Weekly Muni Snapshot | September 27, 2021

|

September 27th, 2021

Municipal New Issuance: Negotiated issuance for the week totaled to about $7.2 billion for the week down from the prior week of $10.4 billion. The largest deal of the week was the Los Angeles Department of which totaled to about $879 million with AMT bonds as well as taxable bonds. The next largest deal of the week which AmeriVet was part of the syndicate was the $868 million Triborough Bridge and Tunnel Authority Revenue bonds. AmeriVet was also part of one other deal of the week which was the $147 million New York State Housing Authority.

Municipal Secondary Trading: Secondary trading picked up for the totaled to just around $25 billion for the week as many saw yields increase for the week and decided to take advantage of cheaper bonds especially since yields have been relatively unchanged for about a month. As with secondary trading, we did see clients put up more bonds up for the bid this week with customers putting up approximately $2.8 billion up for the bid compared to the previous week of $2.4 billion. |

|

|

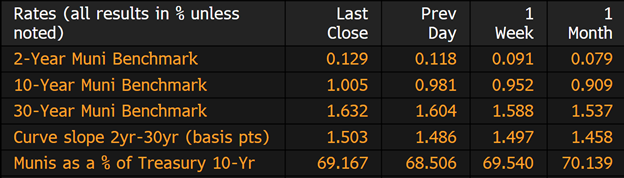

Municipal Spread: After multiple weeks of unchanged yields, yields on the 10-year notes rose by 4.8 basis points from 0.952% to 1.00%. Even as municipal bond yields rose this week, they did outpace Treasuries as the 10-year ratio is now yielding 69.16% of Treasuries compared to 69.54% a week ago. With the rise in rates, we did see the municipal bond curve flatten slightly by 0.6 basis points to 150 basis points as the short-term bonds rose by 2.7 basis points and long-term bonds by 2.6 basis points. |

|

|

For the 29th straight week investors added to municipal-bond mutual funds during the week ended on Wednesday by adding $1.55 billion to those funds according to Refinitiv Lipper US Fund Flows data. This follows lasts weeks inflow of $1.26 billion and the trend that we have seen all year as many investors are flocking to tax-exempt bonds as they continue to seek yield and the potential of any tax increases. High-yield funds continue to interest as those funds picked up $408 million in new investments.

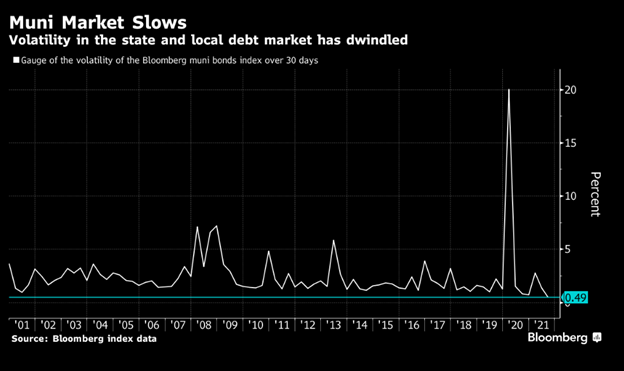

The municipal bond market has been eerily quiet for the past few months which been a big blow to many traders as many continue to wait for some market volatility. September’s volatility for has been exceptionally slow as volatility has tumbled to just shy of the record low that was set back in January. With 29 straight weeks of inflows, the potential of new proposals in Congress which can unleash new debt if enacted and the increase of bond sales in the last few months many expected to see new buying opportunities but that still has not materialized as yields continue to be stagnant. |

|

|

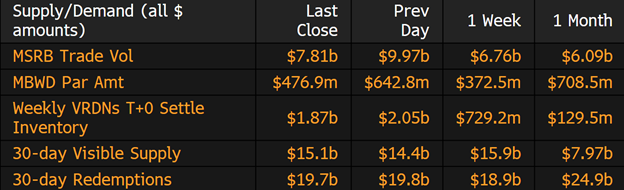

Municipal Supply: The negotiated calendar will have an expected volume of $9.3 billion which is up from the prior week of $7.9 billion as supply finally picks up. This week we will have 2 issues that will be over $1.5 billion. The State of Hawaii will be issuing $1.9 taxable bonds that will consist of taxable general obligation bonds as well as taxable general obligation refunding bonds. The Golden State Tobacco Securitization Corporation will be issuing $1.84 billion in federally taxable refunding bonds. California State Housing Finance Agency will be issuing $995 million Social Certificates bonds. |

|

|