AmeriVet Weekly Muni Snapshot

|

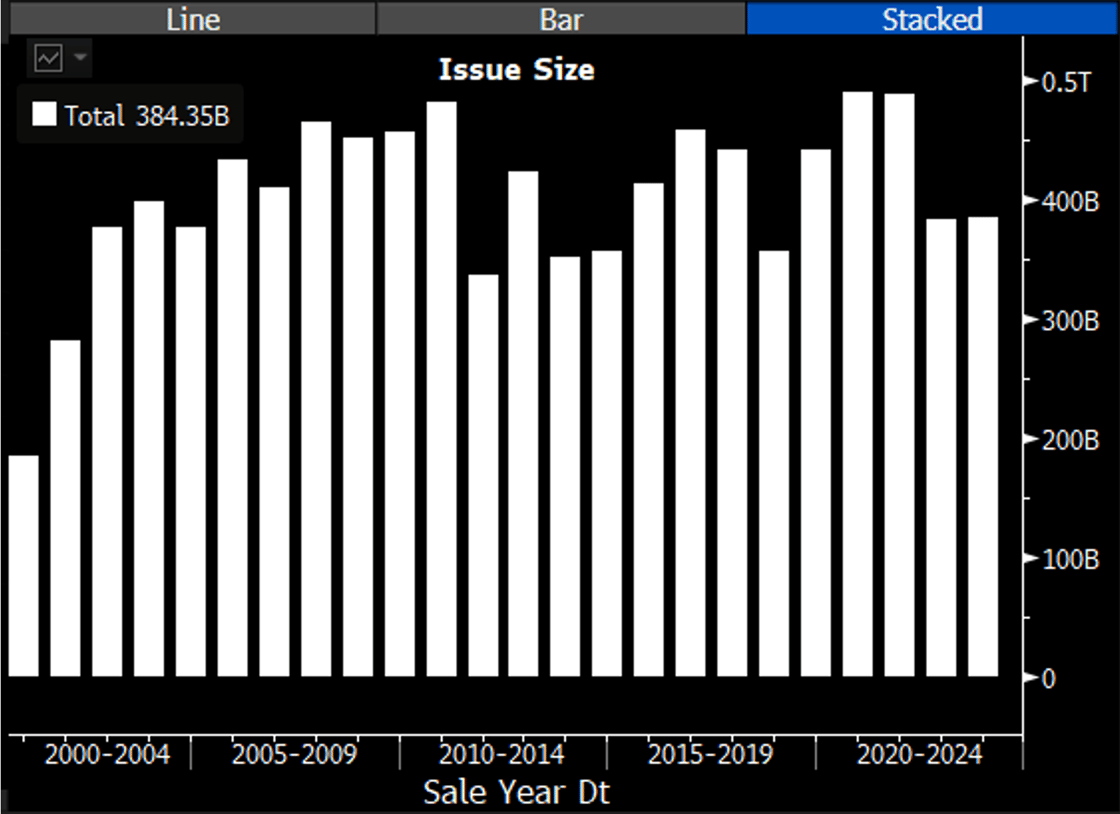

Municipal New Issuance: For the last week of the year, we did not have any new negotiated issuance as issuers were finished for the year. Issuers issued roughly $384.35 billion for 2024, which is a slight increase from 2022 when issuers issued about $382.91 billion. For 2024, it is expected that we should see an increase of issuance as it appears that the Fed will cut rates late in 2024. |

