading for the week totaled to just over $28.5 billion for the week as the markets were closed on Monday due to the July 4th holiday on Monday. With the CPI number coming on Wednesday, we should expect to see a very active secondary market as investors try to gauge if inflation has been brought under control. According to Blomberg client bids-wanted were down for the week totaling to about $3.7 billion with only one day having bids-wanted to over $1 billion. |

|

|

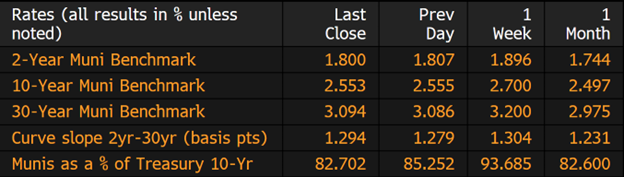

Municipal Spread: For the third straight week muni yields fell, showing signs that we may start to see a recovery and some positive sentiment towards tax-exempt bonds. Yields on 10-year notes fell this past week by 15 basis points to 2.55%. With $45 billion in redemptions coming this month and a small 30-day visible supply we could see a very active secondary market as investors need to put money to work. Munis continue to outperform Treasuries as ratios on 10-year notes fell to 82.70% this past week. Ratios have slowly turned to favor munis since their highs back in mid-April when they hit a high of 104.45% which was also when we saw yields at its highest for the year when they were at 2.97%. With yields falling again, we did see the muni curve flatten slightly by just 1 basis point to 129 basis points. |

|

|

For the first time in many weeks, we saw an outflow that was below $1 billion. According to Refinitiv Lipper US Fund Flows data, investors pulled about $313 million from municipal bond mutual funds. This is the first time we did not see an outflow of over $1 billion since the first week of June when we saw an inflow of $1.2 billion. This outflow marks the 5th straight week of outflows and 20th out of the last 21 weeks of outflows. The only inflow we saw during this time was the first week in June which was $1.2 billion when we saw the short muni market rally. |

|

The start of the second half of the year has become somewhat favorable to munis as we have started to see retail investors start to dive back into the markets with yields at attractive levels. Yields have fallen an average of about 35 basis points in the last three weeks alone with 14 basis points in the past week alone. This is positive news as investors and issuers want stability in the muni markets. So far, for the month of July, munis have returned about 1.2% but still have a loss of about 8% this year. As long as June’s CPI number comes within expectations, which comes out on July 13th and the Fed pulls back on a 75 basis point rate hike we could see a better outlook in munis and post a gain for the second half. |

|

|

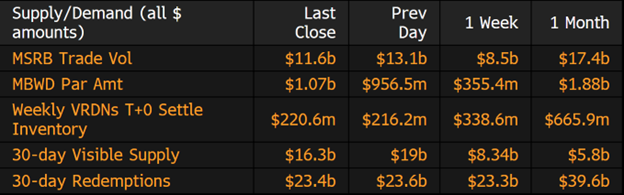

Municipal Supply: With the July 4th holiday behind us, we will see the calendar pick up slightly with an expected negotiated calendar to be at $5.3 billion. The largest deal of the week will be the $1 billion Colorado Health Facilities Authority Intermountain Healthcare issue. Dallas Fort Worth International Airport will be issuing $542 million in refunding bonds. AmeriVet will be in one issue this week as a Co-Manager which will be the $64 Maryland Stadium CABS issuance. With only $19 billion in next 30-days coupled with $45 billion coming back to investors as well as yields falling, we should start to see issuers comeback to the market. |

|