AmeriVet Weekly Muni Snapshot

|

Municipal New Issuance: With a shortened trading week due to the Presidents’ Day Holiday, the negotiated calendar had a total volume of $4.7 billion with the largest deal being the $658 million New Jersey Educational Facilities Authority for the Princeton University. The second largest deal last week was the $622 million Maryland Transportation Authority issuance. |

|

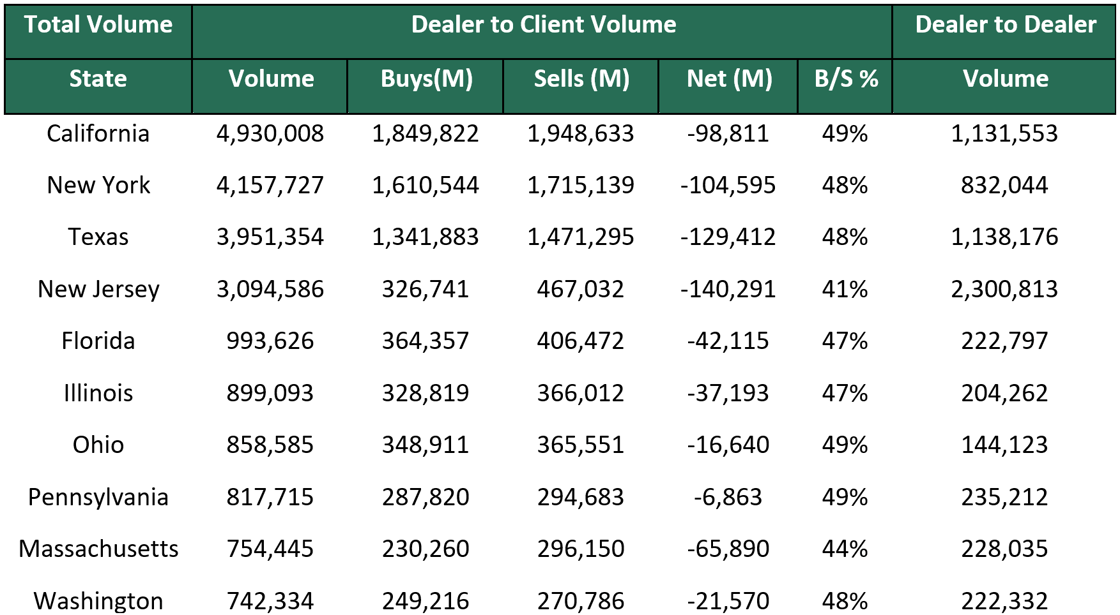

Municipal Secondary Trading: Secondary trading for the week totaled to about $29.98 billion, with 53% of all secondary trades being dealer sells. With a large calendar this week, we should expect that the main focus will be on the new issue calendar. According the Bloomberg, client’s bids-wanted totaled to just over $4.6 billion with the largest volume of bids-wanted being last Thursday with $1.4 billion. |

|

|

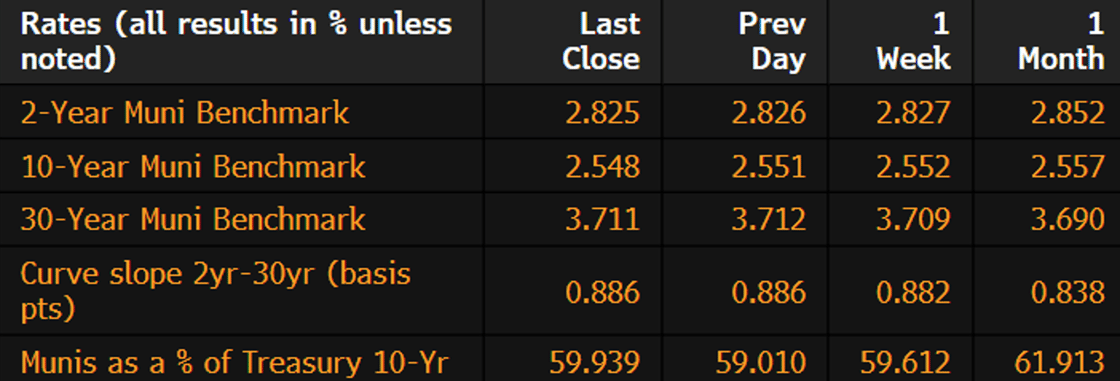

Municipal Spreads: Muni yields remained relatively unchanged, with 10-year notes rising by .4 basis points to 2.54%. With yields remaining unchanged for the week, we did see munis underperform Treasuries with 10-year notes yielding 59.93% of Treasuries compared to the prior week when the ratio was at 59.61%. We did see a slight steepening of the muni curve with the curve steepening by .4 basis points to end the week at 89 basis points. |

|

|

According the LSEG Lipper Global Fund Flows data, for the third week in a row muni bond funds saw outflows with investors pulling roughly $11.4 million. Just prior to last week, there was an outflow of $140.9 million. |

