AmeriVet Weekly Muni Snapshot

|

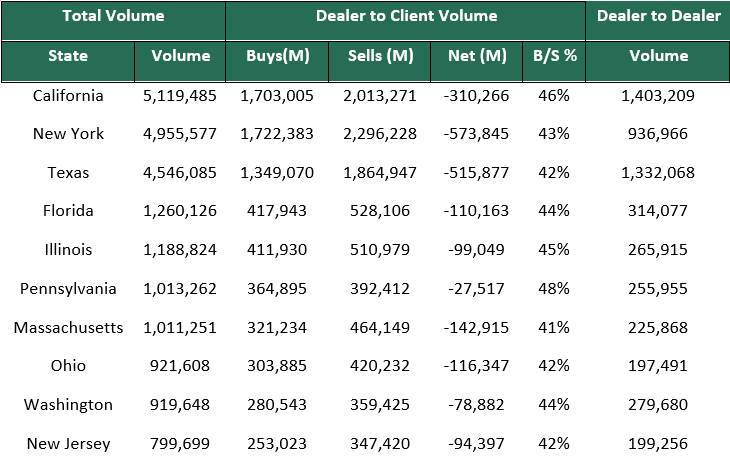

Municipal New Issuance: The negotiated calendar last week totaled to around $5.5 billion with the largest deal being the $1.1 billion Los Angeles Department of Airport issuance. The second largest deal of the week, which AmeriVet was in the Selling Group, was the $400 million Triborough Bridge and Tunnel. AmeriVet also participated as a Co-Manager in one other deal for the week which was the $294 million Philadelphia Water and Wastewater Revenue issue. Municipal Secondary Trading: August continues to be off to a slow start as secondary trading for the week totaled to $33.95 billion, with 56% of all secondary trades being clients buying from dealers. According to Bloomberg, clients bids-wanted was up slightly for the week as clients put up roughly $5.22 billion for the week compared to $5.16 billion from the prior week. |

|

|

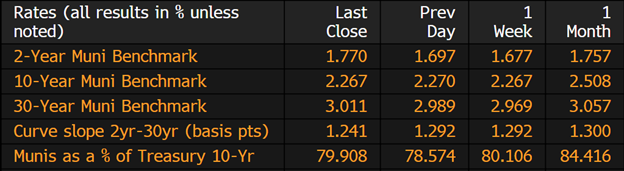

Municipal Spread: The second week of August saw yields remain unchanged with yields on 10-year notes remaining at 2.26% for the week. Although munis have been unchanged for the week, they continue to outperform Treasuries with the 10-year portion of the curve yielding 79.91% compared to the prior week when the ratios were at 80.10%. The 10-year portion of the curve also performed the best compared to the rest of the curve which only out performed treasuries slightly. We did see the muni curve flatten for the week to 124 basis points, as the short end rose while the long end remained relatively unchanged. |

|

|

After two straight weeks of inflows, investors pulled about $635 million from municipal bond mutual funds last week according to Refinitiv Lipper US Fund Flows Data. This follows the prior weeks inflow of $1.1 billion and is the 22nd outflow since February. |

|

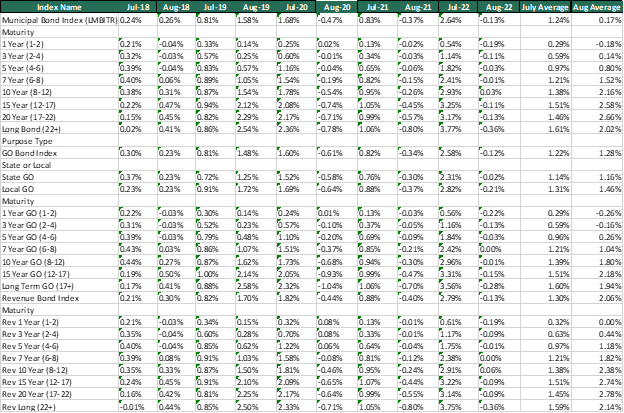

After having a fiery start for the summer with returns of 2.64% (LMBITR) in July, August has yet to come out of the starting gates with munis falling by just .13% for the first 2 weeks of the month. This shouldn’t be too much of a cause of concern as August is generally a slow month for Munis, as much of the buying was from redemptions in July. In the past, July has gained about 1.24%, while in the same period August has only returned just 0.17%. 10-year notes in the same time period for July have fallen on average of 17 basis points while for the same time period in August, have remained flat showing us that August has historically been a slow month for munis. |

|

|

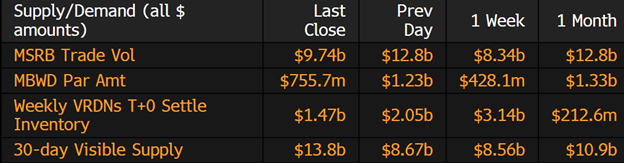

Municipal Supply: The negotiated supply for the week will be larger than usually expected for 2022 with an expected volume of just over $9 billion with three deals being over $1 billion and four deals total to $6.25 billion. This is a good sign to see larger issuers return to the markets as investors have been in need of supply. The largest deal of the week will be the Commonwealth of Massachusetts, which plans on selling $ 2.69 billion on taxable social bonds. The Oklahoma Development Finance Authority will be also issuing taxable bonds to the sum of $1.35 billion. The Regents of the University of California is planning on selling $1.25 billion which will consist of taxable and tax-exempt bonds. AmeriVet will be in two issues this week which will be the $950 million New York City General Obligation bonds and the $52 million Wisconsin Housing and Economic Development Authority. |

|