AmeriVet Weekly Muni Snapshot

|

Municipal New Issuance: The negotiated calendar for the first week of January totaled to just over $1.1 billion with the bulk of the calendar being the $765 million Triborough Bridge and Tunnel issuance which AmeriVet participated as a Selling-Group-Member. With a light calendar, the Triborough deal took up the bulk of attention for the primary calendar as the deal was well over-subscribed with maturities being 2 to 3 times over-subscribed. Municipal Secondary Trading: Secondary trading for the week totaled to about $40.4 billion with about 55% of the trades being clients buying. According to Bloomberg, client’s bids-wanted totaled to about $4.72 billion for the week. This is the first time since March 2022 that we saw bids-wanted fall below $5 billion for the week. |

|

|

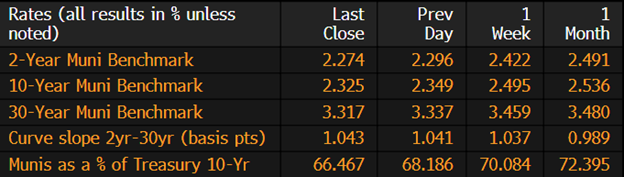

Municipal Spreads: Munis continue their rally as yields on 10-year notes fell by 17 basis points last week to 2.32%. Munis have fallen an average of 31 basis points across the curve in the first two weeks of the year. With yields falling last week, we did see the muni curve steepen by 6 basis points to 104 basis points. We continue to see munis outperform versus Treasuries as 10-year notes are now yielding 66.47% of Treasuries compared to the prior week when the ratios were at 70.08%. |

|

|

According to Refinitiv Lipper US Fund Flows data, investors added about $2 billion to municipal-bond funds last week. This follows the prior weeks outflow of $2.5 billion. This was the largest inflow to municipal funds in more than a year. This is a positive sign for munis as we had a record of outflows totaling to $144 billion back in 2022 due to yields rising from record inflation numbers and the Fed rate hike policy. |

|

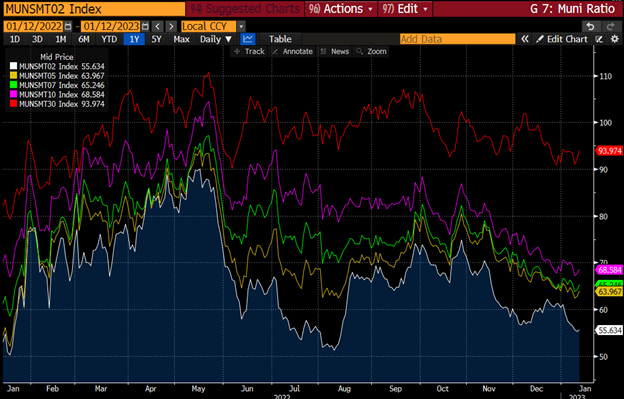

Demand for muni bonds has started to slowly make a comeback as muni funds saw $2 billion of inflows last week. This demand is a welcome sign to the tax-exempt sector as rising yields pushed investors to the sidelines. But with the CPI number coming in at 6.5% on Thursday, investors are slowly jumping back into the markets as yields are at attractive levels compared to the start of 2022. Yields should continue to fall as demand for munis will outpace supply in 2023 and coupled with concerns of inflation weaning, investor positive sentiment has continued to push munis further into positive territory with munis gaining about 2.1% so far this year. This has unfortunately pushed munis to become expensive relative to Treasuries with ratios at 12-month lows. This has caused many investors to move further out into the curve but this shouldn’t be too much of a concern as it is showing that investor concerns of a market downturn is abated. |

|

|

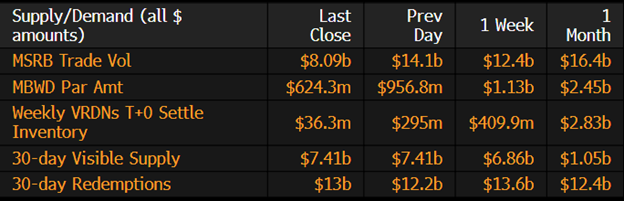

Municipal Supply: Supply will pick this week as the negotiated calendar will have an expected volume of about $8.1 billion. This will be the first significant sized calendar we’ve had since November of last year. The largest deals of the week will be the $887 million Brightline West Passenger Rail issuance followed by the $735 million Sales Tax Securitization Corporation that will consist of $430 million in taxable bonds and $305 million in tax-exempt bonds which AmeriVet will be in the Selling-Group. Also on the calendar will be $700 million Tennessee Energy Acquisition Corporation issuance which will include taxable and tax-exempt bonds. The Dallas Independent School District is planning to sell about $568 million in refunding bonds. |

|