Weekly Muni Snapshot | June 21 , 2021

|

Municipal New Issuance: The negotiated calendar for last week totaled approximately $11.6 billion in overall volume. The largest deal of the week which AmeriVet was part of the syndicate was the $1.8 billion New York State Dormitory Authority taxable and tax-exempt Issues. Both series saw good demand which Allowed the underwriters to lower yields across all maturities. The Port of Seattle also priced a deal with a total size of $514 million, that issue saw solid demand as well. AmeriVet was part one other issue which was the $500 million New York City Housing Development Corporation which also saw it yield levels tighten as a result of robust investor demand.

Municipal Secondary Trading: Secondary trading for the week saw roughly $24 billion in trading which is just around the weekly average we have seen for 2021 but still well below the weekly historical average over the past few years. Secondary trading volumes continue to be very light as many investors are opting to hold onto their bonds then rather have to pay capital gains taxes when they sell as well as having to pay a high premium for bonds when they reinvest. According to Bloomberg Client bids-wanted total to roughly $3.1 billion, which is an increase from the prior week of $2.67 billion. |

|

|

Municipal Spread: Municipal bond yields for the week rose with the yields on the Bloomberg 10-year rising by 8.9 basis points to 0.969%, a significant reversal of what we saw in the prior week. With municipal yields rising and with the rally in Treasuries, municipal bonds underperformed when compared to Treasuries as debt maturing in 10-years now yields 67.24% of Treasuries. Ratios did touch its all-time lows earlier in the week, but we had a quick reversal due to the rally we had in Treasuries. The municipal bond curve did steepen by 1.2 basis points to 136 basis points as bond yields rose across the curve. |

|

|

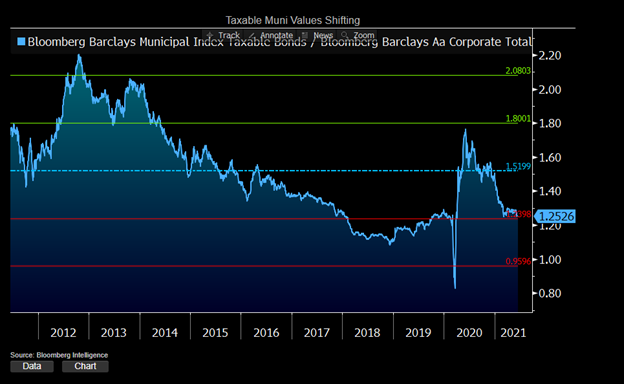

For 15th straight week investors added to municipal-bond mutual funds during the week ended Wednesday. According to Refinitiv Lipper US Fund Flows data investors added about $1.85 billion to those funds with about $1.52 billion, going into Long-Term municipal funds. This trend continues to show that investors to see value in the tax-exempt sector as they are looking for the tax-exempt income. Taxable municipal bonds vs corporate bonds are finally starting to go back to pre-pandemic levels signaling, that taxable munis are cheap relative to other forms of taxable investments. Currently, taxable municipal bonds are now yielding 125% vs corporate bonds which is significantly higher than what we saw in March 2020 which was 86%. On an index level Taxable municipal bonds are 138 basis points compared to a high of 180 basis points back in May 2020 with a 10-year average of 154 basis points while corporates have declined by about 300 basis points since Spring 2020. |

|

|

Municipal Supply: The negotiated calendar will pick up once again this week with a total of roughly $10.9 billion in supply which is one of the largest amounts of issuance, we have had this year. The largest deal of the week will the $1.8 billion City of Los Angeles California Tax and Revenue Anticipation Notes. The next largest deal for the week will be the State of Tennessee which will issue $657.7 million in taxable refunding bonds. The Michigan Strategic Fund Limited Obligation Revenue Fund plans to issue about $604 million in revenue bonds to fund various projects across the state. AmeriVet will be part of one issue this week which will be the New York State Housing Finance $209 million in Affordable Housing Revenue bonds. The volume of municipal debt sales seams to be increasing as request for new cusips climbed 5% in May which is the 4th straight monthly increase, with a 7.9% year-over-year. |

|

|