|

|

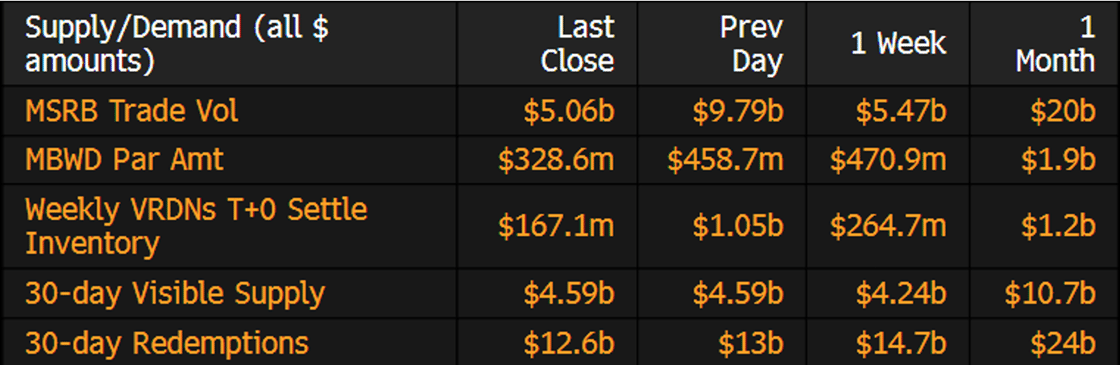

Municipal Secondary Trading: For the last week of the year, secondary trading totaled to just over $19.5 billion for the week with 59% of the trading being dealer’s sell. With trading volume being down, we did see client’s bids-wanted down as well. According to Bloomberg, clients put up just under $1.7 billion up for the bid. |

|

|

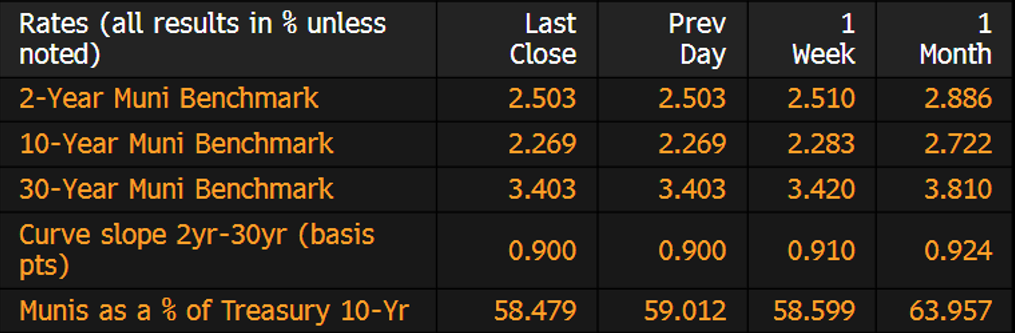

Municipal Spreads: For the last week of the year, munis were relatively quiet for the week with yields on 10-year notes falling by just 1.9 basis points to close out the year at 2.27%. At the start of the year, 10-year notes were at 2.62%. With the quiet week, munis did underperform Treasuries slightly as 10-year notes are now yielding 58.48% hitting the 52-week low. At the start of the year the ratio was at 70.54%. The muni curve flattened slightly this past week by 1.2 basis points to close the week at 90 basis points. On January 3rd, 2023, the curve was at 95 basis points. |

|

|

According to LSEF Lipper Global Fund Flows Data, outflows returned this past week as investors pulled about $464 million from municipal bond funds. This follows the prior week’s inflow into municipal bonds funds to the tune of $147 million. |

|

2023 was an interesting year as we started off strong with the first half of the year returning about 2.67%. The second half of the year was a roller coaster ride for munis as the third quarter saw rate volatility that pushed munis into negative territory for the year with September seeing muni yields climb an average of 50 basis points. In October, we started to see some stability in rates as Fed paused rate hikes over two consecutive meetings signaling that their rates hikes would be over for the time being. The final two months of the year we did see a record rally for the last two months of the year with November returning 6.35% and December returning 2.30%, bringing the year-to-date returns to 6.38%. 2024 should be the year of opportunity as muni yields are at their highest in over a decade, the Fed rate hike policy done, and an increase in supply, investors should take advantage of the higher rates before the Fed pivots. |

|

|

Municipal Supply: For the first week of 2024, the negotiated calendar with have an expected size of $173 million, with no deals being over $100 million. For the second week of January, we should expect to see issuance pick up. The expected 2024 supply for most firms will be in the range of $330 billion to $450 billion. |

|