AmeriVet Weekly Muni Snapshot

|

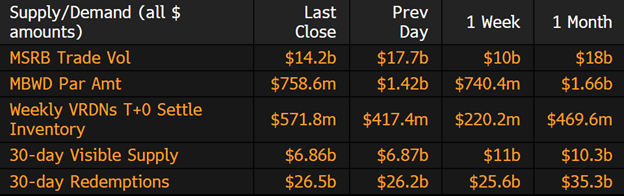

Municipal New Issuance: Last week’s negotiated calendar totaled to just under $5 billion for the week as many issuers decided to issue ahead of the much anticipated 75 basis point rate hike by the Fed. The largest deal of the week was the $709 million Main Street Natural Gas, Inc. (GA) issuance as Supply Revenue bonds. AmeriVet was in 2 deals this week as a Selling-Group-Member which were the $492 million New York City Transitional Finance Authority and the $152 New York City Housing Development Corp issuances. The New York City TFA was downsized slightly by about $15 million. The New York HDC deal was downsized as well as demand on the short end of the issue had faded. Municipal Secondary Trading: Trading for the week totaled to roughly $40.8 billion, with 51% of all trades being dealers buying as investors prepare for a 75-basis point rate hike later this week. Client’s bids-wanted continues to be high according to Bloomberg as clients put up $6.25 billion up for the bid with 4 days having over $1 billion in bids-wanted. |

|

|

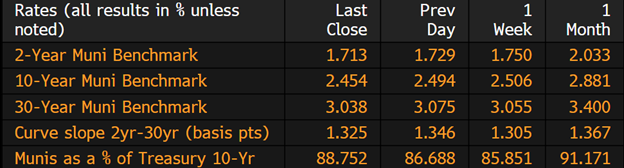

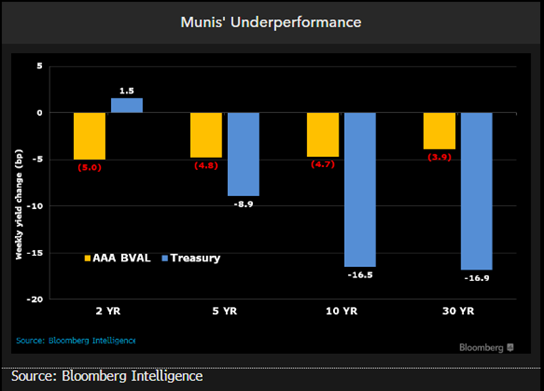

Municipal Spread: For the fifth straight week muni yields have fallen with 10-year notes falling by 5.2 basis points in the past week to 2.45%. With the drop in yields, munis underperformed Treasuries for the week as State and Local debt maturing in 10-years is now yielding 88.75% of Treasuries, compared to 85.85% a week ago. The gap between short-term notes and long-term notes steepened by .2 basis points to 132 basis points this past week. The muni curve continues to steepen as investors are favoring the short end of the curve as the 2-year ratio is now yielding 57.42% while 30-year ratio is yielding 101.81%. |

|

|

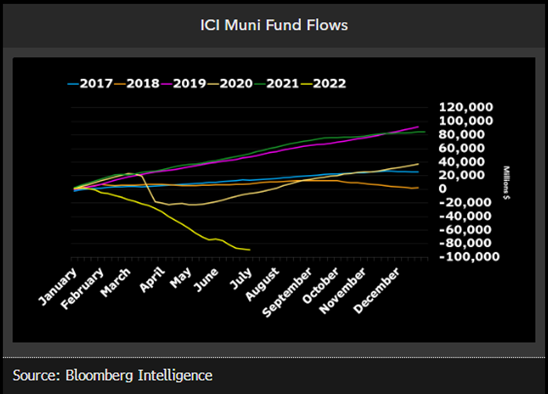

According to Refinitiv Lipper US Fund Flows Data, Investors were quick to pull about $699 million from municipal-bond mutual funds erasing the inflow of $206 million we saw in the prior week. This marks 21 weeks of outflows since February. Investors have pulled about $89 billion from muni funds with only three weeks of inflows. This year’s outflows have erased all of 2021 inflows which totaled to $84 billion. |

|

|

The front end of the muni curve has performed the best so far in 2022, as inflation soars and a possible recession looming, investors have been favoring the short end which has pushed ratios to 55% of Treasuries. Just over 2 months ago, those same ratios were at 90%. While the long end of the ratio today is at 101.8% of Treasuries, 2 months ago it was at 110.70%. With Treasuries rising, munis have diverged from the notion of lagging Treasuries as they have held their own and have pushed ratios to the richest levels on the short end while pushing ratios in the belly and long end to cheaper levels for 2022. |

|

|

Municipal Supply: With the Fed rate decision coming this week, issuers are sitting on the sidelines as they digest the rate hike. The negotiated calendar will be the smallest issuance of the year with just over $2.8 billion scheduled. The largest deal of the week, being the Port of Seattle, which plans on selling $877 million with $595 million being AMT bonds. The next largest deal will the Belton Independent School District which is scheduled to sell $168.8 million. |

|