AmeriVet Weekly Muni Snapshot

|

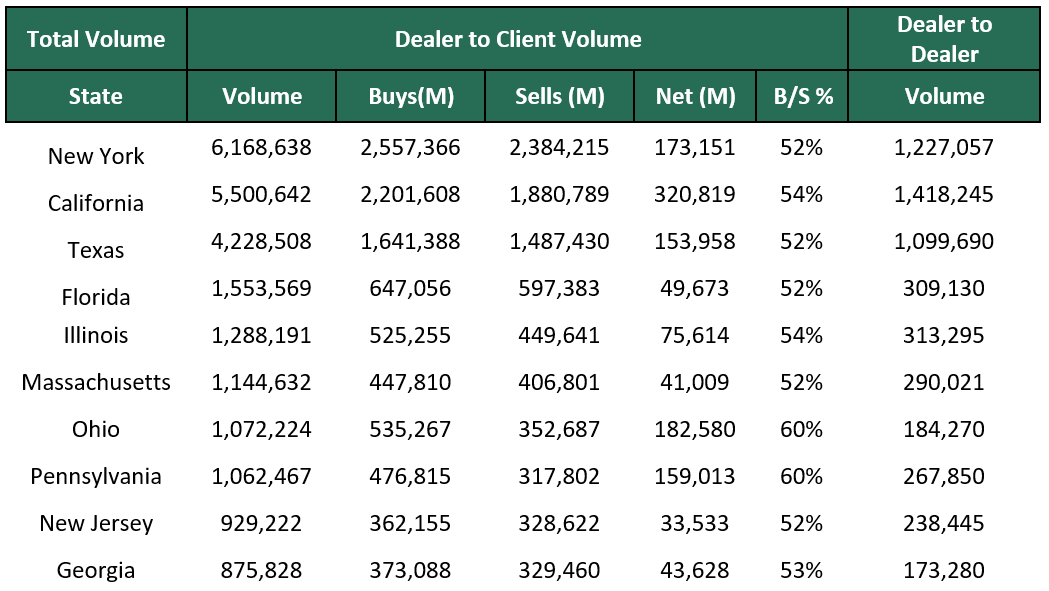

Municipal New Issuance: The negotiated calendar for last week tallied to about $5 billion for the week with two issuers issuing over $900 million in debt. AmeriVet was part of the two largest deals of the week as a Selling-Group-Member which were the $989 million State of Oregon deal which issued $804 million in tax-exempt bonds and $184 million in taxable bonds and as well as the $950 million New York City Transitional Finance Authority issuance. AmeriVet was also a Co-Manager on the $150 million State of New York Mortgage Agency issuance. Municipal Secondary Trading: Trading for the week totaled to roughly $37.6 billion for the week with about 53% of trades being clients sells. According to Bloomberg, we did see an uptick in bids-wanted last week with clients putting $5.1 billion up for the bid compared to $4.9 billion from the prior week. We are continuing to see larger than average bids-wanted as volatility continues to affect the markets. |

|

|

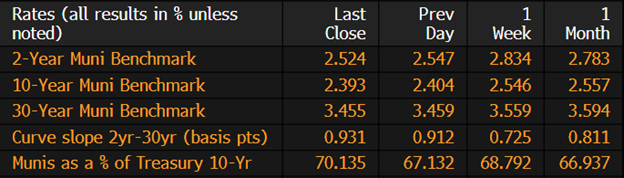

Municipal Spreads: Munis continue to hold up pretty well as the banking sector continues to face the fallout of Silicon Valley Bank (SVB) and Signature bank. Muni yields fell last week with yields on 10-year notes falling by 15.3 basis points to finish the week at 2.39%. Although muni yields fell for the week, they still underperformed Treasuries due to the large rally Treasuries had on Friday. The 10-year ratio is now yielding 70.13% compared to 68.79% from the prior week. With many buyers choosing to move to the front end of the curve, we did see the muni curve steepen this past week by 20.6 basis points to 93 basis points. |

|

|

Despite munis being firmer for the last couple of weeks, we continue to see investors pull money out of muni bond funds last week. According to Refinitiv Lipper US Fund Flows data, investors pulled about $461 million from muni bond funds. This follows the previous weeks outflow of $308 million. Investors have added roughly $1.77 billion to muni funds this year. |

|

With the banking sector having a tumultuous week, munis were largely ignored by investors as they moved towards higher quality investments such as Treasuries and munis. With the Fed expecting to raise rates by 25 basis points (rather than the 50 basis points many expected on Wednesday) and slow down their pace of rate hikes, munis have priced in this expectation. This past week we did see munis rally with the bulk of the bumps coming in the short end of the curve. The failures of Silicon Valley Bank (SVB), Signature bank, and other regional banks gave favorable conditions for munis to rally on this news as munis enjoyed the flight to quality. With this news, the front end saw yields drop by an average of 25 basis points while the long end dropped by an average of 11 basis points. With a potential recession still looming over our heads, investors are still moving towards the front end of the curve for credit quality and duration. With over half of the month over, munis have returned about 1.54% with the long end having the best returns of 2.19%. |

|

|

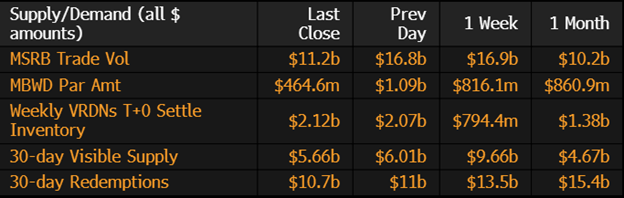

Municipal Supply: The negotiated calendar volume will drop significantly this week as many issuers are in a holding pattern as we wait to see how much the Fed will increase rates on Wednesday. The negotiated calendar is expected to be just over $3.7 billion for the week with the largest deal being the $1.49 billion Louisiana Utilities Restoration Corporation. The New York State Housing Finance Agency is scheduled to sell about $502 million in ESG bonds. |

|