|

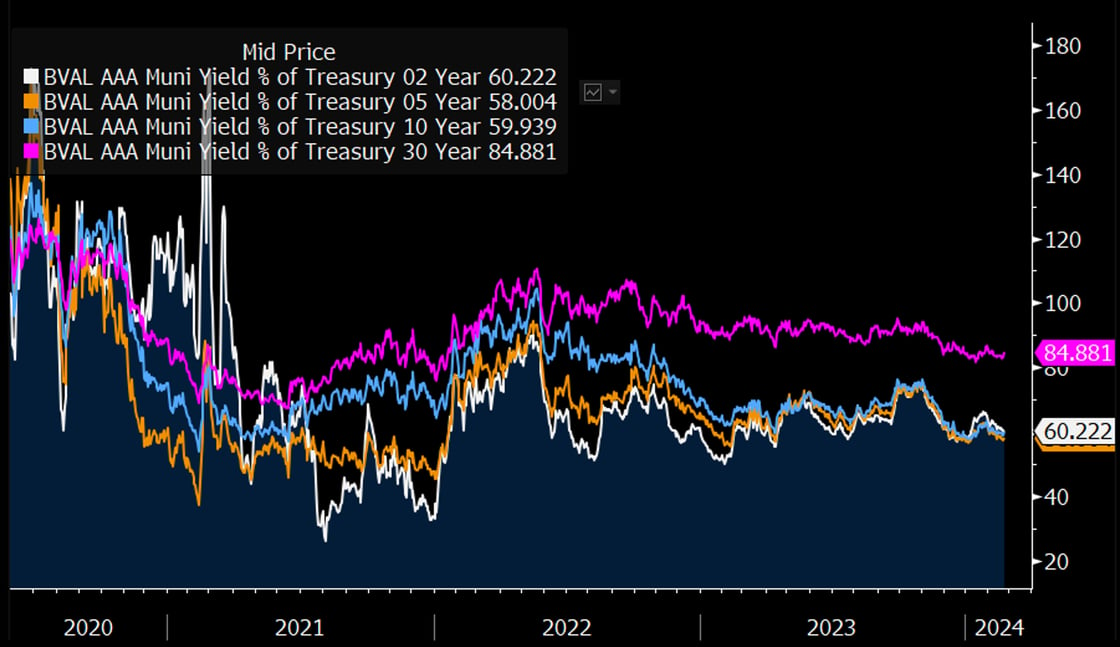

With munis yields continuing to trend higher this month, they are still faring better than Treasuries as we can see munis outperform Treasuries with the 5-year maturities showing the most sizeable out-performance since the start of the month. Since the start of the month, 5-year maturities have dropped by 5 percentage points, 2-year notes have fallen 4.88 percentage points, and 10-year notes have dropped by just 3.9 basis points. This is significant as this shows that yields continue to be attractive even as yields trend higher. |

|

|

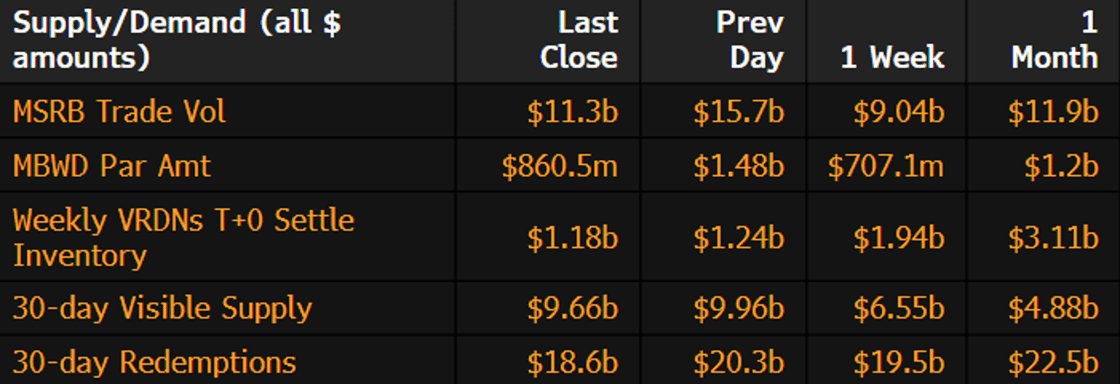

Municipal Supply: The negotiated calendar will have an expected volume of just over $5.3 billion with the largest deal being the $1.5 billion City of New York General Obligation Bonds issuance which AmeriVet will be participating in the Selling-Group. The next largest deal of the week will be the Hurst-Euless-Bedford Independent School District issue which will offer $600 million, followed by the $351 Texas Transportation Commission State Highway Fund. Although visible supply continues to be low, currently standing at $9.62 billion, it is still above the 2023 average of $8.9 billion. |

|