AmeriVet Weekly Muni Snapshot

|

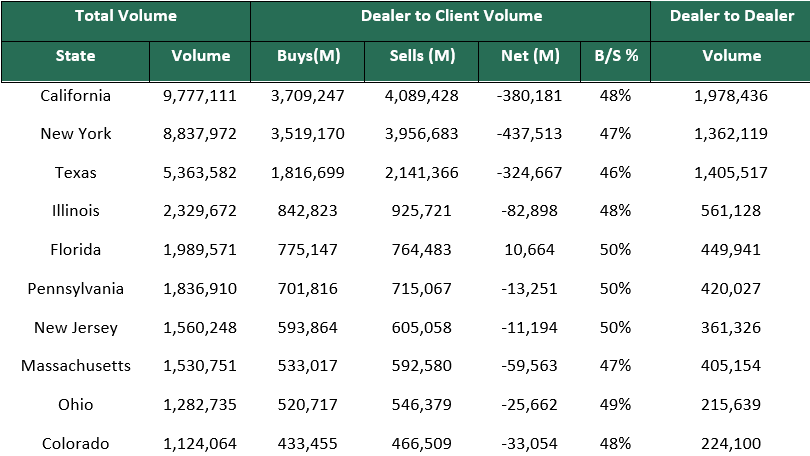

Municipal New Issuance: The negotiated calendar last week was very small with just over $3.7 billion as issuers continue to take a pause on issuance as rising interest rates are making it less attractive to borrow for new projects or the refinance existing debt. The largest deal of last week was the $961 million Texas Water Development Board issuance. The second largest deal of last week was the $258 million San Antonio Water System revenue bonds issuance. AmeriVet participated as a Selling-Group-Member for the $6.4 million Maryland Community Development Department of Housing and Community Development issuance. Municipal Secondary Trading: Secondary trading continues to be very volatile as rising interest rates have caused the markets to go into a frenzy. Secondary trading for the week totaled to roughly $53.5 billion with 52% of the trades being dealers selling to clients. Client’s bids-wanted was also high for the week with about $8.77 billion up from the prior week of $8.18 billion. Clients’ bids-wanted continues to be high as many investors continue to pull money out of mutual funds due to rising interest rates from the Fed’s policy of raising interest rates to combat high inflation. |

|

|

Municipal Spreads: Munis continue their slide last week as yields once again climbed to levels we have not seen in since 2011. Yields on 10-year notes rose over 15.5 basis points in the past week to 3.25%. The last time yields were this high on 10-year notes was back in April 2011. Although Treasuries yields rose sharply last week, munis rose even more as ratios on 10-year munis is now yielding 85.31% compared to 84.11% from the prior week. We continue to see the yield curve flatten as yields on the short end continue to follow the short end of Treasuries as a recession continues to loom over our shoulders. The yield curve flattened by 5.2 basis points this past week to 87 basis points. |

|

|

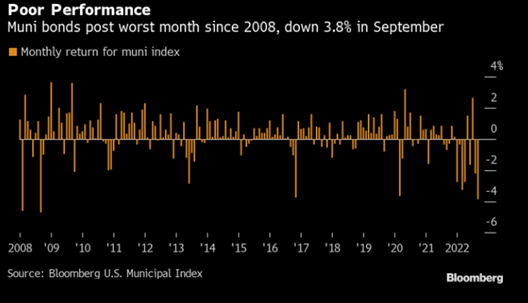

Outflows intensified once again as investors pulled about $3.6 billion out of municipal bond mutual funds last week versus $2 billion of outflows from the prior week according to Refinitiv Lipper US Fund Flows data and marks the 8th straight weeks of outflows. Muni ETFs saw outflows as well to the sum of $295 million after $8.99 million from the previous week. Muni funds continue to feel the pain as rising interest rates has many investors continuing to wait on the sidelines until the volatility subsids. We should outflows continue until we start to see the volatility in the markets to subside. September has been an excruciatingly painful month for municipal bonds as muni bonds have lost roughly 3.84% for the month and now have lost about 12.13% for the year as munis are still on pace to have their worst year of performance since the 1980s when records were kept. September was the worst performing month since September of 2008 as the continuation of an aggressive interest rate hikes by the Fed have battered fixed income markets. The area of the most concern now is the long end as losses have amounted to almost 20% while the short end has lost only 2.34%. Even though losses are greater as you go further out into the curve, investors should start to look further out into the curve as ratios are starting to turn in favor of munis. Ratios for 5-year to 10-year munis have risen over 6 percentage points in the past week while 2-year to 3-year munis have only risen by just 4 percentage points. |

|

|

Municipal Supply: The negotiated supply for the week continues to be very light with an expected volume of just $3.5 billion with one issuer taking up over a third of the supply. That deal will the $1.3 billion New York City General Obligation issuance which will include taxable and tax-exempt bonds. AmeriVet will be participating as a Selling-Group-Member. The next largest deal of the week will be the $500 million California Earthquake Authority revenue bonds. AmeriVet will be a Co-Senior Manager on the $166 million State of California Veterans General Obligations Bonds. For the month of September, muni supply has declined by about 40% to about $24 billion which is the lowest monthly volume of debt sales since November 2020. |

|

|