AmeriVet Weekly Muni Snapshot

|

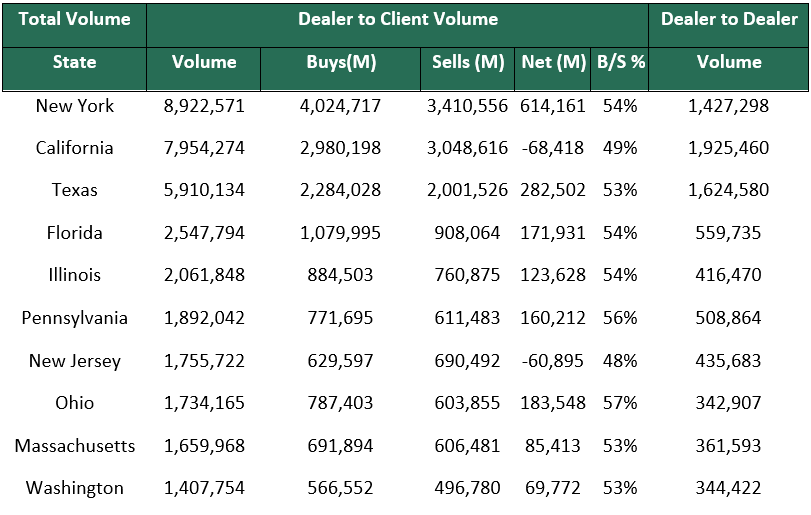

Municipal New Issuance: Last week’s negotiated calendar totaled to roughly $5.7 billion as this should be the last significant week of supply as many issuers will be done issuing for the year. The largest deals of the week were the $524 million City of Chicago followed by the $495 million New York City Housing Development Corporation which AmeriVet participated as a Selling-Group-Member. Los Angeles Department of Water and Power issued $399 million. AmeriVet was also in one other deal of the week as a Co-Manager which was the $72 million Massachusetts Housing Finance Agency. This was the first time Chicago issued since shedding its junk rating last month which saw overwhelming demand for their bonds. Municipal Secondary Trading: Secondary trading last week totaled to about $56.8 billion in trading. As we start to close out 2022, we should start to see secondary trading slow down as traders start to take off for the Holidays. According to Bloomberg, clients bids-wanted totaled to about $8.633 billion, slightly higher that the prior week’s total of $8.22 billion. |

|

|

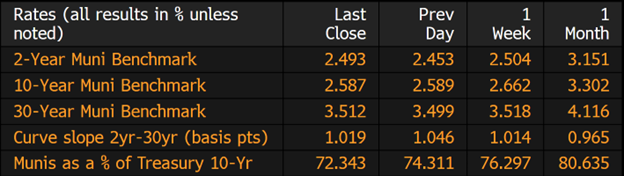

Municipal Spreads: Spreads fell for the week once again with 10-year notes falling by 7.5 basis points to 2.57% marking the sixth straight week of falling yields as we try to end the year on a high note after a year of record losses. With yields falling again, we did see munis outperform Treasuries again with 10-year ratios now yielding 72.34% compared to 76.29%. One month ago, those ratios were at 80.63% as this is sign that many investors are coming back to the muni market. Since the highs back on Oct 26th of this year, munis yields have fallen about an average of 75 basis points due to small supply and the Fed seeming to have gotten inflation under control which have brought yields down to which investor sentiment has improved. The muni curve did steepen last week by 3.4 basis points to 105 basis points. |

|

|

For the third time since August, we saw investors add to municipal-bond mutual funds as according to Refinitiv US Lipper US fund flows data, investors added roughly $47 million to those funds as this follows the prior week’s outflow of $1.4 billion. This is only the tenth weekly inflow we have had this year as investors have had a mass exodus out of fixed income funds due to higher yields as the Fed rose rates to combat record high inflation. Year to date investors have pulled roughly $124 billion from Municipal-bond mutual funds this year. |

|

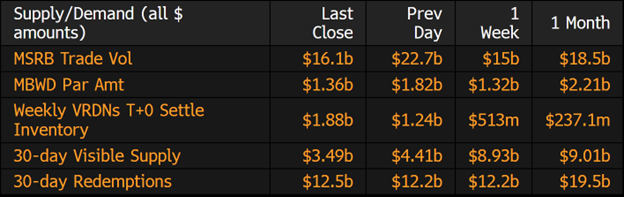

We have seen 10-year yields decline to 2.57% from its peak of 3.39% in mid-October, this decline in rates has been positive news for investors as munis had been down almost 13% for the year but have crawled back in recent weeks to be down by only 8%. The decline in rates in the last month and a half has been driven mainly by light supply with just $4.4 billion in the 30-day supply, as well as inflation being in check, and December being a strong month for cash reinvestment. |

|

|

Municipal Supply: Negotiated supply for the week will dwindle down to just $2.9 billion with one issue covering majority of the calendar which will be the $1.8 billion Pennsylvania Economic Development Finance Authority for the PennDOT Major Bridges Package One Project. The Idaho Housing and Finance Association will be issuing $253 million in Taxable bonds. |

|