AmeriVet Weekly Muni Snapshot

|

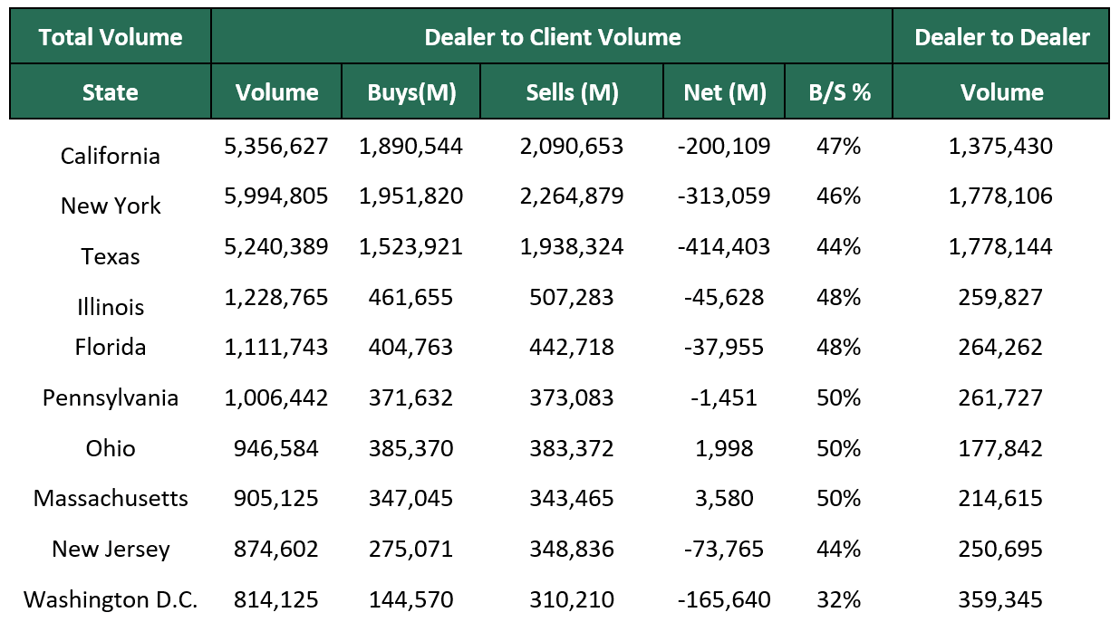

Municipal New Issuance: Last week’s negotiated calendar totaled to $8.3 billion with the largest deal being the $950 New York City General Obligation issuance which AmeriVet was part of the Selling-Group. The second largest deal of the week was the $902 million California Community Choice Finance Authority Green Bonds issue. AmeriVet was part of one other issue for the week as a Selling-Group Member which was the $370 million Triborough Bridge and Tunnel issuance. The majority of the new issues for the week saw significant interest as some of the issues saw their bonds bump by a few basis points. Municipal Secondary Trading: Trading for the week totaled to just under $35.62 billion with 54% of trades being dealer sells. The majority of the trading was done on Wednesday and Thursday and according to Bloomberg clients put up roughly $5.01 billion last week compared to $5.19 billion from the prior week. |

|

|

Municipal Spreads: Muni yields fell for the first time in two weeks where we saw yield rise by 28 basis points. This past week 10-year munis fell by 4.9 basis points to end the week at 2.70%. With munis yields falling this past week, they were able to outperform out Treasuries as the 10-year is now yielding 64.95% of Treasuries compared to the prior week when the ratio was at 68.09%. We did see muni curve steepen slightly by 0.2 basis points to end the week at 65 basis points. |

|

|

According to Refinitiv Lipper US Fund Flows data, investors added about $278 million to municipal bond funds, this gain follows the prior weeks outflow of $990 million. With the CPI number coming in the range of expectation and most seeing a pause in rate hikes next month, we should see more inflows into muni funds. |

|

The second week of August showed much improvement from the first week as we saw month-to-date returns go from -1.25% to -.83% with a year-to-date return of 2.22%. This modest gain is positive for munis as we saw munis follow suite with Treasuries with higher yields after their downgrade from Fitch a week and a half ago. With the CPI coming in mostly in-line with expectations and Treasuries rising as a result of muni ratios falling with front-end ratios currently averaging about 64%. |

|

|

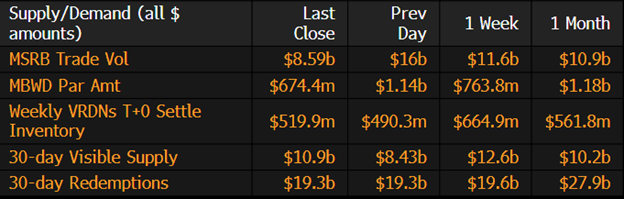

Municipal Supply: The negotiated calendar for this week will have an expected volume of just over $5.58 billion. The largest deal of the week will be the $933.8 million Dallas Fort Worth International Airport issuance which will consist of refunding bonds. The second largest deal of the week will be the $728.2 million Regents of the University of California issue. The Dormitory Authority of the State of New York plans on selling $300 million and with the 30-day visible supply at just $8.43 billion, we should expect to see significant interest in new bonds this week. |

|