AmeriVet Weekly Muni Snapshot

|

Municipal New Issuance: Last week, the negotiated calendar totaled to just under $3.7 billion for the week with the largest deals being the $654 million Kentucky State Public Energy Authority issue followed by the $382 million Prosper Independent School District issuance. The Illinois Housing Development Authority issued $349 million in Taxable bonds. |

|

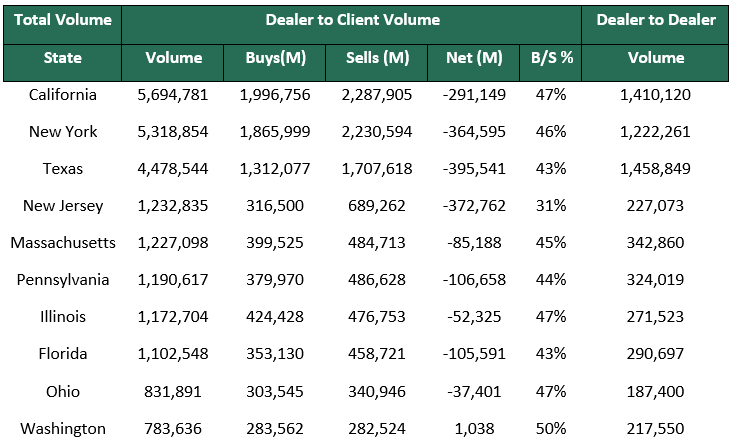

Municipal Secondary Trading: Secondary trading for the week totaled to about $35.85 billion for the week with 56% of trading being dealer sells. According to Bloomberg, clients put up roughly $4.67 billion up for the bid with Thursday having the largest volume of bids-wanted, totaling to approximately $1.14 billion. With supply continuing to be low, we should start to see secondary trading volume pick up as investors continue to put their money to work. |

|

|

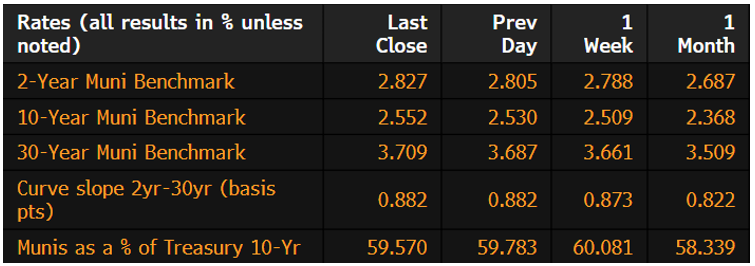

Municipal Spreads: Muni yields rose this past week with 10-year notes rising by 4.3 basis points to end the week at 2.55%. Although yields rose last week, munis were still able to outperform Treasuries with 10-year notes now yielding 59.57% of Treasuries, compared to the prior week when the ratio was at 60.08%. The muni curve did steepen by .9 basis points last week to 88 basis points. |

|

|

For the second week in a row, municipal bond funds saw investors pull their investments out their funds. Investors pulled about $142 million from municipal bond funds according to LSEG Lipper Global Fund Flows Data. The prior week we saw investors pull roughly $121 million for those funds. |

|

As we pass the midway point of February, muni returns continue to push us further into the red. So far this month, munis are down roughly .20% bringing year-to-date returns of –.71% with yields rising by an average of 18 basis points this month and since the beginning of this year, muni yields have risen by an average of 26 basis points. With the new economic data signaling a delay of the Fed starting rate cuts to further into the year, we should continue to see yields rise until we get near to the Fed’s target of a 2% “neutral” rate for inflation. |

|

|

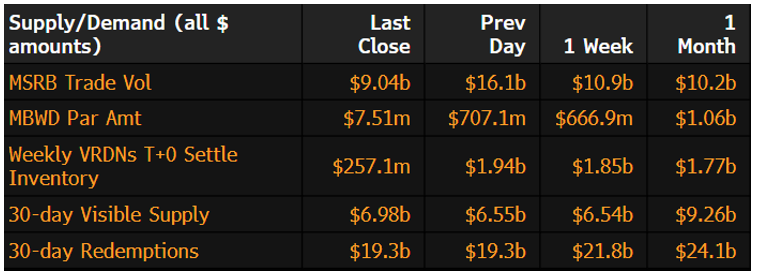

Municipal Supply: With just four days of trading this week due to the Presidents’ Day Holiday, the negotiated calendar will total to just over $4.4 billion. The most notable deals of the week will the New Jersey Educational Facilities Authority which plans on issuing $659 million for Princeton University. Maryland Transportation Authority plans on issuing $628 million in refunding bonds. The California Infrastructure and Economic Development Bank plans on issuing $281 million. Michigan State Housing Development Authority will issue roughly $248 million. We could continue to see supply fall as issuers continue to sit on the sidelines as the 30-day visible supply now sits at $4.9 billion. |

|