Weekly Muni Snapshot | October 25, 2021

|

October 25, 2021

Municipal New Issuance: Last weeks negotiated calendar totaled to just over $10 billion with only one issue being over $500 million. The largest deal of the week which also saw the most demand was the $869 million Central Puget Sound Transit Authority revenue bonds. Hudson Yards infrastructure corporation issued $451 million in green revenue bonds which saw large demand as many investors continue to focus on the larger sized issues as supply has dwindled. AmeriVet was in two deals this week as a co-manager, which was the $225 million California Earthquake Authority notes issue as well as the $148 million Massachusetts Housing Finance Agency.

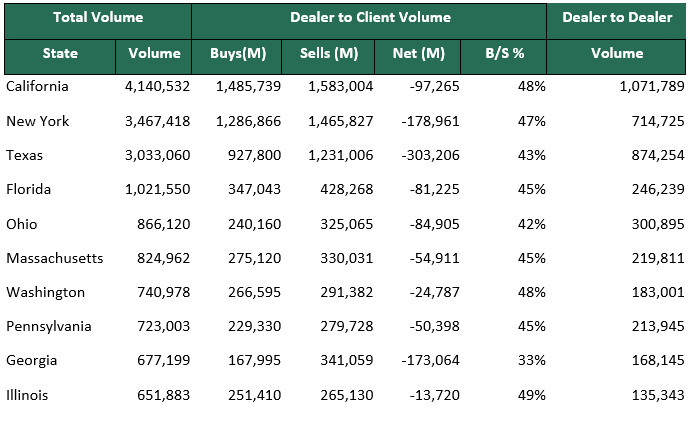

Municipal Secondary Trading: Secondary trading for the week totaled to just over $26 billion as trading continues to be far below the weekly average we are used to seeing in the past few years where we usually see over $35 billion in weekly volume. Even though secondary trading has been down, clients still are putting up their bonds up for the bid as clients placed over $3.8 billion bonds on the bids-wanted systems. |

|

|

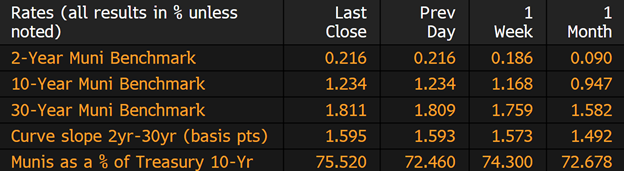

Municipal Spread: Municipal bonds continue their slide for the second half of the year with the Bloomberg 10-year notes rising by 6.6 basis points to 1.23% which is the highest we have seen since March 2020. This steep increase in yields was due to yields catching up to Treasuries after the Federal Reserve is expected to increase interest rates twice by the end of the year. This also drove investors to put over $860 million of bonds out for the bid on Thursday Oct 21st which was the most since May 13. With municipal bond yields rising last week they underperformed Treasuries as the 10-year ratio is now yielding 75.52% compared to 74.30% from the previous week. The municipal bond curve continued to follow everyone else with the curve steepening by 2.2 basis points in the past week to 159 basis points. |

|

|

According to Refinitiv Lipper US Fund Flows data investors added about $177 million into municipal-bond mutual funds which marks to 33rd straight week of inflows which follows the previous weeks $461 million of inflows. We did see some outflows in a few funds during the week with long-term funds losing about $44 million and high-yield funds losing about $58 million, with intermediate- maturity funds adding about $147 million.

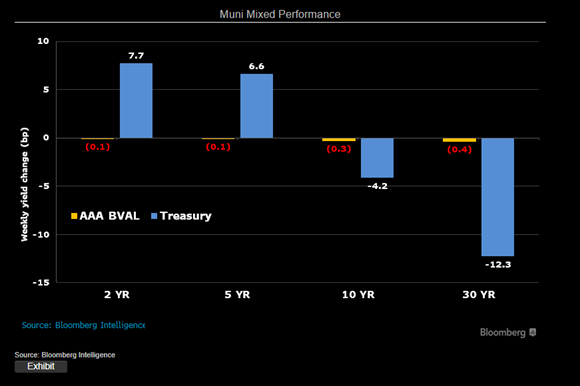

Depending upon which part of the curve you are looking at municipal bonds either outperformed or underperformed when compared to Treasuries. While Treasuries have climbed 7.7 basis points in the short end the long end has dipped over 12 basis points in the long end while AAA tax-exempt bonds have remained unchanged. |

|

|

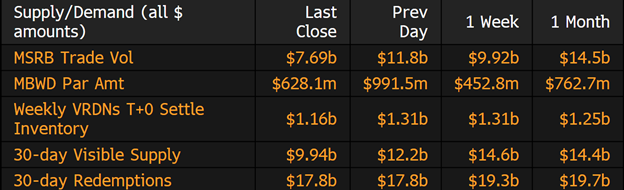

Municipal Supply: The negotiated calendar for the final week of October will continue to be very limited with about $6.4 billion in expected volume with only one deal being over $1. billion. This week the City of Dallas Forth Worth will be issuing $705 million in taxable refunding bonds and $300 million in tax-exempt bonds for the Dallas Fort Worth International Airport. Lost Angeles Unified School District of California has scheduled $556 million for their clean energy project. Sales on new debt has tumbled considerably this year with new debt issuance down 24% since September from a year earlier which has led to many just to focus on larger issuers. |

|

|