Treasury Inversion Is Not About the U.S., It Is About the Whole World

The U.S. yield curve is flirting with another broad-based inversion, reigniting Wall Street fears over the fate of the American economy.

A growing chorus of voices is being swayed by another notion: the signal might say more about the state of the world than the U.S. business cycle.

Treasuries now make up more than half of the world’s haven assets, double the share they accounted for during the global financial crisis, according to Eurizon SLJ Capital. That complicates matters when the spread between long- and short-term yields inverts: what used to be a reliable American recession indicator is instead an barometer of investors diving for cover worldwide.

It’s a narrative that makes a lot of sense as the threat from the coronavirus continues to grow, and it revives the frantic debate from last year about how much predictive power the yield curve actually has left.

“In a grab for safety and duration, everyone is going for U.S. Treasuries,” said Gregory Faranello, the head of U.S. rates at AmeriVet Securities in New York. “The yield curve inversion is a signal now of global growth issues, and not really reflecting what is going on in the U.S.”

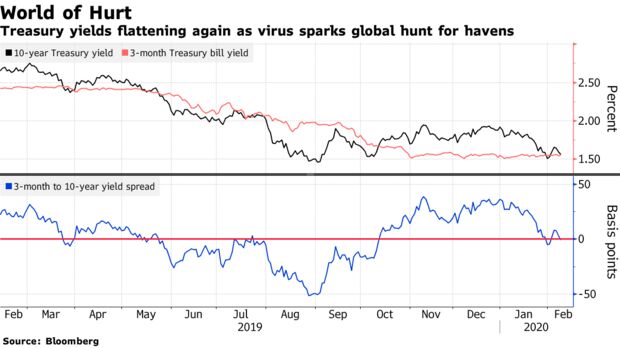

After a respite early last week, the curve is once again flattening, with the spread between yields on three-month and 10-year Treasuries inverting once more on Monday. This followed an earlier inversion starting Jan. 30 that was caused by growing angst about the coronavirus and an equity sell-off.

Pessimistic View

Bond yields typically rise alongside the maturity of debt because they provide compensation for the effects of inflation. If yields on a 10-year note are lower than those on a three-month bill, it suggests investors have a pessimistic view of growth and inflation a decade from now.

Global hunger for U.S. bonds helps explain American exceptionalism in growth, currency markets and stocks, according to Stephen Jen, chief executive officer at Eurizon SLJ.

He predicts that by 2022, U.S. government debt will account for two-thirds of the world’s pool of haven bonds thanks to large issuance and quantitative easing by other central banks. His calculations are based on the outstanding amount of government debt in the U.S., Japan, and the three largest European economies, subtracting the portion that is owned by central banks.

“The U.S. might, perversely, thrive because of troubles elsewhere,” Jen said. “When U.S. Treasury yields fall due to shocks outside of the U.S. that may or may not have an impact on the U.S. economy, it often provides added stimulus.”

It’s a view Federal Reserve officials are playing close attention to as global risks from the virus mount. In an interview with Bloomberg TV, Fed Vice Chairman Richard Clarida played down the inversion and said the negative spread is “really driven not so much by an outlook for the U.S. economy, but globally.”When there’s uncertainty money flows to America,” he said, “so current yield moves don’t reflect the U.S. outlook.”

Campbell Harvey is credited with drawing the link between the slope of the yield curve and economic growth. The professor at Duke University’s Fuqua School of Business says corporate America is much more attuned to the yield curve signal and will take preventative action.

“CFOs and CEOs are more aware and aren’t likely to take on the risk of just ignoring it,” Harvey said. “They are being a little more cautious now.”

Prior Inversions

The gap between the yield on three-month and 10-year Treasuries slipped to as low as about minus six basis points on Jan. 31. The spread — which has inverted before each of the past seven U.S. recessions — had initially fallen below zero in March 2019 as economic conditions deteriorated at the height of the U.S.-China trade war. The difference between two- and 10-year yields, which was negative as recently as September, remains above that mark at roughly 17 basis points.

On Wall Street, strategists at JPMorgan Chase & Co. still see plenty of reason to fret the slope of the curve. Their favorite indicator — and a part of the curve that remains inverted — is the gap between two-year forward and one-year forward rates, which can shed light on the bond market’s expectations of what the Fed will do.

In this case, it shows a “rising probability of a more protracted Fed rate cut cycle extending to 2021,” said Nikolaos Panigirtzoglou, a strategist at the investment bank.

For now, there aren’t many other alarm bells in an American economy with unemployment rates near 50-year lows and the longest stretch without a recession since World War II. Even so, economists forecast that GDP growth will slow to 1.8% compared with 2.3% in 2019, and it’s too early to determine whether the coronavirus outbreak in China will significantly affect the U.S. economy.

“We’re seeing overall risk appetite being driven on global growth,” said Edward Moya, a senior market analyst at Oanda Corp. in New York. “If we continue to see a risk-off scenario, you’re going to see Treasuries remain the key investment for all investors around the world.”

–-With assistance from David Westin and Vivien Lou Chen.