AmeriVet Weekly Muni Snapshot

|

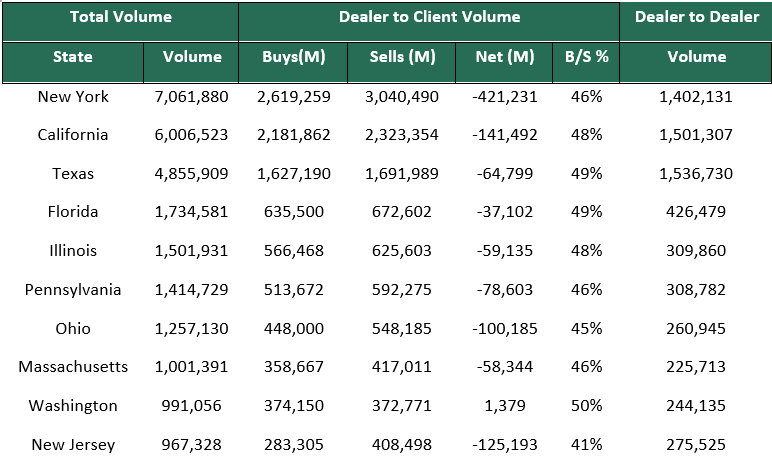

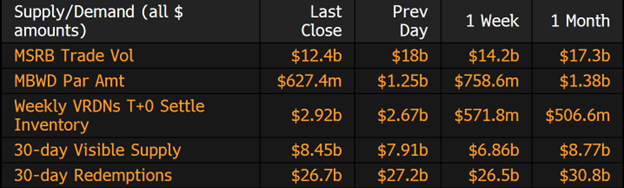

Municipal New Issuance: With the Fed’s rate decision last week, many issuers decided to take a step back and wait to issue until after the Fed spoke. The negotiated calendar for the week totaled to just over $1.5 billion as a few issuers who were scheduled to sell, postponed issuance for a week. The largest deals of the week were Belton ISD which issued $166 million, followed by the Hayes Unified School District which issued $143 million. Municipal Secondary Trading: Secondary trading for the week totaled to roughly $41.9 billion as clients reacted to the Fed raising rates by 75 basis-points by purchasing bonds last week. Roughly 53% of all secondary traders are clients purchasing bonds. One of the reasons for this is due to the lack of supply as many issuers chose to wait until the Fed announced their rate hike. Client’s bids-wanted for the week was below average to what we have been accustomed to seeing in 2022, with clients just putting up $4.84 billion for the week with just two days of bids-wanted of over $1 billion. |

|

|

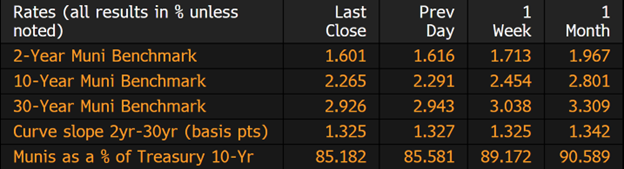

Municipal Spread: For the seventh straight week, we have seen yields fall once again as yields on 10-year notes saw one of its biggest rallies of the year with yields falling by 19 basis points to 2.24% for the week. With muni yields falling for the week, they were able to outperform Treasuries for the week as 10-year ratios are now yielding 85.18% compared to 89.17% from the prior week. Although we did see yields drop this past week, the yield curve still remains the same at 132 basis points. |

|

|

According to Refinitiv Lipper US Fund Flows data, investors added about $236 million to municipal-bond mutual funds last week. This follows the prior weeks outflow of $699 million and marks just the fourth time since February that we have had an inflow. With a potential recession looming, we could start to see more inflows into municipal bond funds. |

|

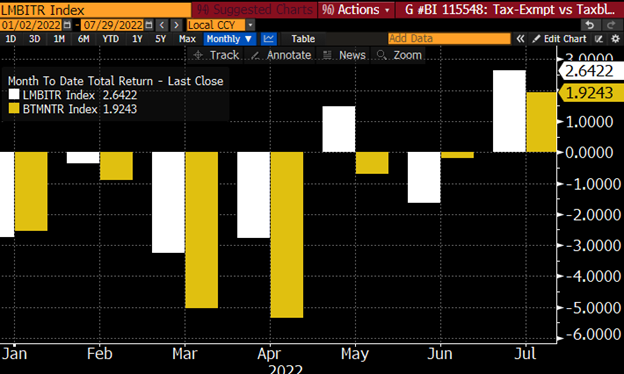

July has been very favorable for munis as munis have returned roughly 2.64% according to Bloomberg index data (LMBITR) for the month, making it the best month-to-month returns of the year and only the second positive monthly return, besting May’s return of just 1.5%. All across the muni curve, we saw positive returns this month with the long end having the best returns of 3.77%. Taxable munis also showed some positive gains by returning about 1.92% for the month. Munis bested US Treasuries as they returned just 1.59% while US IG corporates had the best returns for the month returning 3.24%. Although July was a good month, we still need to be weary of markets as July was a heavy redemption month and investors still need to put money to work. We still need to keep an on the markets as the next couple of months is a true test to see if the Fed’s recent rate hikes were able to tame inflation or if they need to be more aggressive in rate hikes which could push the economy into a deeper recession. |

|

|

|

Municipal Supply: With the Fed decision finally behind us, the negotiated calendar will pick up slightly this week with just $3.5 billion scheduled. The largest deal of the week will be the $877 million Port of Seattle deal, which will $806 million in tax-exempt bonds and $70 million in taxable refunding bonds. Christus Health Obligated Group will be bringing $323 million to the market this week. |

|