AmeriVet Weekly Muni Snapshot

|

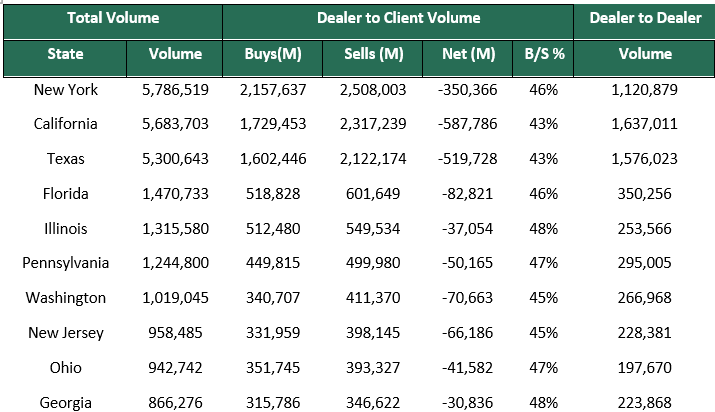

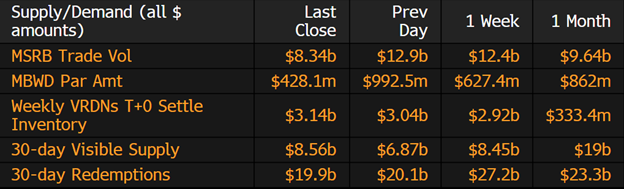

Municipal New Issuance: The negotiated calendar picked up slightly last week with issuers issuing roughly $4.4 billion with two issuers issuing over $700 million. The largest issuer of the week was the Port of Seattle who issued $791 million, which had $585 million in AMT bonds, and $206 million in tax-exempt bonds. The next largest deal of the week was the $755 million Georgia Port Authority Revenue issue. Municipal Secondary Trading: August is off to a slow start as secondary trading for the week totaled to $37.7 billion, with the unexpected higher jobs number we did see some unexpected volatility in the markets on Friday which caused munis to sell off mainly in the front end of the curve. According to Bloomberg, we are starting to see smaller amounts of customer bids-wanted as investors are starting to add to muni funds instead of selling. Last week, clients put around $5.16 billion up for bid and there were only two days of bids-wanted for over $1 billion. |

|

|

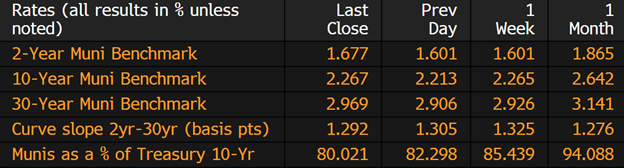

Municipal Spread: It looked like August was starting to look just like July as yields fell for the first four days of the week but with the higher-than-expected jobs number on Friday, we did see yields rise considerably on Friday but munis remained unchanged for the week. With yields remaining unchanged, munis did outperform Treasuries as muni buyers are continuing to favor munis as 10-year ratios is now at 80.02% compared to 85.44% from the prior week We did see the curve flatten slightly by 3.3 basis points to 129 basis points as the relative cheapness on the long end of the curve has brought back buyers as the short end continues to be rich compared to the rest of the curve. |

|

|

For the second straight week, municipal bond mutual funds saw investors add to their funds as the markets continue to be favorable to tax-exempts markets. Investors added last week about $1.1 billion to those funds following the prior week’s inflow of $236 million and making just the fifth weekly inflow since February. This is only the second time this year where inflows topped $1 billion, the other time was back in June where we saw $1.2 billion of inflows. |

|

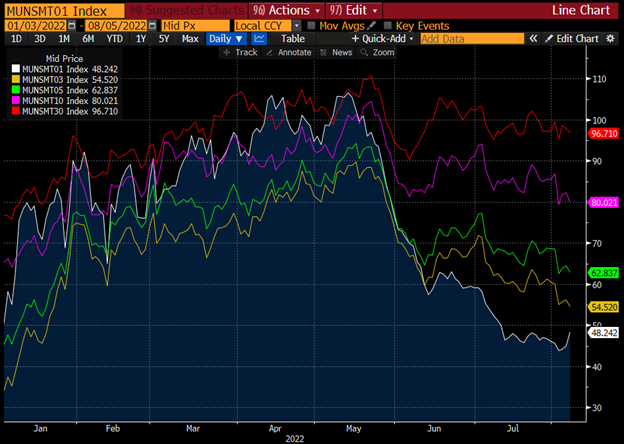

With muni yields continuing to fall, the one area of the curve that has become increasingly expensive relative to Treasuries has been the bonds maturing within 5 years and in. Currently, muni bonds maturing in 1 year are now yielding 48.24% of Treasuries, while bonds maturing a year later are yielding 51.64% of Treasuries, and bonds maturing in 5 years are yielding 62.83%. Once you go further out in the curve, these ratios are more favorable to investors with ratios on 10-year notes at 80.02%, and ratios for 30-year notes at 96.7%. This has caused many to look further down the curve towards the 7-to-10-year part of the curve. In the past two weeks, muni bonds maturing 5 years and in have had ratios dropped by only 7.7 percentage points. However, when you look at the 7- range, ratios have dropped an average of 7.8 percentage points, while bonds maturing 10-years dropped by 9.1 percentage points. With ratios falling this much in the 10-year range, this shows that the investors are willing to go a little further out on the curve if the relative value is there. |

|

|

Municipal Supply: The negotiated calendar will pick up again with an expected volume of around $4.9 billion as yields are starting to look attractive for some issuers to come back to the markets. The largest deals of the week will be the City of Los Angeles Department of Airports, which plans of selling $990 million in refunding bonds, followed by the Triborough Bridge and Tunnel Authority which plans on selling $400 million for the MTA Bridges and Tunnels. AmeriVet will be in one deal this week as a Co-Manager which will be the $307 million City of Philadelphia Water and Wastewater Revenue bonds. |

|