AmeriVet Weekly Muni Snapshot

|

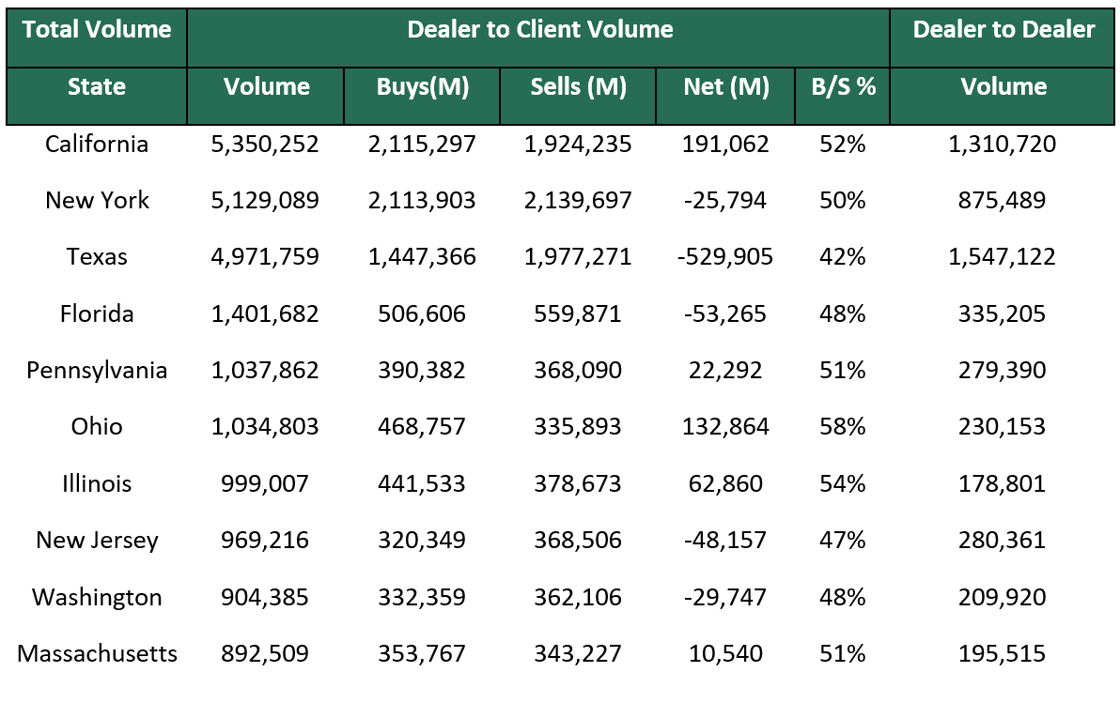

Municipal New Issuance: Last week’s negotiated calendar totaled to $5.8 billion with the largest deals of the week being the $932 million Dallas Fort Worth International Airport deal followed by the $701 million University of California Regents issuance. The Los Angeles Unified School District issued $384 million in sustainability bonds as well. Municipal Secondary Trading: Trading for the week totaled to just under $35.94 billion with 51% of trades being dealer sells. According to Bloomberg, clients put up roughly $6.15 billion last week compared to $5.01 billion from the prior week. This was the first time since the second week of April that we have seen over a billion of bids-wanted each day. |

|

|

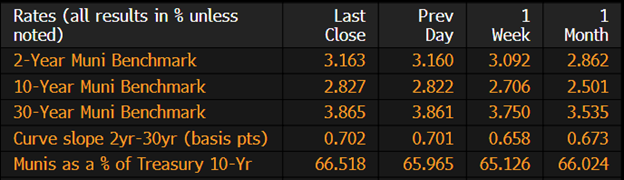

Municipal Spreads: Muni yields rose last week with 10-year notes rising by 12.1 basis points to finish the week at 2.82%. With munis yields rising this past week, munis did underperform slightly compared to Treasuries as 10-year notes are now yielding 66.51% of Treasuries compared to the prior week when the ratio was at 65.12%. The muni curve did steepen this past week by 4.4 basis points to 70 basis points. |

|

|

With munis weaker this week, we did see outflows from muni bond funds return as investors pulled roughly $264 million from muni bond funds last week. Until we start to see more stability in muni market, we should continue to see a see-saw battle of inflows and outflows into and out of into muni funds. |

|

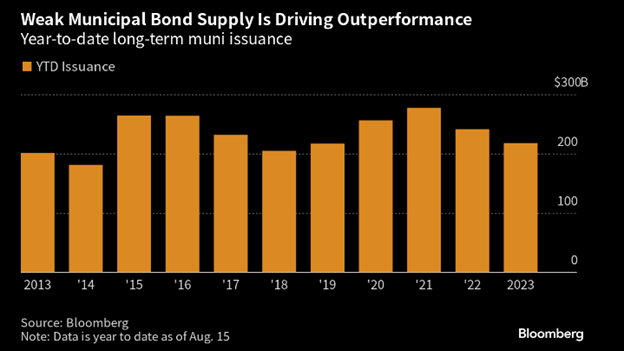

As we pass the mid-way point of the month, munis continue to struggle for the most part as many take their summer vacations. Munis have lost roughly 1.41% for the first half of the month, bringing the year-to-date to gains to 1.63% which is still higher than where we were last year which was a loss of 7.49%. Although we are down for the month of August, ratios continue to be rich as the front-end average ratio is at 65%. With supply down about 9% from last year, many municipalities are holding off on issuing as the Fed’s interest-rate hikes pushed yields higher. With the lack of new issues, munis continue to outperform Treasuries as investors and portfolio managers hold onto their bonds rather than sell, driving muni performance even higher. |

|

|

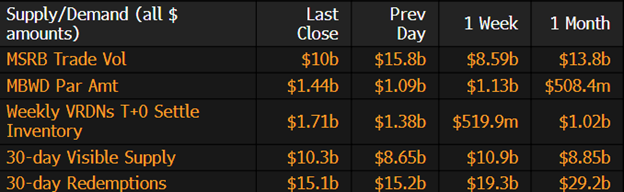

Municipal Supply: The negotiated calendar for this week will have an expected volume of just over $6.4 billion with two deals being over $1 billion. The two largest deals of the week will be the $1.18 billion State of Michigan State Trunk Line Fund, followed by the $1 billion New York City Transitional Finance Authority which AmeriVet will be in the Selling-Group. AmeriVet will be in two other deals this week which will be the $185 million Wisconsin Housing and Finance Development Authority which AmeriVet will be participating as a Co-Manager and the $19 million New Hampshire Housing and Finance Authority as a Selling-Group-Member. With the lack of supply, we should continue to see many of the issues be well oversubscribed. |

|