AmeriVet Weekly Muni Snapshot

|

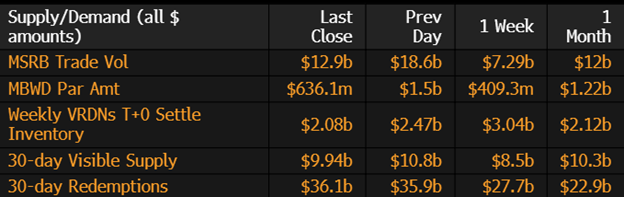

Municipal New Issuance: Although we had a shortened week for the Memorial Day holiday last Monday, the negotiated calendar totaled to about $5.2 billion with largest deal being the $1.4 billion New York City GO issue which AmeriVet was part of the Selling-Group. The next largest deal of the week was the State of Connecticut issue which sold $715 million in taxable and tax-exempt bonds which AmeriVet participated as a Co-Manager. AmeriVet was part of two other issues which were the $133 million New Jersey Housing and Mortgage Finance Agency as a Co-Manager and the $106 million South Carolina State Housing Finance and Development Authority issuance as a Selling-Group Member Municipal Secondary Trading: With only four days of the trading last week, secondary trading totaled to just over $33.25 billion for the week with 58% of the trading being dealer sells. Thursday had the largest volume of trading with $10.6 billion in secondary trading volume. According to Bloomberg, clients put up roughly $4.9 billion up for the bid with Thursday having the largest volume of bids-wanted with $1.5 billion in bids-wanted. |

|

|

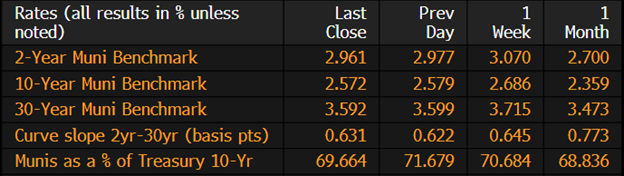

Municipal Spreads: After two straight weeks of rising yields, muni yields were firmer for the week as yields fell an average of 11.7 basis points for the week with 10-year notes falling by 11.4 basis points this past week to 2.57%. Munis were able to outperform Treasuries last week as the 10-year ratio is now yielding 69.66% of Treasuries, compared to 70.68% from the previous week. We did see the muni curve flatten this past week by 1.4 basis points to 63 basis points. |

|

|

According to Refinitiv Lipper US Fund Flows data, for the 16th straight week, muni bond funds saw investors pull money out of those funds, to the sum of $1.3 billion last week. This outflow follows the prior week’s outflow of $847 million. Year-to-date investors have added just $1.6 billion to muni bond funds. |

|

Munis ended the month of May with a firmer tone narrowly missing out on having one of the worst months of May in nearly two decades. Munis ended the month just down .87% and at its lowest peak, munis were down 1.38% for the month of May. As we enter the month of June, munis are currently up 1.96% for the year, which at this time last year, munis were down 7.3%. With June being a big period for reinvestment, we could see munis take a firmer tone but we still have to wait and see if the Fed will continue to raise rates once again. With NFP coming in higher than expected, we could see one more hike in the next 2 meetings. |

|

|

Municipal Supply: For the first week of June, the negotiated calendar will have an expected volume roughly $7.5 billion with the largest deals being the $900 million California Community Choice Financing Authority for their Clean Energy Project Revenue Bonds. The County of Los Angeles will be issuing a note deal to the size of $700 million. In addition, AmeriVet will be participating on the New York City Housing Development Corporation issuance of $641 million as a Selling-Group-Member. |

|