AmeriVet Weekly Muni Snapshot

|

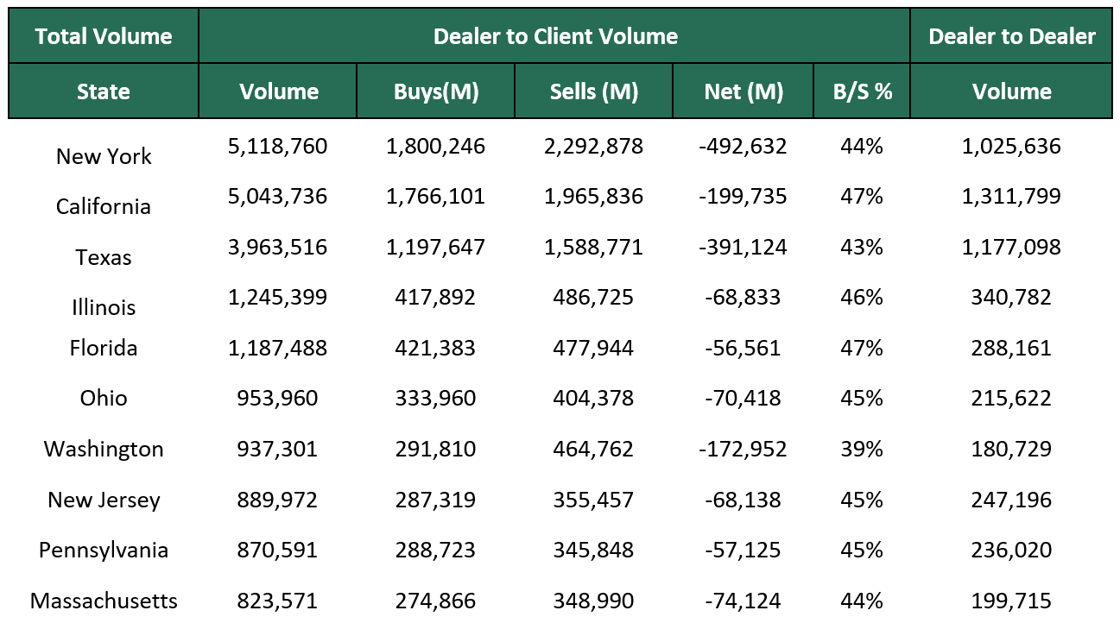

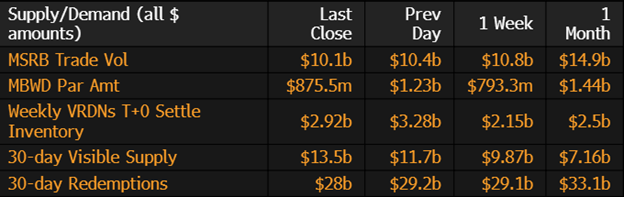

Municipal New Issuance: Last week’s negotiated calendar was low due to the Fed’s rate decision which influenced many issuers to take a pause in issuing for the week. The negotiated calendar last week totaled to roughly $3.4 billion with three deals taking up a third of the issuance. The largest deals of the week were the $581 million Black Belt Energy Gas District issuance, the National Finance Authority of New Hampshire which issued $540 million, and the third largest deal was $364 million Medina Valley Independent School District issue. Municipal Secondary Trading: Trading for the week totaled to just under $33.22 billion with 56% of trades being dealer sells.The majority of the trading was done on Tuesday and Thursday with light trading activity on Wednesday as traders waited for the Fed to announce their 25-basis point rate hike. According to Bloomberg, clients put up about $5.55 billion up for the bid, slightly up from the previous week total of $5.44 billion. |

|

|

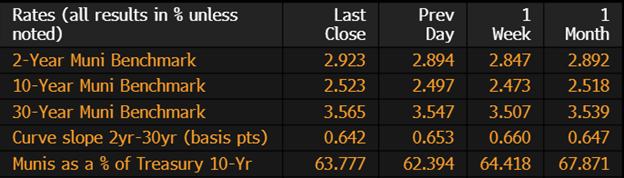

Municipal Spreads: Munis were weaker this week due to the stronger-than-expected economic data with yields on 10-year notes rising by 5-basis points to end the week at 2.52%. The long end saw some significant cuts with yields rising by 5.8 basis points this past week. With the sell off in Treasuries, munis were still able to outperform Treasuries with 10-year munis now yielding 63.77% of Treasuries compared to the prior week when the ratio was at 64.41%. We did see the muni curve flatten slightly by 1.8 basis points to 64 basis points. |

|

|

For the second week in a row, municipal bond mutual funds saw inflows. According to Refinitiv Lipper US Funds Flow data, investors added $552 million to those funds. This follows the previous weeks inflow of $1 billion. With the economic outlook looking favorable for munis, we should continue to see investors put money back into muni funds. |

|

As we close out the month of July, munis have had a strong showing to start of the summer with June and July showing positive gains pushing year-to-date returns of 3.25% with July returning so far .56%. The long end of the muni curve has seen the largest gains this month returning about .61% while the front end has seen modest gains of just .25%. With the front end continuing to be extremely expensive, investors are looking further out in the curve as 10-year munis continue to yield well below historical averages which are around 83%. With the summer being a time where new bond sales are light, valuations should continue to stay expensive in the short end. |

|

|

Municipal Supply: The negotiated calendar for this week will be rather large with an expected volume of $9.3 billion with the largest deals of the week being the $1.6 billion Dormitory Authority of the State of New York issuance and Long Island Power Authority is expected to sell $579 million. Crowley Independent School District is planning on selling $425 million. |

|