Weekly Muni Snapshot | November 1, 2021

|

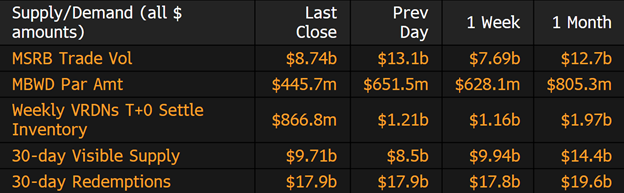

November 1, 2021 Municipal New Issuance: The negotiated calendar for the final week of October saw just over $6.6 billion issued with one issue being over $1 billion. Dallas & Fort Worth International issued $706 million in taxable bonds and $299 million in tax-exempt bonds in revenue bonds for a total of $1 billion. Los Angeles Unified School District issued $494 million in tax-exempt general obligation bonds. Municipal Secondary Trading: Secondary trading for the week totaled to just over $28.9 billion with 55% of tall secondary trades were clients buying. Trading continues to be on the light side as many continue to focus on the new issue calendar even as the new issue supply has dried up as well. According to Bloomberg clients put up $3.14 billion bonds up for the bid down from the prior week of $3.8 billion. |

|

|

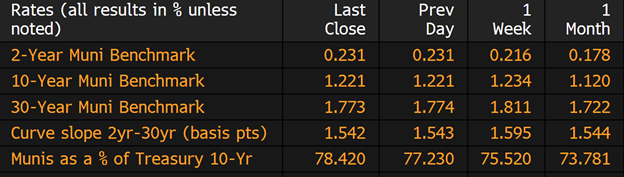

Municipal Spread: Municipal bonds remained relatively unchanged with the 10-year notes falling just by 1.3 basis points from 1.23% to 1.22% Although, yields fell, municipals did underperform Treasuries as state and local debt maturing in 10 year is now yielding 78.42% of Treasuries compared to 75.52% a week ago and 71.54% a month ago. With yields falling, we did see the municipal bond curve flatten by 5 basis points in the past week to 154 basis points. |

|

|

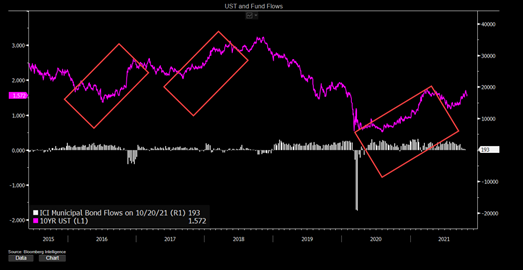

For the 34th straight week municipal-bond funds saw a weekly cash flow with investors adding $397 million to those funds, according to Refinitiv Lipper US Fund Flows data. This follows the previous week’s inflow of $177 million as many continue pour money into tax-exempt bonds. High yield funds for the week saw its smallest weekly inflow in which they gained just $3.2 million. Even though we have been seeing rates rise steadily over the past year this still has deterred investors. |

|

|

The tax-exempt received come bad news this week as the advanced refunding revival along with the taxable bond infrastructure plan that would have created a Build America Bond style debt program was left out from the Build Back Better legislation proposed by the Biden Administration. This came to a surprise as many expected that it would have been proposal as it would have helped many municipalities to finance the much-needed new infrastructure. If the tax-exempt provisions were left in the legislation, it was expected that we would have seen a flurry of issuance which the markets have been waiting for as issuance has dried up in the second half of the year. Even though municipal bonds were left out of the provision yields still have not reacted as many are still enjoying the low rates. Municipal Supply: The negotiated calendar for the first week of November will have an expected volume of about $3.75 billion with three of the issuers compiling to over half of the calendar. The largest issuer of the week will be the Texas Public Finance Authority which plans of selling 832.5 million in refunding bonds. AmeriVet will be a Co-manager on the second largest deal of the week, $553 million State Public Works Board of the State of California. Beth Israel Lahey Health will be issuing taxable bonds to the size of $500 million. |

|

|