AmeriVet Weekly Muni Snapshot

|

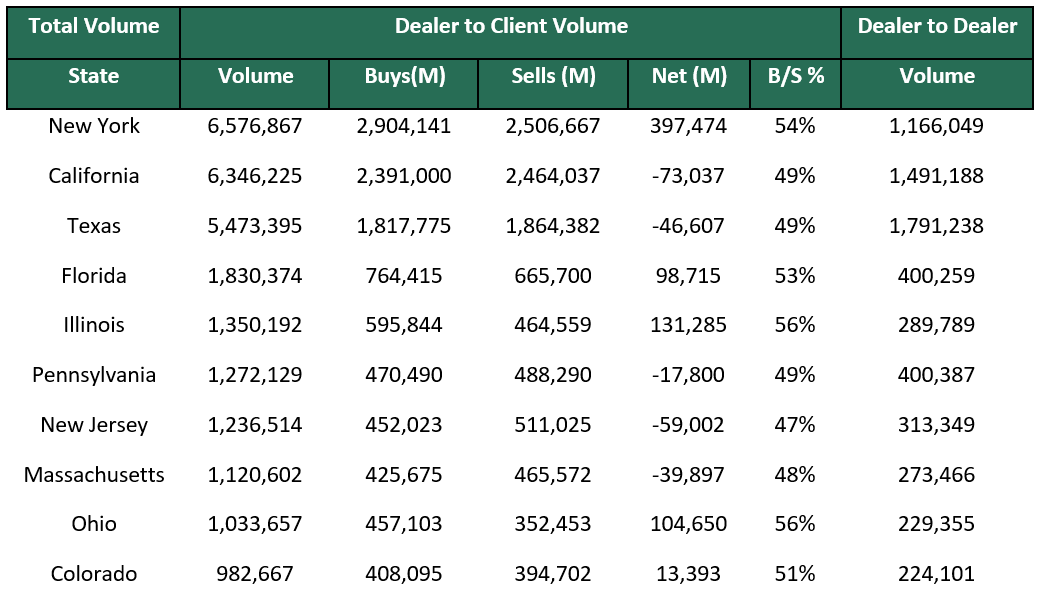

Municipal New Issuance: Last week’s negotiated calendar was very light due to the anticipation of the the FOMC rate decision and the employment numbers report as many issuers decided to sit on the side-lines for the week. Last week’s issuance totaled to just over $941 million for the week with the largest deal being the $274 million Fort Worth Independent School District issuance. Municipal Secondary Trading: Secondary trading for the week totaled to about $42.65 billion with majority of trading volume being on Thursday, the day after the Fed’s 25 basis point rate hike. Clients bids-wanted continues to be at elevated levels and according to Bloomberg, clients put up roughly $5.3 billion bonds up for the bid. Bids wanted have been up roughly 131.45% since the start of 2020. |

|

|

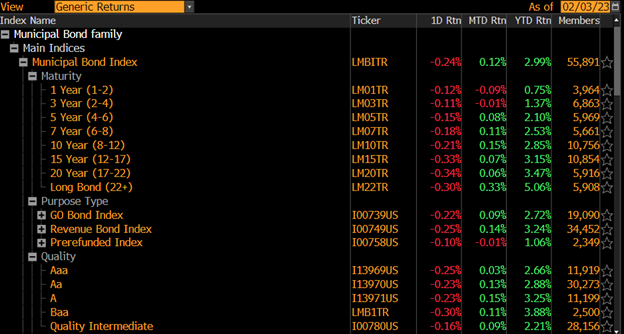

Municipal Spreads: Muni yields fell once again last week with 10-year notes falling by 1.7 basis points to 2.20%. We did see some bump in the curve as a result in the FOMC hiking rates by 25 basis points on Wednesday. However, with an unexpected high employment number, fixed income yields rose as a direct result of this. Yields have fallen an average of 37 basis points so far this year, a far cry from what we saw last year with yields rising to levels we have not seen in decades. With yields falling again last week, we did see ratios fall as Treasuries rose significantly after Friday as a result of the employment number and munis rose by only by an average of 5 basis points. Ratios for 10-year notes are now yielding 62.89% compared to the prior week of 63.79% and 70.54% a month earlier. We also saw the muni curve flatten slightly last week by 2.9 basis points to 108 basis points. |

|

|

After three straight weeks of inflows, last week investors pulled about $362 million from municipal bonds funds according to Refinitiv Lipper US Funds Flow data. This follows the prior weeks inflow of $1.3 billion. This is a unique situation as munis are a bit firmer and demand for tax-exempts are still present. |

|

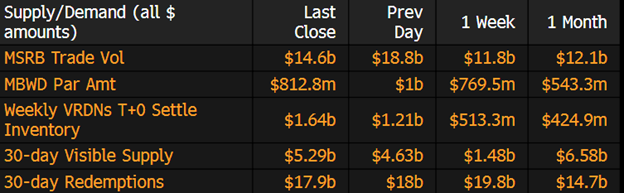

Munis continue to have a firmer tone going into the first few days of February even as the Federal Reserve hiked rates by 25 basis points. This firmer tone in the markets is based on investors acknowledging that the Feds hawkish tone is nearing its end as it appears that the Fed is still firmly committed to 25 basis points moves. Munis ended the month of January up 2.87% compared to a loss of 2.74% back in January of 2022 and have continued that rally going into February with munis being up 0.12% so far this month totaling to gains of 2.99% for the year. With January being one of the lowest new-issue supplies on record, we should continue to see this spill over into February as the 30-day supply is only $4.7 billion and 30-day redemptions are at $18 billion. We should expect to see yields fall even further as well and munis/Treasury ratios to become even richer as Treasuries have sold off after the unexpected strong Jobs number. |

|

|

Municipal Supply: The municipal calendar will pick up from the prior week of low supply, with the negotiated calendar totaling to about $3.6 billion with the largest deal being the $1 billion New York City Transitional Finance Authority which AmeriVet will be in the Selling-Group. The next largest deal of the week will the $648 million Lamer Consolidated Independent School District. AmeriVet will be a Co-Manager on the Massachusetts Housing Finance Agency issue which will issue $132 million in tax-exempt bonds and $22.9 million in taxable bonds. AmeriVet will also be in the $66.9 million Minnesota Housing Finance agency deal as a Selling-Group-Member. |

|