AmeriVet Weekly Muni Snapshot

|

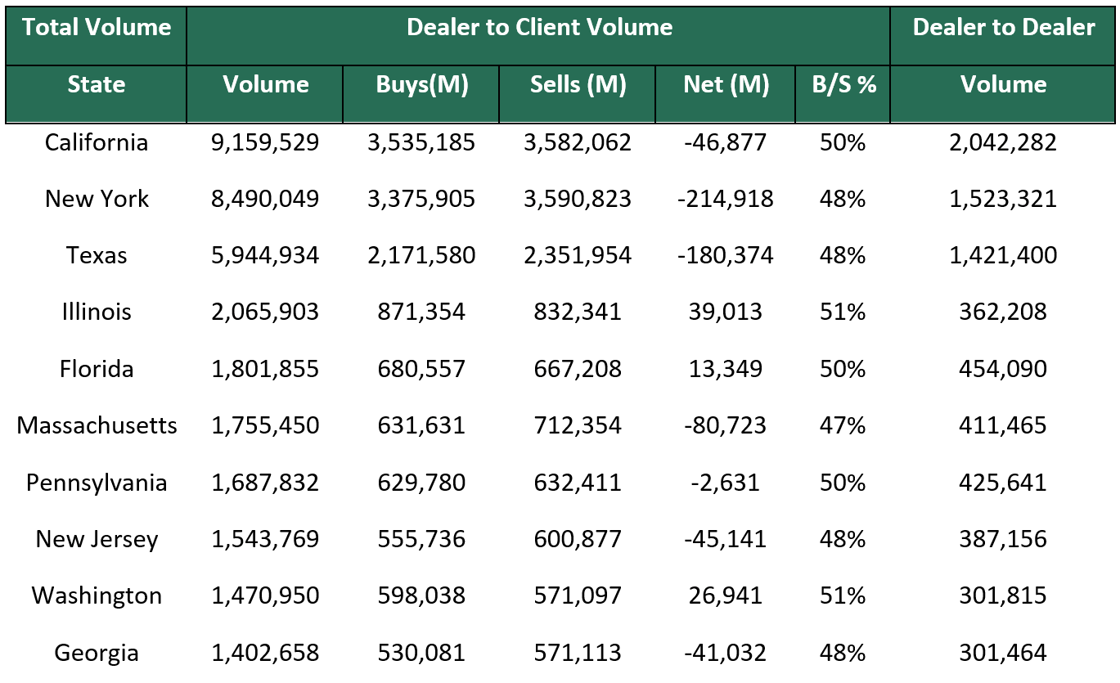

Municipal New Issuance: Last week’s negotiated calendar totaled to just over $8 billion as many issuers decided to issue prior to this weeks Fed rate decision. The most notable deals of the week were the $877 million New York Transportation Development Corporation issue for the LaGuardia Delta Airport Terminal project, followed by the $840 million Los Angeles Unified School District issuance. The City of San Francisco issued $794 million for their International Airport (SFO) and the New York State Power Authority issued $734 million. Municipal Secondary Trading: Secondary trading for the week totaled to just over $54.66 billion with 51% of all secondary trades being dealer sells. With yields continuing to rise this past week, we did see a record number of bids-wanted. According to Bloomberg, clients put up just over $10.63 billion up for the bid compared to the prior week’s total of $8.92 billion. |

|

|

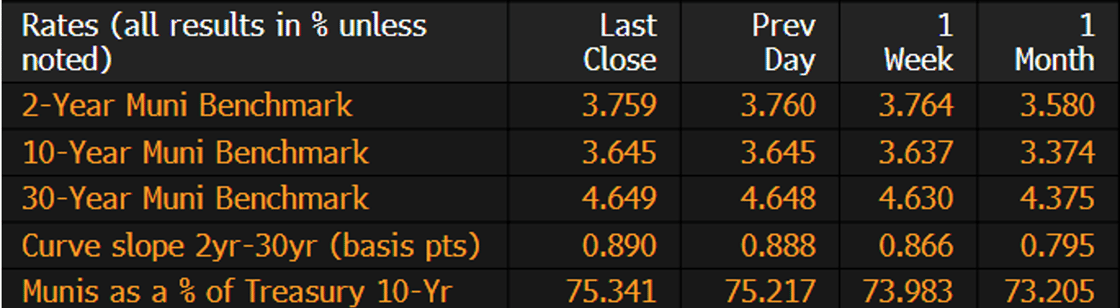

Municipal Spreads: Muni yields remained relatively unchanged for the week as 10-year notes rose by just by .8 basis points to close the week at 3.64%. With yields being unchanged for the week, we did see muni ratios rise as 10-year notes are now yielding 75.34% of US Treasuries compared to 73.98% a week ago. Just one month ago, those ratios were 73.20%. With the slight rise in yields, the muni curve did steepen slightly by 2.6 basis points to end the week at 89 basis points. |

|

|

According to LSEG Lipper Global investors, investors pulled approximately $935 million from municipal bonds funds this past week which follows the prior weeks outflow of $297 million and marks the eighth consecutive week of outflows. With yields continuing their upward trend, we will continue to see investors pull their investments from bond funds. |

|

With October coming to a close, we are currently down .91% for the month and 2.28% for the year, keeping us on track for the second straight year of declines due to the Fed’s interest-rate hikes and their intentions to keep rates higher in the longer term to tame inflation. Although we are poised for another down-year, yields have surged to their highest points in over a decade, reaching levels that we should expect to see investors re-enter into the muni market bringing demand back into the municipal markets. |

|

|

Municipal Supply: With the Fed rate decision this week, the negotiated calendar will have an expected volume of just over $1.9 billion. The largest deals this week are the $189 million Connecticut Housing Finance Authority issue followed by the $171 million City of Dallas Texas issue, and the $162 million Southern California Public Power Authority. |

|